Rishi Laser is a precision fabricator. It has 13 manufacturing unit across 5 states. They have sheet metal processing capacity of 45000MT. They have diversified clients.

A glance of Balance Sheet suggests that their sale has increase from 55 crore in FY2007 to 155 crore in FY2011. Operating profit is on lower side and the company dipped into red in FY2009. In 2009 & 2010 the company skipped dividend, however a dividend of 12.5% was declared in FY2011.The company went into expansion mode in 2007 & 2008 when loans were raised. It resulted in higher interest payment and higher depreciation, leading to erosion of net profit. However, on operating level the company has been able to maintain its revenue and operating profit in down years, 2009 & 2010.

The company has a very strong cash flow. cash flow from operating activities has been strong even in down years of 2009 & 2010). In fact in these years the company has been able to repay a large chunk of its long term loans. Long term debt has been reduced from 75 crore in 2009 to 43 crore in 2011.

The company is a well managed company, having expertise in precision fabrication. All the infrastructure at the place, and company is generating enough cost to repay its debts in next 2 years. Further, the revenue of the company is increasing at a decent pace. With investment cycle picking up in India, and may be falling commodity prices, the company is in a sweet spot to benefit with India Infrastructure growth story. Further, falling interest payment will directly improve the net profit in the years to come.

At current market price, the company has a market cap of 30 crores. With revenue of more than 155 crores last year, based on price sales ratio the company is undervalued. Last year, eps was more than 6 rupees, which gives a pe ratio of around 6. Further, the company has a operating cash flow of arond 15 crores- looks very decent for a market cap of 30 crores. On these criteria the stocks appears to be undervalued.

The ace investor Rakesh Jhunjhunwala has also taken stake in the company- an icing on the cake.

looking cheap at 2 times free cash flow may do well in long run.

FY2011.The 2010.

hi!rajesh,

i agree this ia a good company and i am betting heavily on it,but just wanted to inform that mr.rakesh jhunjhunwalal has exited rishi long ago ,confirmed by the mgmt at agm.

It would have been better had the promoters held more shares and there would have been insider buying in the shares. But, Alas! is it impossible to find a company meeting all the favourable criteria and still be cheap… where everything is perfectly hunky dory, price quotation ensures that one will not get anything more than FD rates in long term. Investing in hidden gems is all about decision making in uncertain environment.

As the company had bad 2009 & 2010, RONW is certainly pathetic. But it is improving, and likely to improve with investment cycle as and when it improves. All said and done, it is in engineering sector, depended upon capital investment cycle… the cycle was bad in last few years, the company didnt do well; if the cycle turns up, it may do well. Further, RONW may not be a very good indicator for companies operating in cyclical industry… cyclicals ought to be purchased when RONW is pathetic and sold when RONW starts shining. Peter Lynch said the same using PE ratio… he said that cyclicals should be brought when PE is very high and sold when PE falls, i.e. earning rise a lot.

It was certainly very leveraged when downcycle started in 2008. Debt equity ratio was touching 2, Interest coverage ratio less than 1.5. In 2011, situation have changed with repayment of loans. Debt equity is less than 1 and operating profit is covering the interest comfortably.

When we look at profit & loss account, raw materials cost is around 60% of the total sale. For a fabricator, it is a great margin showing competitive advantage. For this reason only, the company withstood the last downturn without much difficulty. I am presuming that investment cycle will start in the months to come, and in that scenario, the stock is in a sweet spot.

here is the ROC for the last 5 years - never gone over 10 % -

8.65 6.23 4.73 9.67 7.99

if your definition of ‘comfortable’ interest coverage is 2 - then I guess you have a different standard. mine is 5.

what are the inputs that allow you to predict a new investment cycle will start in 2 months - especially with IIP numbers falling consistently and growth moderating metrics everywhere.

how exactly did you come to the conclusion that it is available at 2 times FCF. mind you - EBITDA is not equal to FCF. But, anyways, I will give the benefit of doubt and wait for your explanation.

Why do I think that investment cycle will take a upturn?

Well, predicting economic cycle is as good as impossible. RBI will all its reserach departments is not able to predict the inflation or interest rates. By the time economists comes to the conclusion that recession is coming, generally we are already 3 quarters in recession and recession is likely to end. I have no clue that investment cycle will take a upturn, in fact there is no economic data which is pointing towards investment cycle upturn. But I am sure it will happen, and happen soon for these reasons,

1). A GDP growth rate of 7-8% or even 4-5% cannot be maintained without adequate investment. Thus we have to presume that either the GDP growth rate shall fall below 4% or investment cycle will upturn. If former is true, we should get out of market. I believe second is true.

2). Indian corporate are flushed with funds. Recent economic times article suggests that they have more than twice cash available than 2008. Further, we have a saving rate of around 35%. Where will these funds go? If investment cycle does not start, interest rate will fall to zero, which does not look possible. Thus investment cycle has to take a upturn.

3). There is sufficient demand in the economy. There is sufficient saving. There is no reason for not investing, which is natural.

Thus I am of the view that investment cycle should take a upturn. In fact at this point f time I am very fearful of defensive sectors stock… Nestle, ITC, Hawkins… their valuation suggests that they can be biggest under-performers in the coming years. So, I am forced to look into stocks based on investment cycle… even if it is unpredictable. Performance of Rishi Laser in down-cycle gives some confidence.

Whenever I get interested in any stock, I buy a few shares immediately… that way I start getting all the communications/report etc. from the company. That way I am invested in any stock I talk about.

Thanking you Pradeep for raising valid pitfalls of the company, which needs to be considered before any serious investment in the stocks can be made.

The stock has been languishing for a long time. In FY 2014 it reported a loss, nevertheless cash flow from the operating activity has remained positive. In the first two quarters also it has reported losses. The fortune of the company is inked to revival in investment activity particularly in power sector.

Recently management has decided to subscribe to 18L warrants, almost 20% of the equity of the company. It will raise management holding in the stock to around 35% level. Further it will also bring some cash to the company.

The best part of the company is its valuation. Share prices has started showing some uptick, and it closed today at around 17.50. At this CMP, the company is valued around 16 crores. Book value of the company is Rs. 43. It is available at around 0.15 times sales. Based on these parameters it may look deep value.

However, performance of the company, like most of others in similar business has been dismal in last few years. Management buying shares of the company is a positive. News are tricking about recent orders in power sector. If investment sentiment improves, the stock may give a decent return.

Nothing specific per say other than the fact that increasing revenue has been matched by increasing costs i.e. benefits of operating leverage were not visible in the last 2 quarter results. Do you have any views on that?

As a matter of fact the company is in a low margin business. Still the margin they get is enough- material cost is less than 60% of the sales. Thus, if capacity utilization goes up, bottom line can improve dramatically. It didnt happen in last many years, and hence the investment didnt perform.

Though the company is not showing any profit, enough cash is being generated to serve the debt and repay the debt meaningfully. Have a look from the 2019 Annual report- where debt has reduced from around 19 crores to 10 crores.

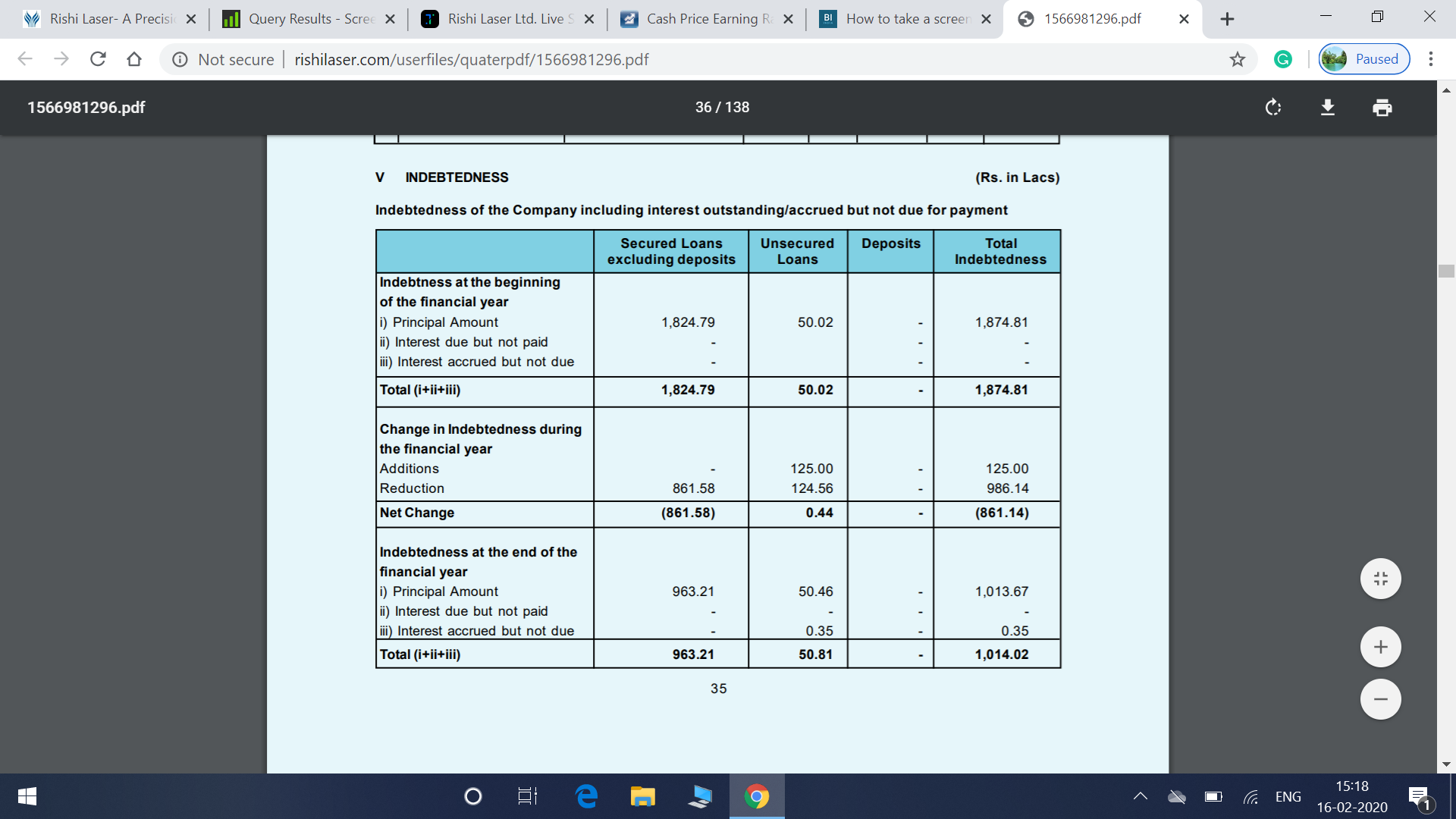

The debt has gone down substantially, and at the end of FY 2019, it was less than 1o crores. The company can be debt free by the end of 2020. We can see that around 2011-12, the debt was around 60 crores. Market cap at present is less than the free cash flow of the company. If the company can generate so much free cash flow in such difficult times, it can do wonders in good times.

Still, the stock is not performing for many reasons. The first reason being that infrastructure/capital goods sector is not doing well. Secondly, promoters have less shareholding- around 16%. If the infrastructure/capital goods/power- anything starts doing well; this low promoter holding will turn into a boon.

There are not many activist investors in India, otherwise such low promoter holding could have acted as invitation to activist investors.