After a very long time, the company declared a profit in Q4-2020-21. At a topline of 28 crores, it has shown a net profit of 2.1 crores. Looks like the capital goods cycle is turning positive.

Rishi Laser 2020-21.pdf (2.8 MB)

1 Like

Our country is going to have a lot of infrastructure spending going ahead. This is also evident from exploding orderbooks of many infra companies. Rishi is also a beneficiary.

Valuation wise it’s at mcap/sales of 0.1 at historical low not after share price being stagnant and sales increasing. Can it go upto mcap/sales of 0.4 from here?

Lot of operating leverage is available if sales increase profit can increase much faster

Can the sales increase from here given the tail winds present?

2 Likes

This company is turning around very well. Do anyone have idea regarding their current orderbook?

Thank you

Company has proposed for Concall…

Seems to be a turnaround story…

Any body attended the concal

Concal audio link

Very insightful detailed and high quality Concal from management.

Their major customer is CATERPILLAR and client name includes ALSTOM

Disclosure: Invested recently after listening to the Concal and is around 1% of my portfolio with long term view.

Q4 FY24 Con Call Notes - Organized Summary

Customer Update:

- Two customers in USA and one in Australia with ongoing commercial orders.

- Significant business growth expected after Q3.

Raw Material:

- Increased steel capacity expected in the next six months, potentially stabilizing prices.

Capital Expenditure (Capex) & New Business:

- New 70,000 sq ft facility 30 km from existing plants (₹10 cr investment).

- ₹2-5 cr allocated for routine upgrades.

- Full plant utilization expected in 2-3 years.

- Entering round & square steel processing (tubes).

- First machines for this new business arriving by Q2, generating revenue from Q3 onwards.

Products:

- Round & square steel processing will target:

- Equipment manufacturers

- Furniture industry

- Hospital industry (stainless steel tubes)

- Large cutting facility at the new plant to supply parts to Chennai and Bangalore factories (currently at full capacity).

Business Segment Growth:

- Top line growth anticipated in H2 driven by export expansion.

Exports:

- Initial commercial exports commenced with Emerson Electric (USA).

- First commercial order received from an Australian company (glass processing equipment).

- Caterpillar (domestic supplier):

- Parts exported to two US plants.

- Aftermarket component orders received.

- France: Parts exported last year.

Manpower & Efficiency:

- Maintaining current headcount while increasing sales by 50-60% through robot installation in the Bangalore plant.

Growth Potential:

- Optimistic outlook for H2 growth in the off-road construction equipment sector (large dumper trucks for mining).

- Conservative FY25 growth guidance: 15%.

- Potential for larger construction equipment customers (Caterpillar) to reach ₹120-150 cr revenue within 3-4 years.

- Combined revenue potential of new and existing facilities: ₹300 cr (conservative estimate).

Margins:

- Margins depend on skilled labor costs.

- Training facility opening in Gujarat to address this.

- Double-digit EBITDA margin possible with higher growth.

Plant Utilization:

- Bangalore & Chennai: Full utilization.

- Gujarat & Pune: Underutilized (exact utilization level needed).

Competitors:

- Apex Auto

- Surin Auto

- Model infrastructure

3 Likes

Thanks @venkatesan - This was helpful.

Will start tracking the same.

@rk1771 - Have you ever interacted with the management or visited their plant? You seem to be tracking this for 13 years now. Can we get further information from contacting them?

1 Like

Impressed by their conference call. Unlike most, Mr. Harshad presented a real picture of the company highlighting the difficulties as well rather than just presenting a rosy picture. Valuation wise, given an entry in the pipes business, there can be P/E expansion.

1 Like

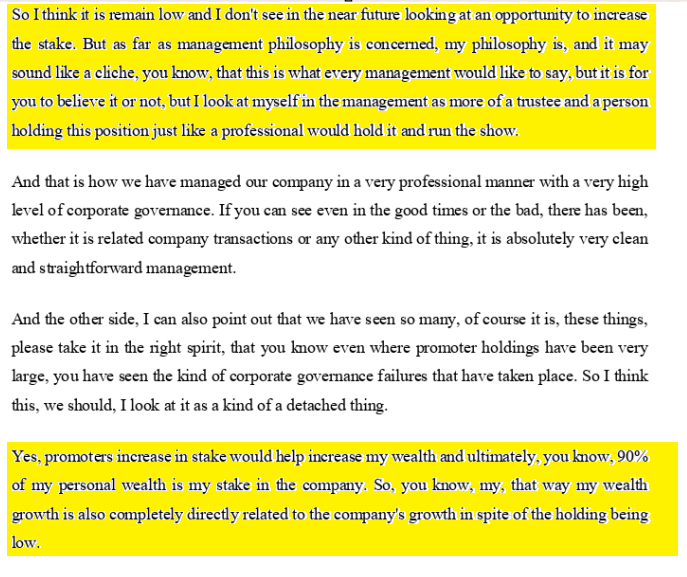

Steel fabrication company with promoter holding of only 16% ![]() Fails major first level filter for investment in any company IMHO…

Fails major first level filter for investment in any company IMHO…

Please go through the latest concall , promoter has answered regarding low promoter holding

Its an important filter but just go through the conference calls to get the whole idea about the company history, current situation and it’s future. A company with 80 Cr. market cap( at the time of first conf. call) conducted two hour call and admitting the mistakes during last cycle, being conservative and cautious this time, current opportunity and highlighting risks, give some solace. This kind of microcap investing always come with uncertainty and some or other item of the checklist is always missing, its up to the investor to take the call whatever he/she comfortable with. Regarding low stake, another way to look at, if a promotor has 15% stake but that is 90% of his networth(That’s what the promotor replied) that implies complete skin in the game and total focus in the company. This situation is better than a promoter having 50% stake but that could be a very tiny fraction of his overall networth and simultaneously managing 10 other companies also.

Yes, the stock trajectory could be volatile due to very low promoter stake and it does not give confidence to investor community and valuation could remain subdued but if story unfolds and shows in the earnings then both rerating and profit growth could give a decent returns.

Conf. call :

4 Likes

Does anyone know or can anyone share who owns the rest of the business?