In J.R.R. Tolkien’s epic book ‘Lord of the Rings’ there were three Rings for the Elven-kings under the sky, seven for the Dwarf-lords in their halls of stone, nine for the Mortal Men doomed to die, one for the Dark Lord on his dark throne but, ultimately, there was ONE RING TO RULE THEM ALL

Similarly in investing, there is ROE to measure return to shareholders, ROIC and ROCE to measure return to all capital holders, ROA to measure return on assets, Fixed Asset Turnover to measure fixed assets efficiency, Working Capital Turnover/Days to measure working capital efficiency, Gross/EBITDA/Operating margins to measure margin, etc but is there ONE RATIO TO MEASURE IT ALL?

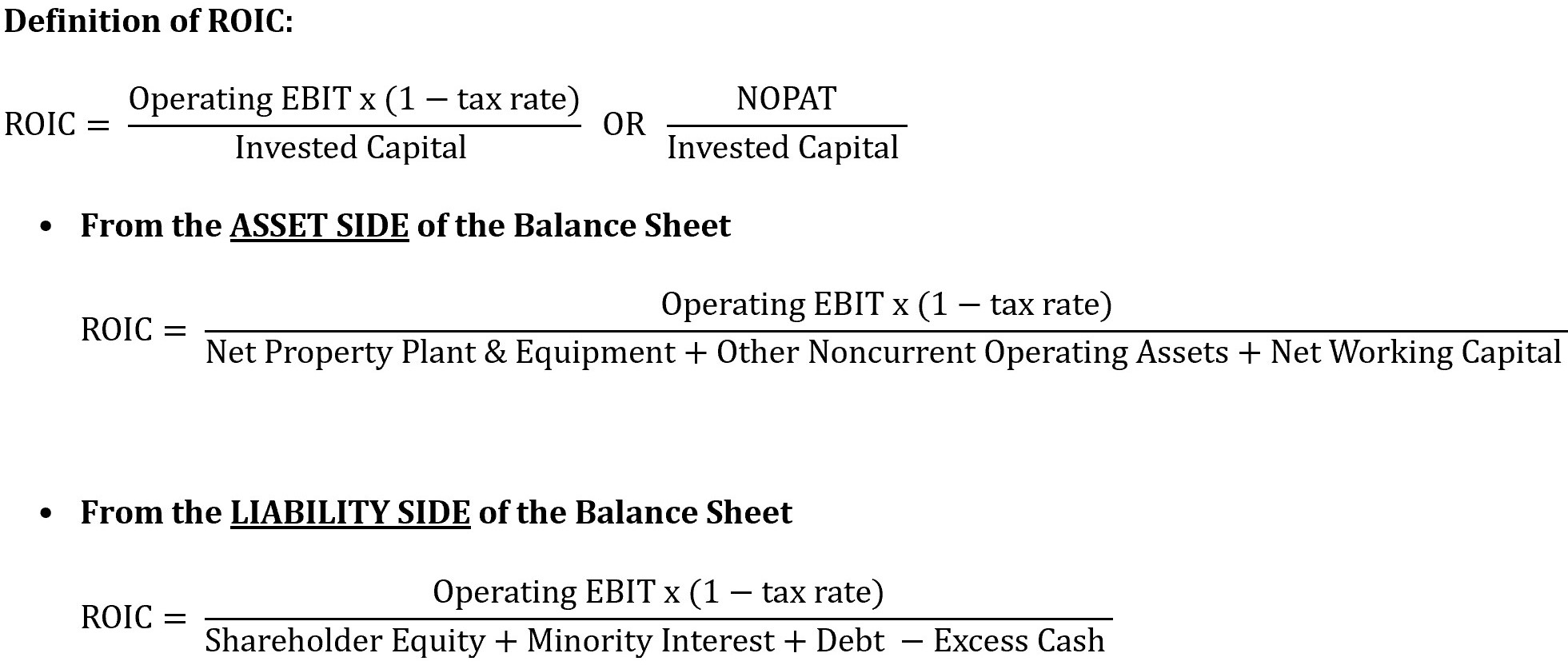

It is my belief that for NON-FINANCIAL COMPANIES Return On Invested Capital (ROIC) (defined as After Tax Operating Income/Invested Capital) is the best measure of return that be used to effectively analyse a wide range of operational parameters by breaking it down into its components.

I have also made an excel file that calculates the impact of ROIC of a company using your own estimate of Margins, Fixed Asset Turnover, Working Capital Days, etc. Click ROIC Predictor.xlsx (175.5 KB) to download. A more detailed version of this write-up is on my blogpost here

Why is ROIC better than measures of Return

There are other measures of Return such as Return on Equity (ROE), Return on Assets (ROA), ROCE (Return on Capital Employed) but all of them either do not measure operational performance properly or mix operational performance with capital structure/capital allocation. To understand the problems with each of this ratios you can read the write-up on the blogpost linked earlier.

ROIC is meant to measure SOLELY the operating performance of a company and thus it does not mix the impact of capital structure and/or capital allocation in its calculation. Then we can (and ought to!) independently examine the effects of capital structure and/or capital allocation issues seperately

How is ROIC calculated

Using the equivalence of the Balance Sheet, ROIC can be calculated both from the Asset Side and the Liability Side

As seen above, only the denominator is different from both the above formulas.

Why should we calculate ROIC from both sides of the balance sheet?

When calculating ROIC from the Asset Side we have to carefully consider what items of the balance sheet classify as operating assets and what do not. This is where calculating ROIC from both sides of the balance sheet helps us. In an ideal situation (for a company with no non-operational assets), both calculations should yield same results and hence calculating the ratio from both sides helps us understand if there is any operating item that we may be missing from our ROIC calculation from the asset side. Alternatively, the difference helps us to understand if the Company has allotted capital to non-operational assets which causes a lower ROIC on liability side.

Typically, ROIC calculated from the Asset Side is HIGHER than that from the Liability Side because the asset side does NOT consider Investments, Non-Operational Assets such as Marketable Securities, Long Term Loans & Advances, etc as part of invested capital. However, there could be times when the return from the Liability Side is higher. This could be because there could be Long Term liability such as Deferred Taxes, Pensions Obligations, or others that amount to a significant number

Measurement Issues and Fixes

Let’s assume that we have made correctly identified the operational items in the invested capital. However, even after that it is extremely important to know that simply plugging the numbers stated in the Annual Report will not give a correct estimate of ROIC (or for that matter any other measure of Return such as ROE, ROA, ROCE). Certain operational items will not even be reflected in the Balance Sheet. In fact, both the numerator and denominator need to be adjusted to get a true picture of the Return. I have given a link to articles detailing the adjustments that have to be made

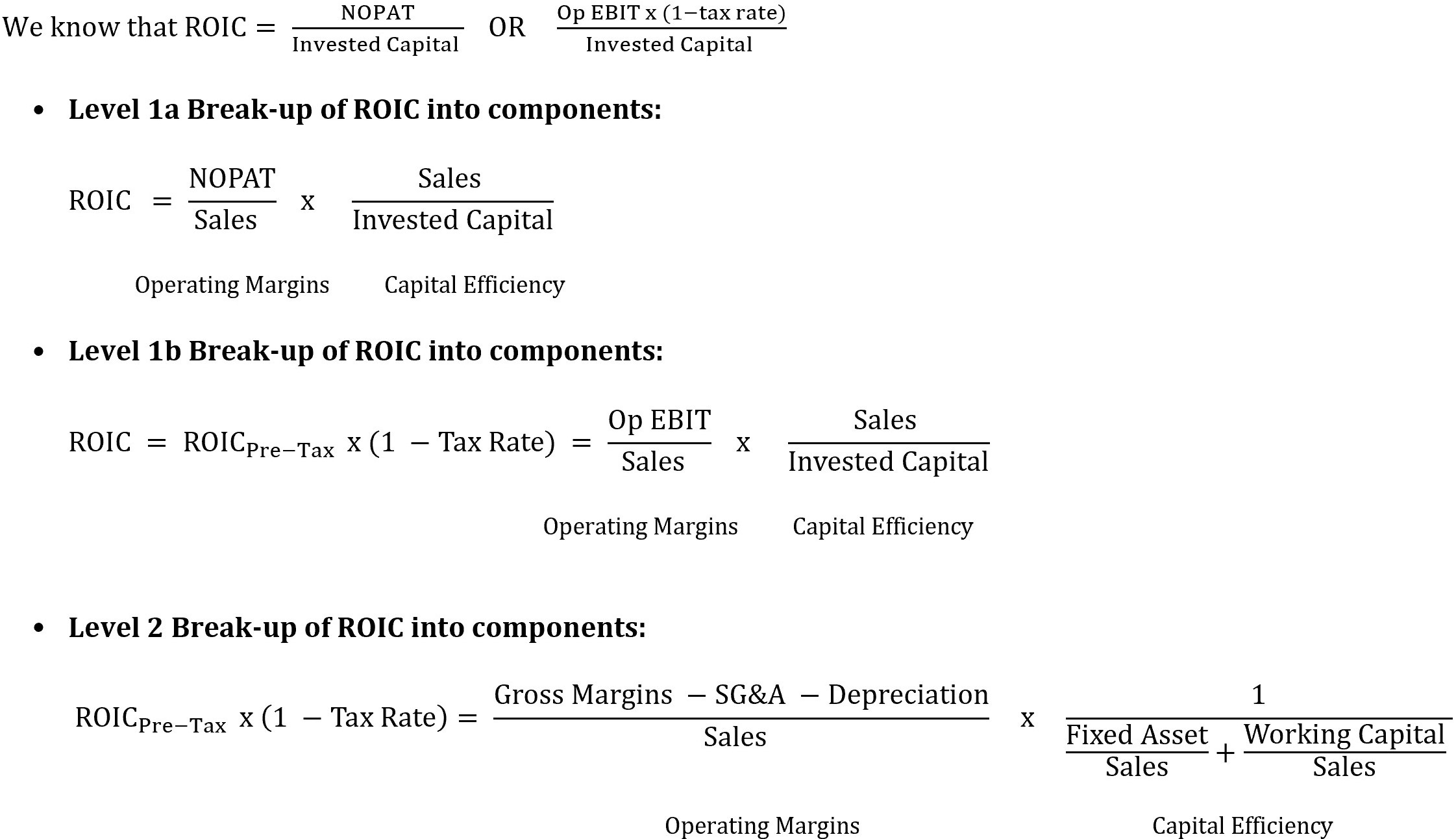

Breakdown of ROIC into its components

Just liked the popular DuPont Analysis, ROIC can be broken down into several more components as follows:

At the first level ROIC should be broken up into Pre Tax ROIC and also broken down into Operating Margins and Capital Efficiency. Most people stop here. However, one should continue. At the second level ROIC, Operating Margin is broken down into Gross Margins, SGA and Depreciation. Capital Efficiency is broken down into Fixed/Sales and Working Capital/Sales.

Working Capital/Sales can be further broken into Inventory Days, Receivable Days and Payables Days (as long as ALL of them are calculated using Sales)

Predict your own ROIC

Many a times, you can have a view that the margins, asset turnover of a company will become better/worse. You can use the ROIC predictor file to translate your assumptions into operational impact on the company’s return. The caveat here is that to get a proper measure of ROIC (or any other measure of return) accounting numbers need to be adjusted.

There are instances where ROIC is not the best measure to analyse returns. As stated earlier, for financial companies, ROE is the best measure as finance costs are a part of the operations. Furthermore ROIC (or for that matter ANY measure of Return) do not work well when the denominator starts approaching zero.

ROIC can be compared with the Cost of Capital and can quickly tell you whether the company is

destroying or creating value.

Hope this write-up is useful.

. Only once a company meets all items in your checklist should you consider allowing it to enter your portfolio

. Only once a company meets all items in your checklist should you consider allowing it to enter your portfolio