My notes from Q2’FY 19 Concall:

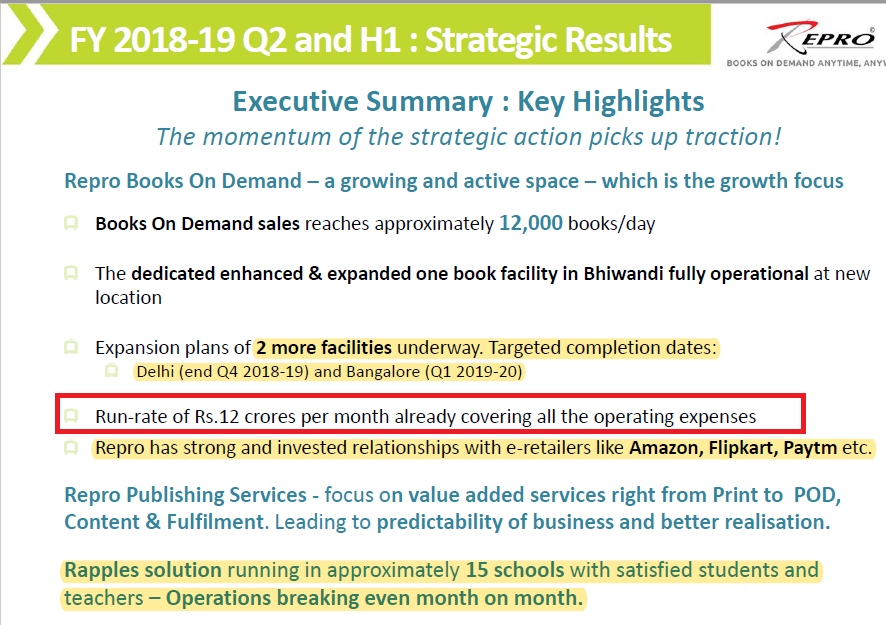

12 Cr/month online books : Able to meet all expenses, still, focus remains on top line to grow

market share for next 12-18 months and capture large market share without bothering much on bottom line as of now

Major focus : Amazon, Flipkart, Paytm

Traditional print : Better predictability, realization and good cash flows happening

Rapples : Continuing in same set of schools and doing break even month over month

India : 10% books old online whereas in USA 50% books are sold online

Bhiwandi,Delhi,Bangalore: 20,0000 one book model (Mumbai up and running at 6000 books per day enhanced to 12000 daily capacity)

Different capacity for advance printing , pre-print: 20k per day in Mumbai and will be adding in Delhi also, will go 40,0000 per day

Current utilization is 60%

Lot of sellers selling online by picking from publisher directly on an inventory based model. As of now, no one doing on demand model

25-30 Crore investment in new facility and warrants will be converted which were done earlier. New business does not need working capital. Old business is stable. So, debt will be maintained or will go down

publishing business margin looks stable and good long term contract in place wit large publishers. Not going to grow and add capacity but some growth through value added capacity

2-30% margin on various books. Overheads wont grow and should add to bottomline

1 book to 1000 book half the cost

School book business : Sales team on ground approaching schools but actua implementation will happen after Dec during Feb, March

Govt policy impacting publisher could be a risk. Trade books like fiction growing. Books going digital is risk but we are invested there through amazon

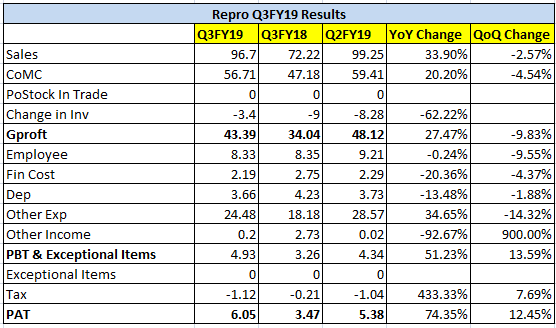

QoQ Other expense is up due proportional export freight and forwarding charges

From past trend, confident to show good growth and trend should co

35 cr quarter export n 48 cr in H1 n its picking n doing well n we r very conservatively doing well. Trend looks positive for growth. Out of 73 cr order book, 61 cr domestic and 13 cr export

Operating cash flow : for current quarter : 16 Cr

Ingram share of books on demand : 10-15%. Have been able to scale up partnerships with domestic publishers

7 cr loss to 1 cr loss at PBT level. Right? Any spike in loss due to 2 new facility coming up?

How to retain market share?

retention of publisher is key to retain market share

Repro Innovative Digi print Limited: What business? 4.8 cr investment ? no revenue and salary expenses?

macmillan business, stopped operation n all print capacity shifted to surat

Paper prices?

with a lag, will be able to pass it to customers

Share of sales from Tier 1 city and Rest?

19-20% growth, tier 1,2 n 3 contributing. amazon strong in t1, flipkart in t2, paytm n others in t3

growth in e-commerce online book 50-100%

online book 4%

Margin pressure from channels:

We need scale to become large enough so that others cant ignore us and hence building scale and having publishers

Is industry doing anything to fight with piracy?

Big problem in India and with big amazons it is becoming apparent n whenever they see they are taking action. so hoping better future

Investor Presentation : https://beta.bseindia.com/xml-data/corpfiling/AttachLive/96b4e1c0-6051-4afa-af04-8323b75face9.pdf