Waiting for @kunal28parikh 's view on q1 numbers… @suru27 thanks for ur valuable notes

I agree with @suru27 assessment completely. I attended the AGM too yesterday.

Here are some views:

-

Company has hit the run rate of 9000 books per day. This is a good run rate although one interesting thing that Mr. Dhruve mentioned is that in printing business one cannot function more than 80% capacity. They have already increased the Bhiwandi capacity to 12000 but further growth will be less in my opinion till the Delhi or Banglore plants do not start

-

According to Mr. Khera, once the Delhi plant starts, the revenue should shoot up by 30% -35%. It is expected to start later this year.

-

On academic front, I was frankly disappointed. Given there is so much happening within E-Commerce, going into K-12 segment might be distraction. Also, the Ingram titles need to be uploaded more quickly. It seems that they are now also focusing on Indian publishers. Ingram titles are high margin but low volumes. Also, to upload titles, Repro will have to convince the original publisher who is working with Ingram. This was suppose to be time consuming but I still feel the pace could have been faster.

-

Till Jan or Feb we would not see much action on the academic segment as the year has already started. I can understand the reasoning why they want to go in academic market, since more than 50% of market is there. But it will take a huge infrastructure(building a sales team, competing with existing distributors, etc.). They could have concentrated at testing books and trade segments more but let us see how they execute this.

-

Other insight provided by Mr. Khera is that they might start spending on their brand too this year. This is important as to reduce the dependency on e-commerce partners in the future. What he means here is, say Repro adds a Menu button on the website, and that leads to the Repro E-Commerce store, this will create a channel for them where they will be able to sell to customers directly. This can be very interesting if done right as Repro will be able to extract more margin as they will bypass e-commerce sites. But this is still under experimentation but I would bet more energy here than the academic market.

-

School Textbooks: Repro has listed 1000 books under school textbooks. Check the competition here. Now curriculum does not change very frequently for school books. The competition is not going to go for digital printing but for offset. Apart from E-commerce sale, the competition has great tie-up with schools(and more importantly corrupt staff/trustees who get commissions on these).

-

Since I am active on this thread, I should also disclose that Repro is still part of my portfolio, but I do feel it is a risky bet and a lot will depend of implementation by management.

5 Likes

Completely agree, it is totally wasting of resources, what u want to achieve at the end of the day!! ?

If they want to balance risk of dependency than also its not the right way…

On my view they can choose 2nd option to make "Repro e-commerce "…where they will get futuristic value.

If you can elaborate it…Good to listen about that point…

@kunal28parikh On school book part, there could be a different view. My understanding from concall was “they are doing it ALONG WITH AMAZON” and I think the bold words might be important in case this is getting driven by Amazon. Any clue on this? My sense is that Amazon wants to make inroads in various B2C retail businesses of India where there is an inefficient business model by bringing online/hybrid set-up. I believe Amazon is trying to do similar stuff in pharmacy. Wherever they see huge market size opportunity where there is an inefficiency which they can fill, it might be interesting to them. So, key question is - Is it being driven by Repro and Amazon is just a name there for branding or Is it getting driven by Amazon where Amazon feel that Repro is a right partner to do the same. These 2 scenarios can play out very different based on who is driving it. Any clue or thoughts on this?

One more thing, in concall, someone asked that as schools get a cut out of it, wont they oppose such move and management’s answer was that it adds value to school, publisher and parents by saving their time, simplifying things and reducing administrative burden. What cut school gets that is a deal between publisher and school and they can decide between them and Repro will not have anything to do with that. They will charge for the value they are bringing to table for all the stakeholders. So, yes it is a grey area but that is the defence

1 Like

From my very very limited knowledge of the publishing industry, my opinion is as below:

Schoolook delivery seems a good idea, if they are able & confident of cracking it. It’s a predictable business, working capital light (being pay first, deliver later model), capacity utilization point of view(offset & digital), market share gain (weakening the rivals), introducing parents are to ecom world etc

Disc: invested

1 Like

Dint they mention even if they have 12000 books/day capacity they can actually print 3 times that no. So there should not be any capacity constraints in growth. Or please correct me if my understanding is wrong.

Went through FY18 annual report and wanted to share few items that intrigued me:

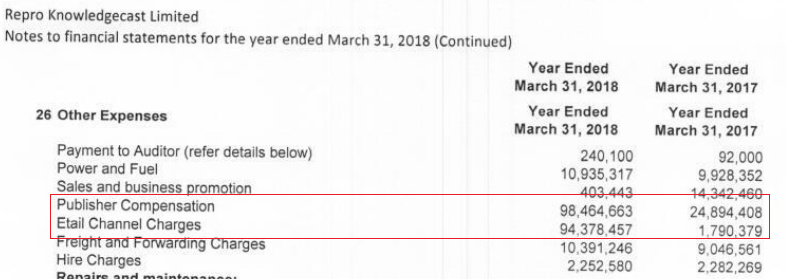

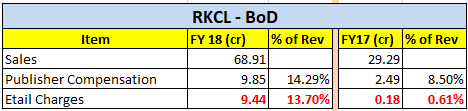

- For BOD (RKCL) business, I see big jump in Publisher Compensation and e-tail Charges expenses for FY18. When I compare these numbers as % of sales - sudden spike in e-tail charges don’t make much sense. My guess is that management started recognizing BoD revenue gross of e-tail charges for FY18, whereas, they were recognizing net of e-tail charges for FY17. Being conservative they should be recognizing revenue net of e-tail charges, if Amazon pays them after deducting their cut. But something that we need to confirm with management.

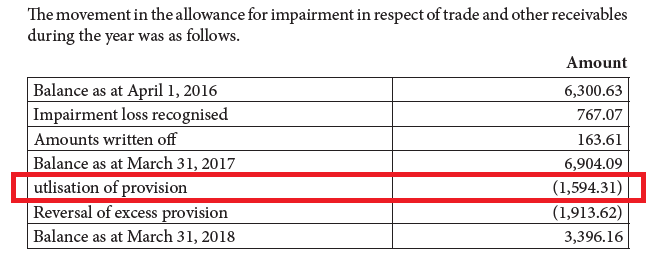

- Below screenshot is from page 227 of the annual report. It shows movement in allowance for impairment for receivables. I don’t understand the 15.94cr amount for “utlisation of provision”. I don’t see it’s impact on FY18 financials. Will be great if someone can educate me with what this entry is about. I do understand that below entry of 19.14cr is the amount that they recovered against receivables that were written off previously. Also see this increase in cash in receivables item in CFO. But don’t understand “utlisation of provision” line item below.

All views/comments invited.

Disc: invested

1 Like

Repro Innovative Digiprint Ltd: a wholly owned subsidiary of India: does anyone knows what do they do…they have a rev of 39 lakh but an employee cost of 5 cr, other expenses of 1.2 cr and a loss of 7.2 cr. Repro India has given them a loan of 19 cr. how will such a company ever pay back a loan of 19 cr plus they are accruing interest of 1.7 cr towards repro india and paying TDS / taxes on it for no reason.,plus parent company must be showing this as income and pay taxes on it

why is repro india investing money every year in a company that is not doing anything,

1 Like

@ajay81 sir could you please mention source of information…

My initial perception is ,there must be some confusion ,otherwise management seems to be very much transparent.

one hand they have JJ irani, malabar and vijay kedia on the board and other hand they tied up with company like Ingram Group. with such a promising environment they never do mischievous things like you mention.

Digiprint and Knowledgecast are 100% subsidiaries engaged in Rappels or BoD biz and both are making losses. I would worry if these were promoter controlled entities.

BOD comes under RKCL so digiprint has nothing to do with BOD…

And this quarter BOD turns profitable…

This is my understanding. It has only 2 subsidiaries : 1 for ebook knowledgecast (67 cr turnover) n 1 for rapples (innovative digi). Now based on my understanding of all concalls ( will try to find the exact sections), innovative digi is for rapples were they did a PoCs on few schools for this business n marked these PoCs as expenses (i remember in some concalls they said it) n it created some revenue in 16-17 but off late they ve put rapples on back burner n not discussing which might lead to 0 revenue from this subsidiary (n they said perhaps timing is not right n they ll come back to this on appropriate time). So, thats the possible reason what you see in numbers n we can check with mgmt in next concall.

1 Like

Just to clarify i am not casting anything on mgmt…was just trying to check if anybody has knowledge abt Repro Innovative Digiprint subsidiary

as such from Repro Innovative BS FY18 (its available on the site):

their revenues have fallen so much from 7.8 cr in FY17 to 39 lakh in FY18 (39 lakh is all scrap sales so no business this year) but expenses havent reduced one bit, cost of materials has increased, employee cost has increased…it just looks surprising that you are winding up business and still increasing employees,i wasnt even able to findout even what this subsidiary exactly does now

RKCL (handling BOD) is also ebidta -ve but there revenues are increasing at a fast pace and you are betting on operating leverage helping you convert into profits in some time…not sure i can say the same abt this subsidiary

the Intercocporate deposit is given by repro india and it increased from 11.5 cr last year to 19.1 cr this year

3 Likes

Repro Innovative digiprint is 100% subsidiary of Repro India. Loan is given to this company to setup Chennai plant as this company will be managing operations of Chennai unit. Plant is still not operational hence income is not there and minor expense is there. Vijay Kedia, Mukul Agrawal, Malabar Fund are top investors and they have invested lot more money in this stock than us so there won`t be any corporate governance issue in this cos …

It would naive to think that just because some famous investors have invested into a company, there would not be any corporate governance issues. One needs to do own’s due diligence before investing…

In presentation it is mentioned 12 crores run rate per month is covering all operating expenses, looks like from Q3 BOD will be break even. what’s your view on the results?

Q1 BOD did brak even at EBITDA level. If we see Q2 standalone and consolidated numbers, it looks like from Q2FY18, 7 Cr loss, BOD is down in Q2FY19 to approx. 1 Cr loss at PBT level. Considering new BOD centers coming up in Q4 and then Q1’FY20, there could be an initial spike in expenses with respect to revenue and hence, I think PAT level break even though can happen anytime soon, might get a bit delayed on a consistent basis due to projected ramp up in new facilities

Disc : Invested

1 Like