Any updates/scuttlebutt here? The number of reviews on Amazon have kept going down as can be seen at this link

The total reviews over the last 12 months had crossed 10.5k in the last quarter. Any news ?

Now its a complete missing what they projected earlier …

1)the bubble they have created in terms of daily book sale numbers was broken so to hide that failure they separating “Stock sales” and POD numbers.

2)In actul term the whole POD story was over projected it will take 3 5 years to reach atleast 100cr yearly sales and that will translates into 10 12 cr peofits.

3)In Q4 Total Books sold per day was nearly 10000 out of which 3000 books POD remaining was stock sales.

4)The management was second time came out as story teller first Rapples and then BOD/INGRAM/E-COMMERCE.

Its just a publication company with good management …

Corrct me if i am wrong …

@kunal28parikh @suru27

Expecting 20% steep fall in the counter…

Sooner or later it will come to its actual value which is merely Rs.350 - 400…

Whole story was riding on Ingrams massive portfolio of Titles. which now looks like Inappropriate or Irrelevant to indian market…

They have uploaded 5 milion titles which gives 4000 bpd sales.

One thing is clear when there are 4 5 decision makers company will never creat any significant wealth …

i have to choose between Vaibhav global and repro on that basis (sunil agarwal a 1 men show) i transfered 50% of my repro holding to vaibhav which gives some comfort atleast…

Correct me if am wrong…

Thanks

if your time horizon is short term then it’s Okk other wise it is going to be big wealth creator in next 10-15 yrs… Online book selling is future and they are placing at very excited stage to grow over longer term

Focus now will be on margins and bottom line.

800 cr mcap for company like repro completely gives sign of something was fissy…how malabar and vijay kedia agreed for that.

Even for long term what they will achieve lets elaborate

If they sold 1cr books per year with Rs.350-400 per book . Topline 400cr and profit 40-45cr at PE of 25 price will be Rs.1000 that is after 5 6 yrs.

Considering 25% qoq growth which is merely impossible.

Now they are 10lac books per year with ticket size Rs. 320 they have to grow 10times looks like joke.

According to me either Vijay kedia nd sumit nagar are not understanding whats going on or i am over reacting:-)

Thanks

They open up fingers exactly after that malabar money came…so they eventually knew POD numbers are gamble!!!

Not at all expecting from company where Allac padmasee and jj irani was directors…

The entire Ingram story was misinterpreted they have 13mn titles from US. they have very little importance in india otherwise why such company allow repro to earn any handsome money.

If they want to do like Ingram than they have to creat content bank like ingram had from indian authors and this will take many years.

Dear Kuldeep sir, I don’t understand what suddenly change for Repro other then delay in expansion plan that you become so much pessimist in Repro. Kindly provide your concern areas here.

Repro sold book online on 2 ways

1)POD which r mostly ingram titles

2) Stock sales which r indian titles which many people can sale on amazon nd flipkart where competition ia huge and margins r very less.

So 70% of their Online sales comes from stock sales. Which has no meaning at all.

And this was biggest prank they used to fool malabar nd kedia.

And open up this exactly after receving their money.

In hurry ,Sorry for typo errors

Alyque Padamsee passed away in nov 2018.

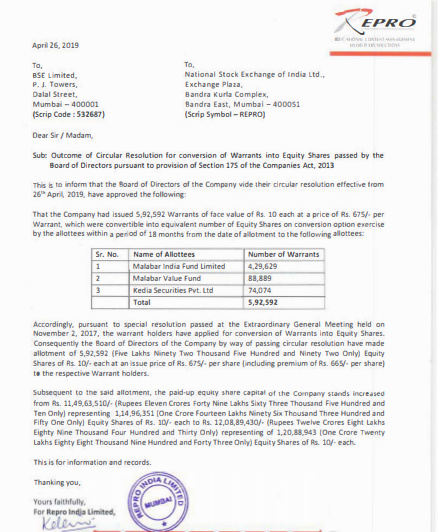

Malabar/kedia money -All that came long back. It got converted recently.

Pressure will be to work on margins and bottom line now.

Last year they said they will double POD books in July2019. Things changed bit now. They are moving out slowly from stock sales to POD. They have to start delhi unit without further delay to make for decreasing stock sales. They clearly said top line might not look good but bottom line will surely improve. They are the best judge after all

Expecting things should change drastically in next 2 quarters.

@parth_dalal

You are not understanding whats going on…

Brother read it twise and think again on it.

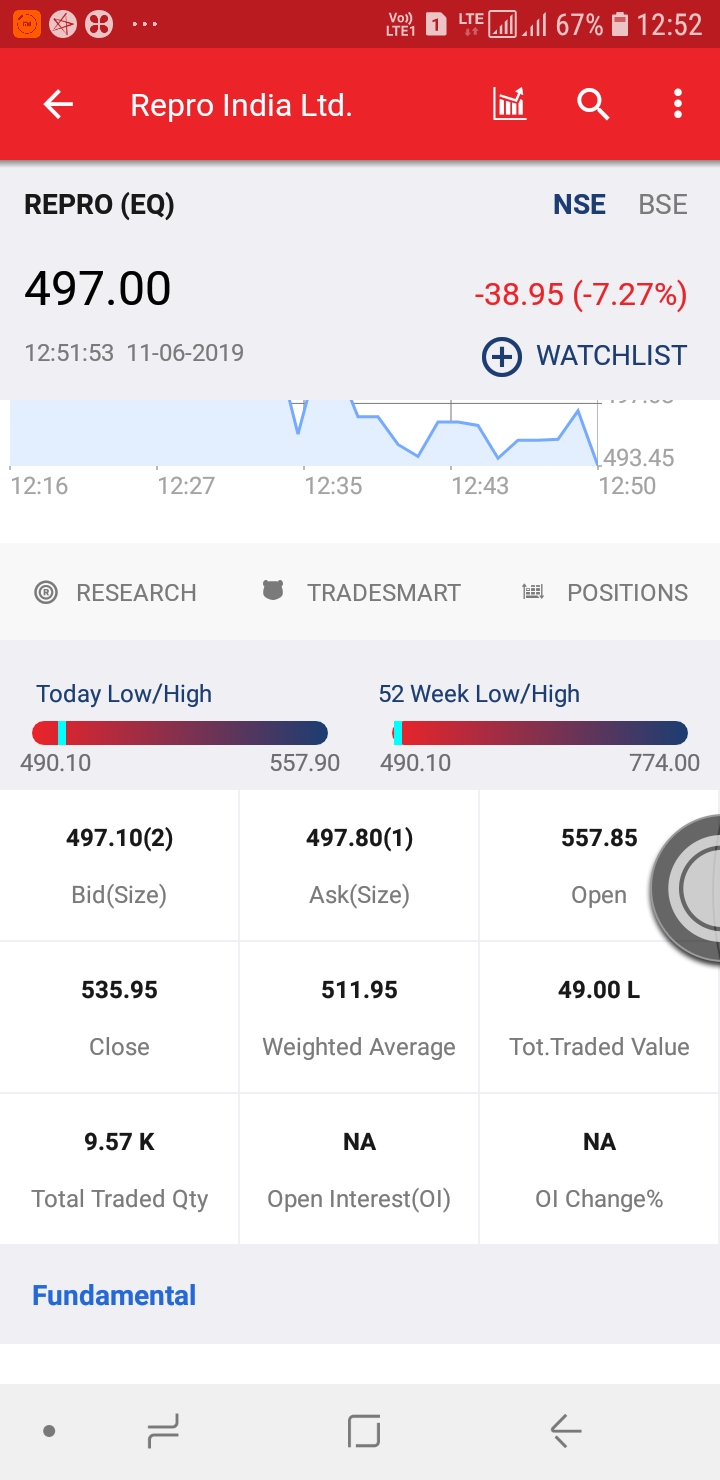

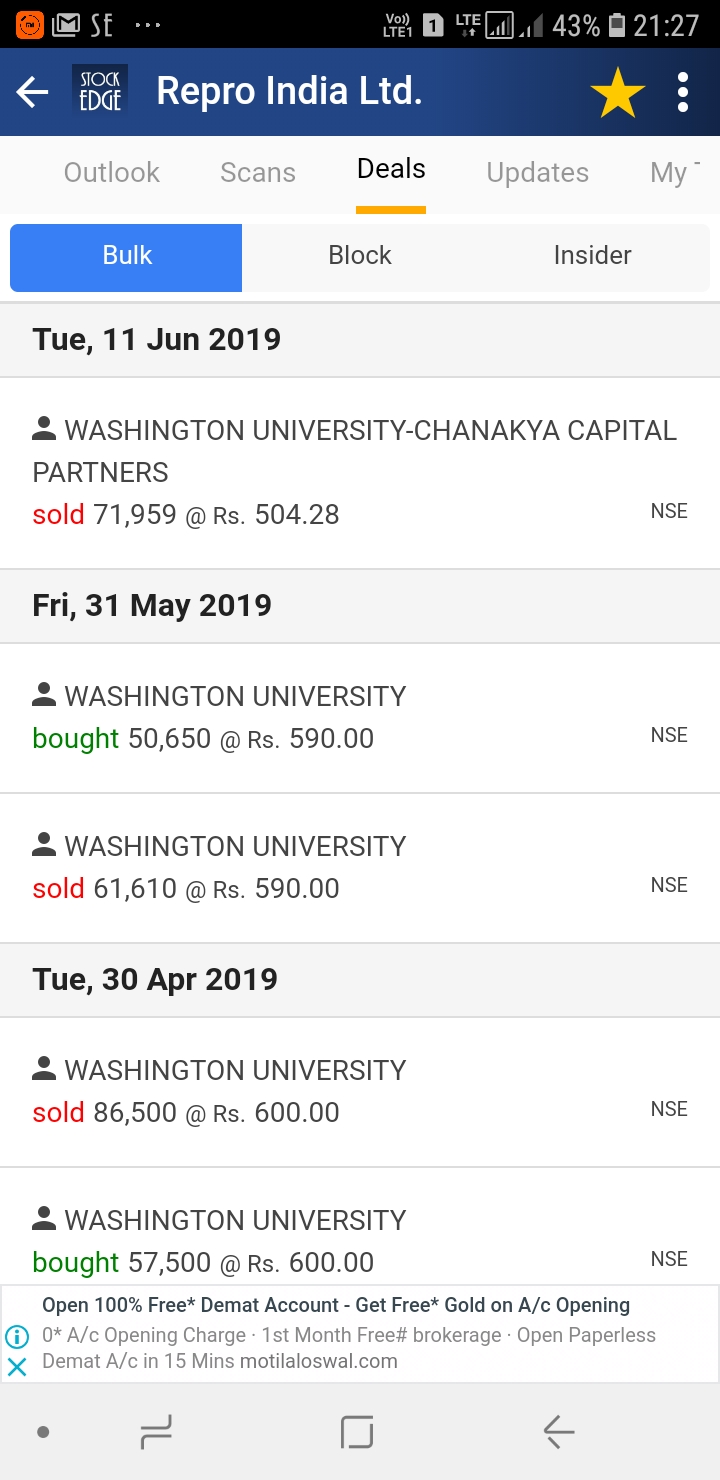

86k volume… Any idea who is selling and who is buying??

Repro India Limited

WASHINGTON UNIVERSITY-CHANAKYA CAPITAL PARTNERS

SOLD 71,959 SHARES AT 504.28

Picture is not clear as delivery % hardly justifies this sale if we go by NSE data. It has been very low for the last few days despite high volumes. I think they have lent the stock to somebody who is shorting the stock to buy at lower levels due to perceived weakness in quarterly nos. Not sue what is the motive here.

I guess they completely understand whole picture so even selling at 600 then 590 and now at 504 levels…total 120000 shares sold by them out of 271000shares

This co. which is also a major seller on amazon claims to have tie up with INGRAM.

N also they have POD facility too.

Now if INGRAM is also having some kind of tie up with this co. then, what exclusivity Repro Enjoy?

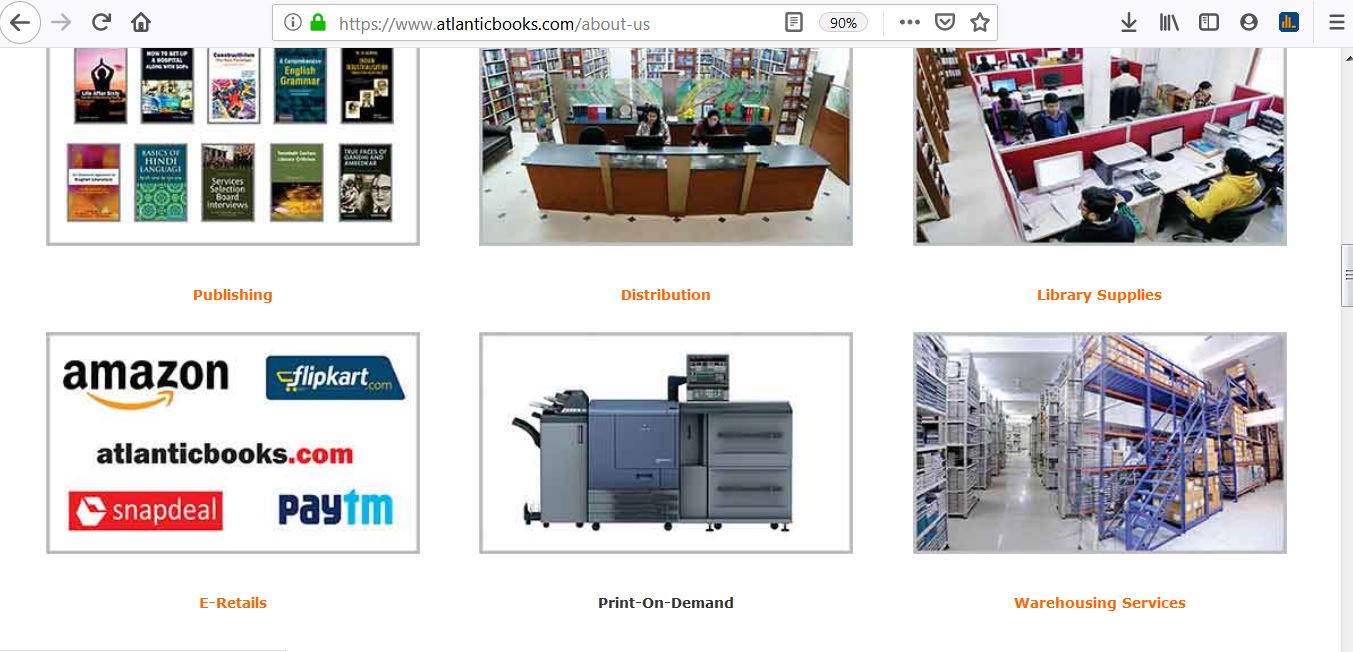

https://www.atlanticbooks.com/about-us

A good find for sure! This company appears to be a large marketing and distribution company rather than an exclusive book printer. If you want to procure from Ingram’s global network, they would be happy to ship you. There is no exclusivity in selling but Repro enjoys exclusivity only in sharing the content in digital form so they could print on demand and sell. This company would definitely compete in the local book publishing and print on demand.

Sir it is a British publishing company, not Indian. Repro said they are Indian partner of Ingram… There many such partners in other countries also