Reliance Capital to exit all non-financial businesses in next 12-18 months; Does anyone knows which non-financial businesses are in the holding of company & how much money it is expected to fetch.

Thanks

Reliance Capital to exit all non-financial businesses in next 12-18 months; Does anyone knows which non-financial businesses are in the holding of company & how much money it is expected to fetch.

Thanks

@manoopatil Following is from the ICICI Direct report:

Investments book

Reliance Capital has transferred a few investments to an SPV post restructuring and being CIC. It funded the same with capital of | 1500 odd crore and carrying similar investments.

All put together, non-core investments are | 10000 crore, as per the management, in the conference call. In the same, media and entertainment investments were to the tune of ~| 6000 crore.

With expected closure of radio business deal (RMVL) in the near term, ~| 2000 crore can come. From Prime Focus, around | 1200 crore is expected. The proceeds will be used to pay off debt on the books. The process of exiting most of these non-core investments is under process.

Exit of Yatra stake in Q1FY19, Sula Vineyards in Q4FY18 and proceeds from gaming company IPO are being used towards reduction of debt.

Greetings!

Have reviewed the balance sheet of the Company. My observations are as under:

a. Investment in CCDs (compulsory convertible debentures) - Rs.7700 Crores - all these are in group companies - I think these are in turn invested in entertainment, gaming and media businesses.

b. Loans to unrelated entities - Rs.8718 crores

c. Investment in Reliance Corporate Advisory Services Limited - Rs.1218 Crores - even though it is a wholly owned subsidiary, it is sort of an investment arm. All investments of private equity in nature are held through this subsidiary, like Grover Zampa.

Company is earning interest on CCDs and loans - hence it is not much affecting the Profit and loss statement, however it has been an overhang on the Balance sheet.

Most of the group media businesses are incurring huge losses and running with negative net worth- like Reliance Media Services, Reliance Broadcast Network, etc. Also these companies have got huge debt on their balance sheets. Investment in Prime Focus, radio business, etc are part of this.

Major subsidiaries or core businesses, even though small, have been doing fairly well and growing YoY, except for life insurance business, which is yet to be turned profitable.

Company has got Rs.1500 crore exposure to Reliance Communications and to its subsidiaries, by way of loan and bank guarantee.

As of now, none of the group entertainment companies are subsidiaries of the Company, hence capital gains will not accrue to the Company on divestment of stakes. What it will get is the repayment of loans - for ex- investment in Code Master was held in Reliance Big Entertainment Pte, Singapore.

In the next one year, lot of things are going to happen. Let us see how much the company would recover on divestment of its non financial businesses. Also, fate of the reliance communication would be known by that time. Share price movement will largely be influenced by these two factors.

Considering present market conditions, i don’t think general insurance IPO will happen during FY2018-19.

Solicit your views…

You have tried to go into detail of numbers which is good thing, but when it comes to bad governance, and especially with anil ambani company, all these numbers add for very little, he cooks the book all the time.the numbers you quoted could easily go to zero or even negative.

The pain of being invested in this counter is too much, and one can only gamble with small amount and not invest in company with suspect promoters.

Problem with ADAG companies is their poor track record in execution. Too many businesses, too much debt and lack of financial acumen. All the companies in the group have been eroding shareholders’ wealth over last 6-8 years. Hence, investors’ perception on the management is not positive. This has got huge bearing on the valuation.

Having said that, I have been closely following up the developments in ADAG companies over last one/one and half years. Off late, now it seems management is serious and trying its best to sustain and grow the left over businesses.

a. There have been sincere efforts going on to monetize Reliance Communication’s assets and repay debt.

b. Reliance Infrastructure sold its Mumbai Power business and reduced its debt drastically.

c. Reliance Capital has been trying to get rid of non-core investments and deleverage the balance sheet. It has successfully divested few investments, however long way to go.

When it comes to reliance Capital, I feel the valuation is too cheap and can be a multibagger. However much depends upon:-

a. Successful completion of strategic debt restructuring of Reliance communication - Reliance capital should get its loan repaid and get rid of corporate guarantee.

b. How quickly and how much the company realizes on divestment of its stake in non financial businesses – hope there will not be much capital loss. Few deals are pending for too long now, like sale of radio and tv business to Zee, divestment of stake in Prime Focus, etc.

c. Successful debt restructuring of Reliance Naval – this will help in regaining investor confidence.

Hi…could you share where did you find this info? It would be helpful.

Hi,

From Codemaster website.

Reliance Big Entertainment Singapore Pte. Ltd (RBES) is still holding 28.5% stake in Codemasters.

RBES is an investment arm of Reliance Big Entertainment India.

Care Ratings has revised its credit rating on RCAP debt instruments by one grade lower. Below are the extracts from rating letter which provides insight into Company’s exposure to group companies/noncore investments:

Detailed Rationale & Key Rating Drivers:

The rating revision takes into account the delay in sale of group assets/investments as per timelines provided by Reliance Capital Ltd. (RCL) to pare down its debt levels. The ratings remain under credit watch with developing implications due to RCL’s continued exposure towards Reliance Communications Ltd. (Telecom Company of the ADAG group; rated ‘CARE D’) and its group companies. Further, the ratings also take into account RCL’s sizeable exposure to group companies in the non-financial business segments having weak financial profiles and requiring continued support from RCL. While some of these group entities have been identified by RCL for divestment, timely exit from these investments will be critical for reducing the leverage at RCL level.

Key Rating Weaknesses

Delay in sale of group assets/investments as per timelines provided by Reliance Capital Ltd

On November 23, 2016, the group announced sale of its radio business and general entertainment TV business to Zee group. The transaction relating to the sale of the TV business has been completed and the sale proceeds of Rs.300 crore were realised on August 16, 2017. The sale of radio business is awaiting the final approval from the Ministry of Information & Broadcasting. The management expects inflow of about Rs.1700 crore from this transaction which has been delayed and is now expected to be concluded by December 2018. The company also plans to sell up to 25% stake in Reliance General Insurance via IPO; the same, however, has been delayed from February 2018 to December 2018. The company has also committed to exit from its media businesses to pare down its debt levels.

However, RCL has been able to achieve only about a third of the total exits planned by the management by September 2018 with timelines for other exits being revised twice in the last one year. Some of the key exits achieved during the period are Yatra Online stake sale and Codemasters sale.

As at the end of FY18, RCL had total exposure of Rs.17,653 crore to its group companies in the form of CCDs of Rs.7,700 crore (P.Y. Rs.6,250 crore ) and loans & advances of Rs.9,953 crore (P.Y. Rs.8,575 crore). These exposures are mainly towards the non-financial businesses of the group. However, out of the total investments in the non-financial business, the management has stated timelines for exits from the Zee deal, Mahindra First Choice and Prime Focus stake sale. Timely conclusion of the envisaged divestments will be critical for reducing the leverage of RCL.

Exposure to Reliance Communications (RCOM) group

RCL has exposure towards RCOM (rated ‘CARE D’) and its group companies which forms around 11% (Fund based: 8% and Non-fund based: 3%) of its networth as on March 31, 2018. The management was confident of recovering majority of this exposure post completion of strategic transactions. However, there has been delay in recovery of the same.

Quarterly results still not declared, any idea when they will be declared ?

Result date is not yet announced. Since the company has adopted Ind AS rules for preparation of financial statements effective from FY 2018-19, It can enjoy extended due date by 1 month for publishing Q2 numbers, i.e. by 15th of December, 2018.

Wasn’t that the reason for last quarter delay too?

Yes. When a company moves to Ind As for financial reporting, it will have time relaxation of 1 month for reporting its first 2 quarters results under new reporting guidelines. It is because they also need to recast previous year numbers under the new system and provide reconciliation to help better understanding and comparison.

-Q2 numbers look good albeit margins being under pressure.

-Stock is trading at dividend yield of 4.68%;company has paid about Rs. 49 in dividend in last 5 yrs.

-Management conference call at 10:00 am(IST) on28/11; need to watch out of commentry(excuse ![]() ) on divesting non-core assets to reduce debt

) on divesting non-core assets to reduce debt

-would like to hear views from other board members

https://www.nseindia.com/corporate/RELCAPITAL_27112018201807_Investorpresentation_30092018_233.pdf

Standalone_Results_30092018.pdf (1.7 MB)

Consol_Results_30092018.pdf (3.8 MB)

Disc - Part of core portfolio, currently in 38% loss; adding on every decline.

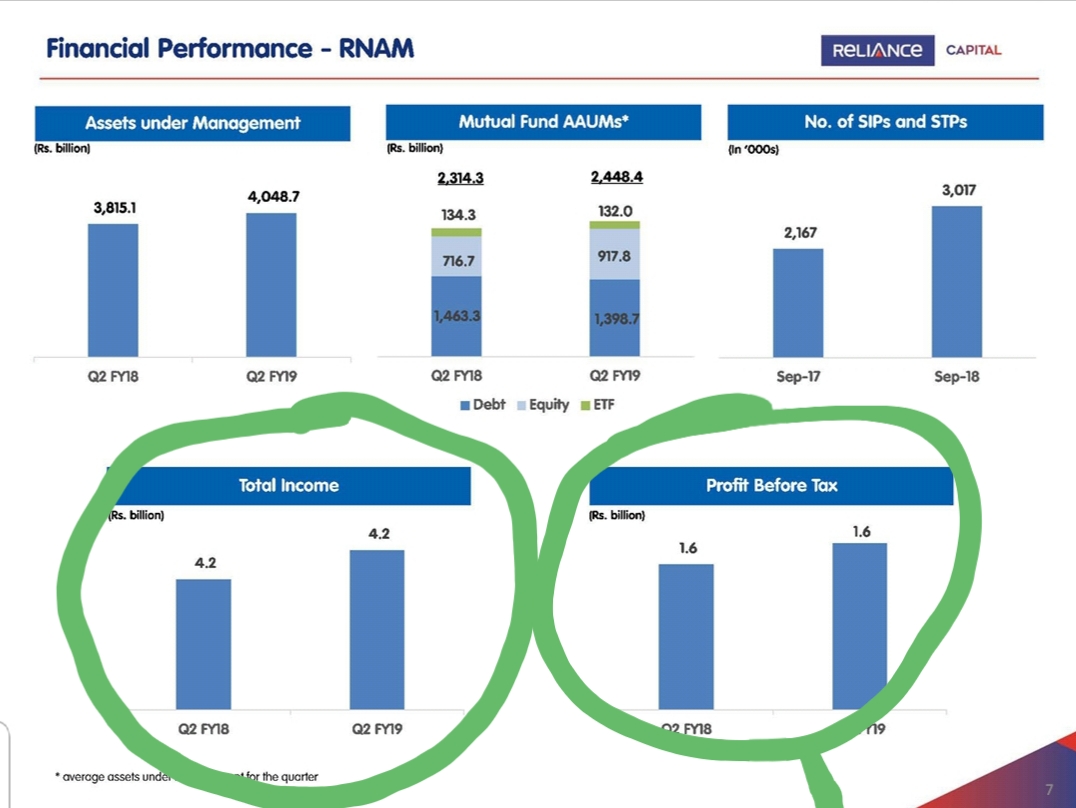

Such graphics are at least a little bit of visual trickery… Not sure why would management allow such cheap antics in investor presentations.

Dear All,

In view of the recent sharp correction in the share price of RCAP, I think it is worth again to review the fundamentals of the company with fresh eyes. I am listing below few recent developments and my take thereon:

It looks like RCOM has cleared all hurdles and now it a matter of few days before it concludes the sale of spectrum to RJIO. With this sale, I believe, RCOM will be, for time being, out of financial crisis and will not be dragged to insolvency. I am not sure whether, in near future, RCAP will succeed in getting back the loan extended to RCOM and its subsidiaries (Rs.1000 crore), but however, it is highly unlikely that banks will enforce the corporate guarantee extended by RCAP in support of RCOM’s loan (Rs.500 crore). Hence, risk level is partially reduced.

During investor concall, the management has represented it is working on following divestments:

a. Sale of stake in Codemaster – valued at around Rs.1000 crore

b. Sale of stake in Prime Focus – valued at around Rs.1000 crore

c. Sale of 49% stake in Reliance Broadcast (big fm) – valued at around 1500 crore.

d. Sale of few private equity investments – valued at around Rs.1000 crore

If management succeeds in concluding the above deals, it can get around Rs.3000~3500 crore (net of outside liabilities in the books of Reliance Mediaworks and Reliance Broadcast Network).

Further, remaining 51% stake in Reliance Broadcast Network still can fetch another Rs.1500 crores, however this can be divested only after a lock-in period.

3. RPOWER owes Rs.1500 crore to the Company. Management does not see any difficulty in recovering this amount.

4. On transition to Ind AS reporting, the Company made provision for credit loss and diminution in the fair value of investments of an amount around Rs.8000 crore. So, the net worth of the Company has been halved! The management feels these provisions will get reversed in future when company recovers advances/divests the investments. To be on safer side, we can consider out of the total noncore investments of around Rs.18000 crore, Rs.8000 crore is lost and cannot be recovered. This amount could even be higher!

5. It looks like Reliance General Insurance IPO will not happen at least for next one year. So the Company can’t count on this money.

6. As on 30th September, 2018, at holding company level, the Company is sitting with a net borrowing of around Rs.22,500 crore (net of cash and bank balance). So it has an annual interest burden of at least Rs.2000 crore. Combined profit sof its subsidiaries and associates for FY 2017-18, attributable to the RCAP was around Rs.710 crore. Hence, it is clear that the Company has to realize at least Rs.1300 crore by way of interest on its group exposure to be cash neutral. Money required for the repayment of principal loan and dividend payouts will be on top of this. I think, this is what forcing the management to divest the stake in its subsidiaries. They sold the stake in RNAMC through IPO and planning to sell stake in General Insurance business. If we see the balance sheet of RNAMC, the company did not need any additional funds for its business. It collected around Rs.625 crore through IPO and in turn paid dividend of Rs.600 crore during the year. It is unfortunate that, because company can’t divest its noncore investments in time, it is selling the stake in its core financial profit making businesses and borrowing additional money year after year.

With the above, we can understand that the recent correction in the share price is led by the concerns associated with the group exposure at the holding company level and not because of the performances of its core financial businesses. I believe, the combined valuation of its core financial businesses attributable to RCAP is more than 20000 crore.

Having said that, following are the positives about the company:

Will positives and profile of subsidiaries outweigh the concerns at holding company level?

Solicit your views please.

Disc: Part of my portfolio and have been adding with falling share price.

Market cap has now fallen to around $500M. Even the stake in RNAM should be worth more than this. I feel the market is punishing the company way more than it should.

Disc: holding

@ bghBharat Did you get chance to evaluate R Capital with current development.

As RPower stock is also tumbling now, do you see difficulty to receive the 1000 Cr now.

Few businesses looks good and company seems to have black&white shade.

Disc: Part of my portfolio and have been added in current share price fall.

As per screener, standalone debt is 20k cr and consolidated debt is at 46k cr.

Hi,

Yes, nothing is working in favor of ADAG companies. I knew, RCAP share price will plummet if RCOM RJIO deal does not go through but did not expect it to touch the double digit! Market capitalization of the group has shrunk to 25% of what it was 6 months ago.

One thing I am unable to comprehend. RCOM repeatedly said, it owns the responsibility to take care of the disputed past spectrum liabilities, estimated to be around 3000 crores, but it is unable to provide the bank guarantee for obvious reasons. If this was the only factor hindering the deal, then what was stopping RCOM and consortium of banks to agree upon a deal so that Rs.3000 crores out of the sale consideration is deposited in an escrow account till the dispute is resolved. Banks will stand to lose much more if the deal does not happen.

In view of present development, we need to analyze the below key issues relating to RCAP:

Lenders have already started uploading pledged shares. Yesterday promoters lost around 4% of their shareholding.

I feel, it is a high time promoters should update the shareholders on recent developments though a press conference/media release.