Introduction

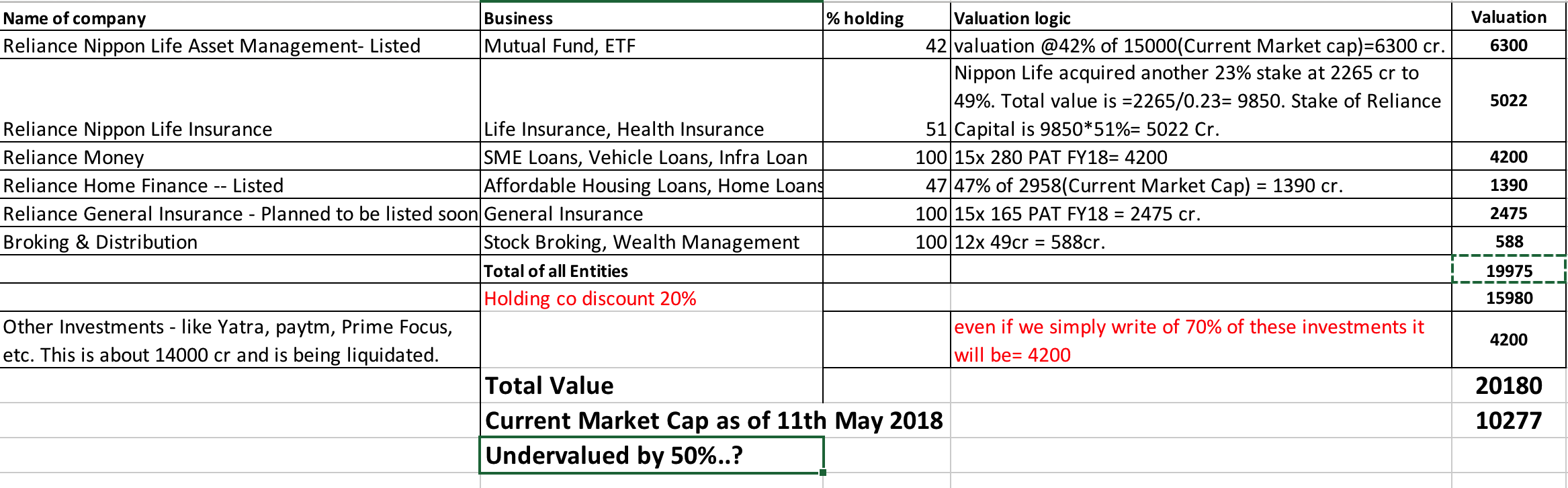

Reliance Capital has the following businesses:

-

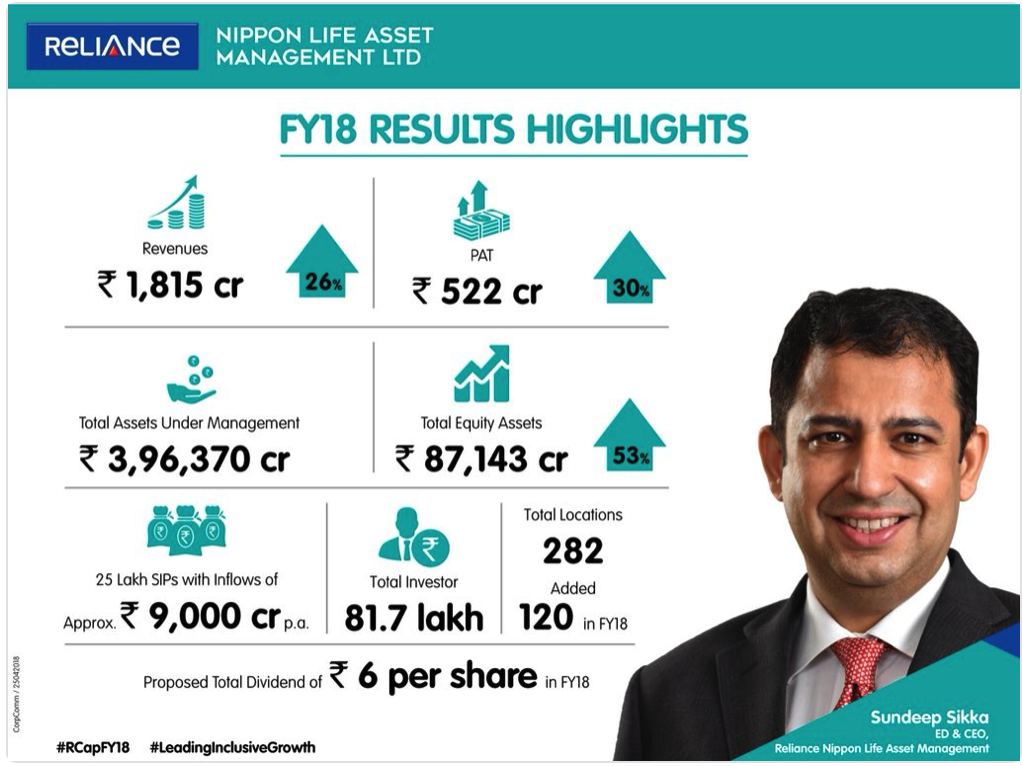

Reliance Nippon Assset Management - listed. Company holds 42% - Business doing fairly well, valuation @42% of 15000(Current Market cap)=6300 cr.

-

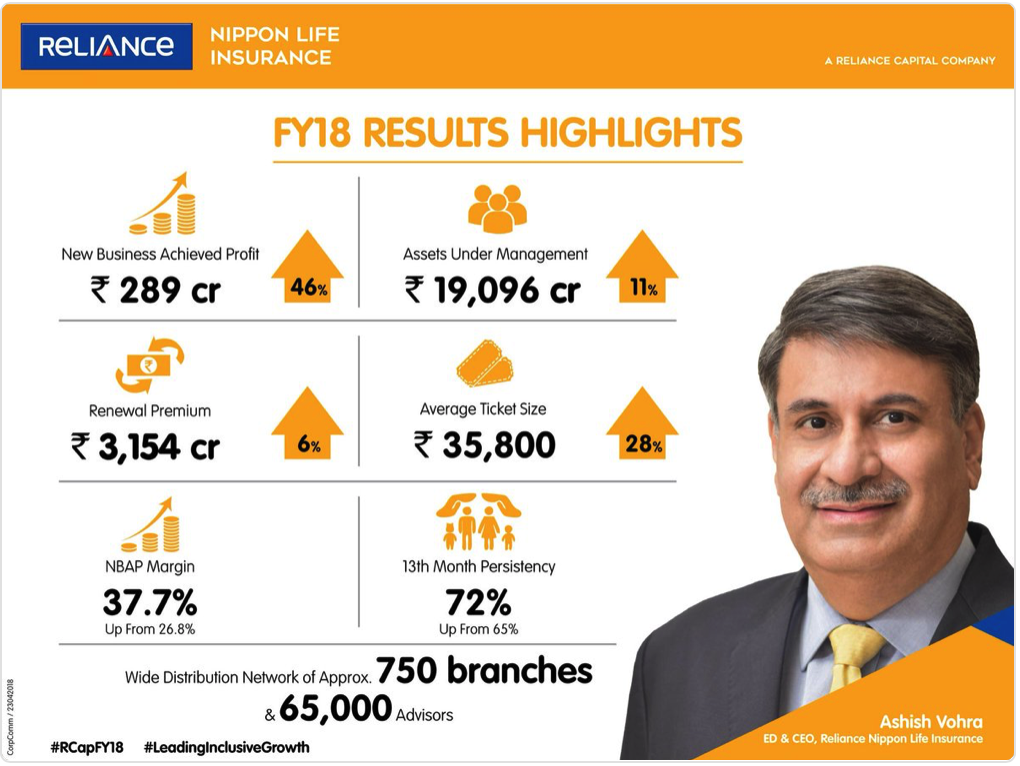

Reliance Life Insurance - held with Nippon. Will be listed/demerged in the future-Nippon Life acquired another 23% stake at 2265 cr to 49%. Total value is =2265/0.23= 9850. The stake of Reliance Capital is 9850*51%= 5022 Cr.

-

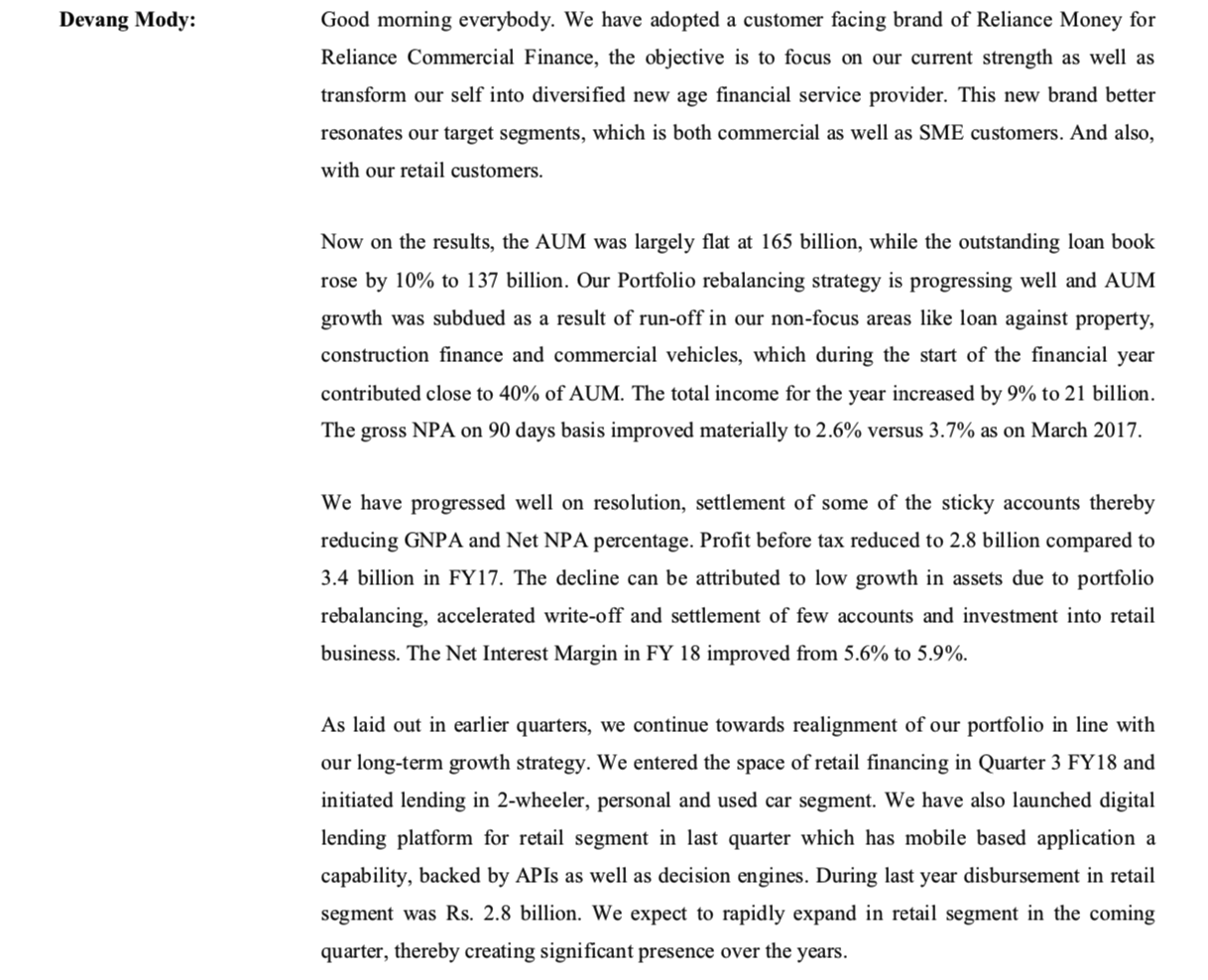

Reliance Money - rebranded from Reliance Commercial Finance. Has more tham 16000 cr loan book, Valuation: 15x 280 PAT FY18= 4200

-

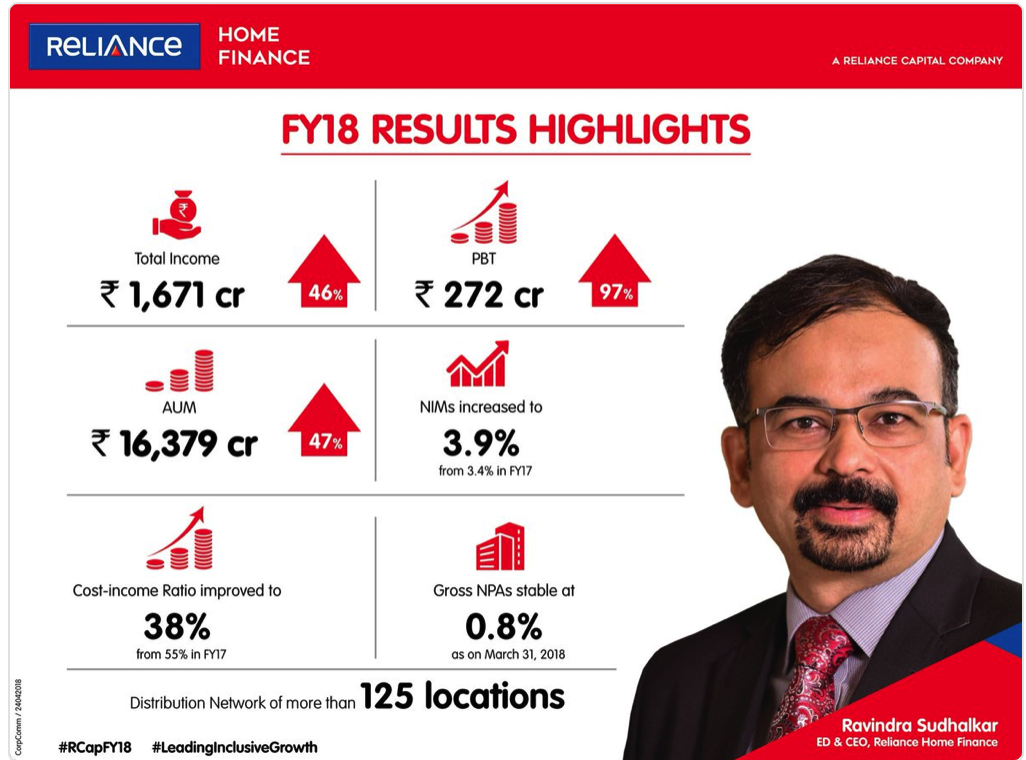

Reliance Home Finance - listed. Company holds 47% - Doing very well, valuation: 47% of 2958(Current Market Cap) = 1390 cr.

-

Reliance General Insurance - held with Nippon. Will be listed/demerged in the future - Doing very well, 15x 165 cr PAT FY18 = 2475 cr.

-

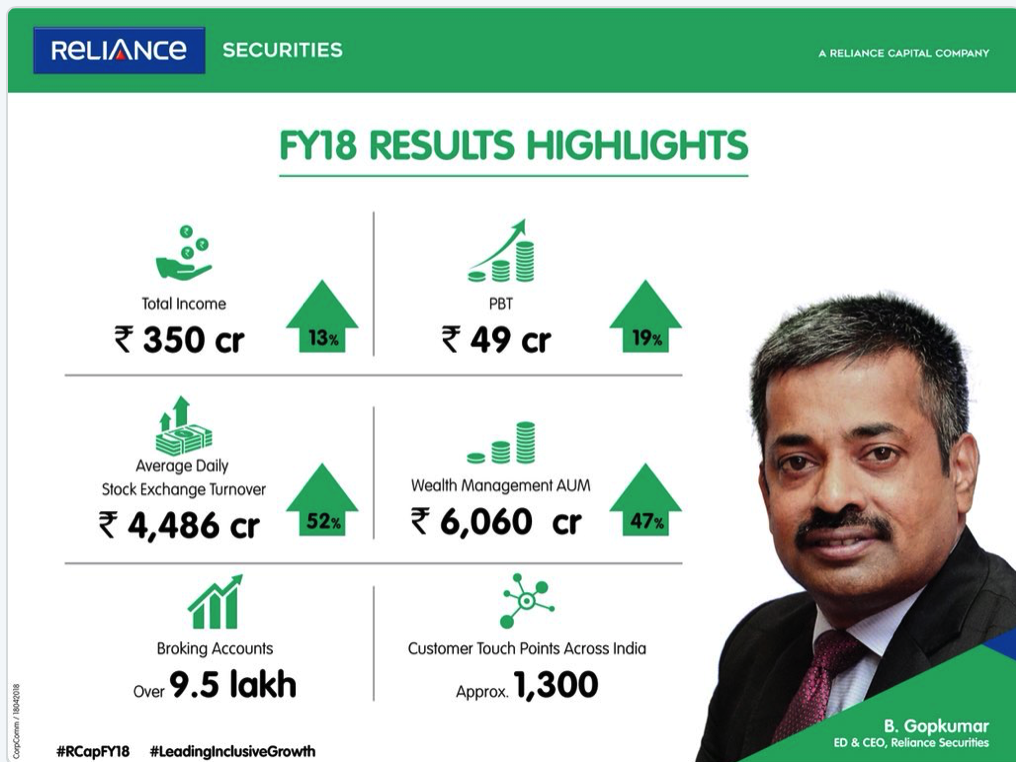

Reliance Securities - brokerage business, valuation: 12x 49cr (FY18 PAT) = 588cr.

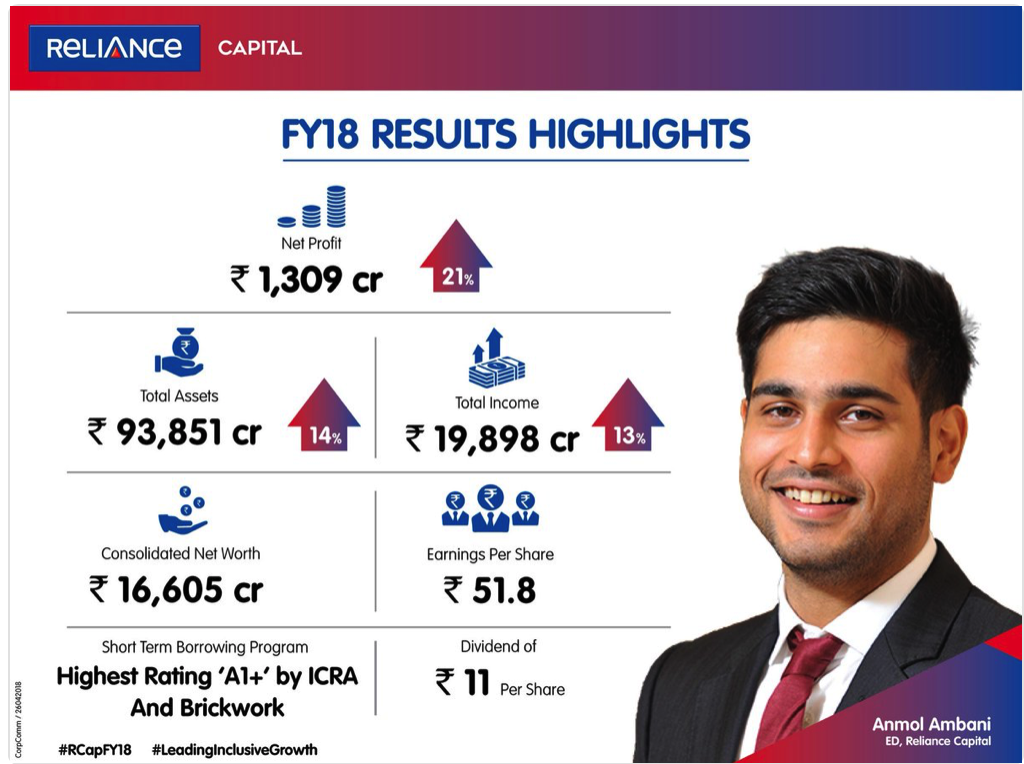

Reliance Capital

Valuation:

Concerns/risks and causes for Huge undervaluation:

-

RCOM default related issue caused week sentiments: although the agreement was done with Jio, but still some delays due to court stay on proceedings. [EDIT] Supreme Court allowed the sale in a relief to RCOM.

-

Reliance Naval is in huge losses and excessive debt: another ADAG group co may go bank-corrupt and can cause further week sentiments on all group co’s, altough Managment stated clearly Reliance capital has no exposure to it.

-

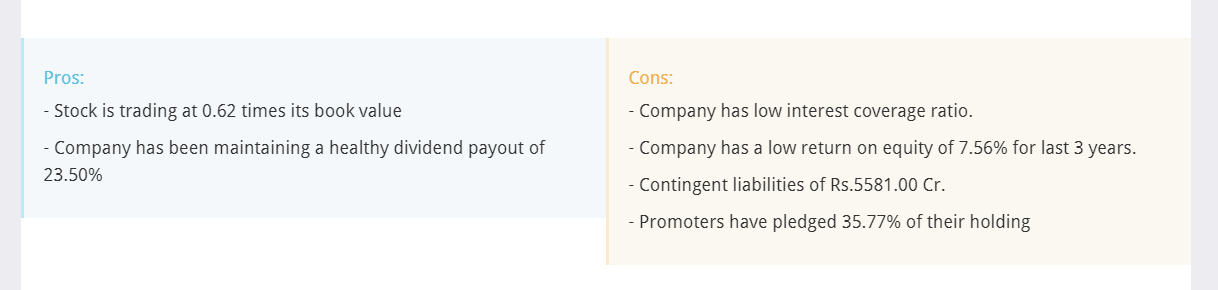

Promoters pledge increased to 70.28% of holdings in Mar 2018 qtr, this may be due to stock price plunge and additional pledge might have been required in order to maintain the loan security.

-

Bad Managment: Anil Ambani is known for poor execution and poor debt management taking huge loans without proper plan or effort to repay them, Maybe his effect will diminish after RCOM & R-Naval debacles, also it is widely perceived that Govt pressure & NCLT has caused enough fear among such corporate to behave better.although one should not invest based on the hope of management behavior change, rather one needs to observe the actions of management.

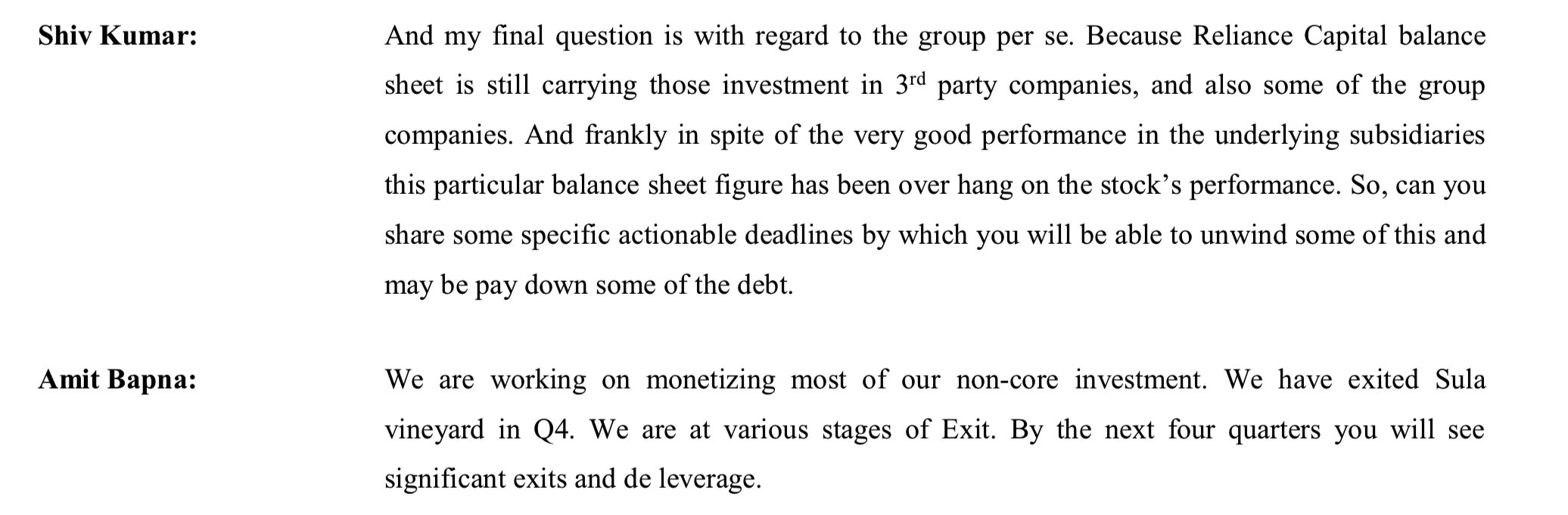

Updates/Actions from Managment on the various concerns: snaps are form the concall apr-2018

- IPO of General Insurance: Managment want’s to time market and accordingly launch IPO

let’s see if they can.

let’s see if they can.

-

Regarding Non-Core Assest Monetization: which are said to be 14000cr, managment sticking to eariler statement and saying all 14000cr will be monetized, lets see.

-

Reliance Naval no Exposure confirmation:

Rationale for Investment

-

Managment Change: Anmol Ambani is leading now, he officially inducted into Reliance cap, and a Father(Anil Ambani) is less like likely to mess up his kids future(Reliance Capital), probably Anmol is inducted in R Cap because this is the best business this family left with, and Anmol is coming with clean slate, rest as long as he is following advice from CEO’s of each business segment, businesses are expected to do well.

-

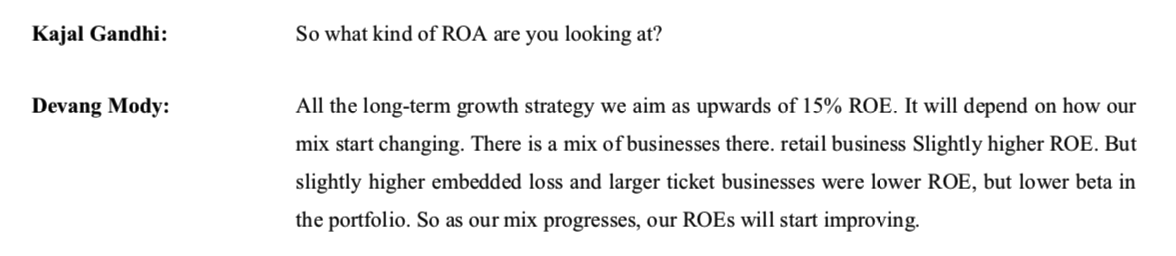

Devang Mody is heading Reliance Money (ex- Bajaj Finance): who was instrumental in building consumer finance business of Bajaj Finance.

-

In RNAM and R Life Insurance, Nippon is the equal partner, so it’s highly unlikely that Anil Ambani will be able to divert funds from these subsidiaries.

-

IPO of Reliance Life Insurance & General Insurance could give decent value boost.

-

Non-Core Asset Monetization: they already divested(Sula vineyard), in advance talks for other asset sales, will need to keep eye on this.

-

Businesses are coming with good numbers: This is the single most important factor of the investment thesis, most businesses are appointed with good Jockeys, and number are coming good, growth and profitability are reasonably decent.

Concluding Thought: legacy bad Managment track record is possibly the biggest cause of undervaluation.

What are the factors which can change market perception of management…?

-

Continous profitable growth across all vertical, which is as of now happening.

-

Taking care of minority shareholders by giving reasonable dividends, Managment already declared an 11rs dividend, which is quite a good yield of approx 2.5%.

-

Sticking with the guidance for non-core divestment, which is already started.

if management keeps delivering good results in the coming years(3-5 years), the market will have to re-access valuations, as in long run markets are weighing machine & all about Future.

In such contrarian investments, one should be against the herd and Correct.

in this case against the herd is for sure ![]() , Correct…? only time will tell.

, Correct…? only time will tell.

Disclosure: I am new to investing, this is an attempt to learn valuation and to refine the thought process and find mistakes in the thesis, Invested, avg price: 425 and significant part of PF.

Note: there are other threads on the forum on reliance cap, one thread is closed and other is generic on Adag group, I wanted to have a separate focused thread so the discussion can be focused and can learn and seek guidance for seniors.

Reference: All the data is collected from publically available information, below are the references, I have copied/edited data from below reference, if this violates the forum norms, Admin may please delete the post.

http://content.icicidirect.com/mailimages/IDirect_RelianceCap_Q4FY18.pdf

https://www.alphainvesco.com/blog/reliance-capital-anil-ambani.

ADAG Group - Investment opportunity or not?.

http://www.reliancecapital.co.in/pdf/Conference-call-transcript-for-FY-2018.pdf