As I said I don’t have any position or view on the company. The disclosure just seemed to be vague and issued only to meet compliance requirement - not the standard expected from a “quality” company. Check out Titan, Dabur, Bajaj Finance disclosures and see whether they are more useful from a small shareholder’s perspective to figure out what’s going on in these companies.

1 Like

Great highlight. Though I have to study the company in detail that is their ARs etc. But from what I have found out is that companies which in which promoter gave themselves salaries to the exact limit for multiple years, were kind of red flag for something that could happen in future. You can read more about it on Vijay Malik site where he has an article about how promotors take advantage of the listed co at the cost of minority shareholders.

2 Likes

High salary with splendid business performance can be a good aspect also. Management taking salary and delivering could also be an indication that they are not swiping out money. Rather taking it legally.

Just a contra view on salary

7 Likes

Second that point, look at CCL products, Balkrishna industries and Alkyl Amines and their performance. When you take an attribute too far it actually becomes counterproductive. Nothing against Dr Malik, but I think if we scrutinize each and every item too much without looking at the context of things. You will hardly ever invest in 5-10 stocks without considering other drivers of returns like capital allocation, tailwinds etc

3 Likes

Q4 FY20 results are out, highlights

Q4 sales down by 17% YoY and PBT down 12% YoY

Diluted EPS 9.10 for FY20

Also could someone please explain what is Depreciation and Amortisation Expense of 109.42 for FY20 this has lead to an increase in net cash generated from operating activities to be up by 158% for the year ending March 2020

Also there is this notice to cancel this years dividend

Would high PE be now retained by relaxo, this quarter seems a big blow to the Relaxo growth story(PE 81.94).

Is this a one off or are the micros changing

Coming quarters are to be more carefully monitored, brace thee ride!!!

I guess 10-15% immediate correction in price because of lower than expected earnings are due!

6 Likes

Has there been information on opening up of their own stores? Just opposite to my house in Delhi, their own stores is still closed and yet to open where all other shops have opened. This quarter results is going to be severely affected for their sales for sure.

1 Like

The decline in PAT looks fairly nominal at 4.7% from 54.42 to 51.05 Cr YoY considering recent developments. Mr Market should have already discounted a muted Q1FY 2021, and the long term fundamental story should remain intact here especially considering the market share of the organised players being still minuscule in the overall footwear market.

2 Likes

I was looking at the balance sheet. The cash and equivalent is only 4 crore. For a company of this size, isn’t it very small ?. Especially during the covid crisis. Of course, they can tap the debt market easily.

The current prices are somewhat near pre crash prices, also the 50% increase from bottom was largely attributed to the growth story, which is proved wrong, also I don’t think the current prices discounts the muted Q1FY21, just to maintain the pre crash PE levels the current stock price should be 12% lower.

Also I hear this very often that the market share of the organised players being still minuscule, someone claimed it to be wround 5%, I went through Relaxo presentation, they say organized players market share is 45%.

3 Likes

Great discussion going on.

Relaxo has been the most interesting puzzle in my investment journey.

You wont believe I have been tracking it since its coverage by sanjay bakshi in say 2013/2014.

And since then I have been convincing myself - " aur kitna chadhega" ( how much more the stock price can go?)

But since last year after its covered by Saurabh Mukharjea of Marcellus, the FOMO ( Fear Of Missing Out) is creeping in. And I have been getting in & out of this stock.

But Relaxo keeps on puzzeling because as per SKMohite post above, it produces 7.5 lakhs per day and if we take production days of 250 ( being conservative) so total 18 Cr per year.

And India’s population is 130 cr.

So at least for me, Indian market is already saturated. Now the further growth may come only through exports.

One trivial thing which keeps me attracting to it - is the 30% discount coupon (on Relaxo products at their stores) they send to shareholders.

Means why not to avail this 30% gain(?) being a shareholder.

But my personal thinking is now it may start trading at sane valuations just like Page Industries.

Page had fallen all the way from 32k to 16k i.e from PE of 80 to 50.

So maybe PE re-rating may happen.

But again I maybe wrong.

Disclaimer - I have invested around 700.

2 Likes

The earnings have seen a dip in the last quarter. Typically when earnings disappoint it is obvious that stock price does correct. Interesting however is the fact that the price hasn’t corrected on such results. Given that the footwear market includes large unorganized players, the market is probably pricing in the scenario where the Covid Lockdown (which is yet another event like Demonetization and the GST event) cause a wipe out of some of the unorganized players. It will be interesting to watch if Relaxo will gain in market share and sustain it in the upcoming few quarters

3 Likes

Yes. This is knee jerk reaction by market.

But again it’s trading at PE of 81 the same PE as of Nestle India.

Relaxo has still quite competition from Bata and other brands like Paragon , Lunar etc.

While Nestle is almost monopoly in both Infant feeds , Nescafé and Maggi.

Yes. There is no doubt about the possible growth and market capture by Relaxo in future.

But even brand like Titan which is also a market leader in many different brands is trading at PE of 60.

So I feel PE of 80 is very expensive for Relaxo.

Maybe the valuation is justified around 50-60.

Again my personal opinion and I may prove wrong.

Regards,

Vikas

1 Like

Few points on Relaxo from Q4 Concall …

- ASP for the year FY20 increased to 135. Realization on per pair basis was flat for last few year but it has increased 8% in FY20. As per management this 8% increase is a function of Price increase taken + more sell of premium product.

2.Direct footwear retail selling point in India is around 85000. Relaxo is present at 45000 selling point. - Export contribution at 4% of sells.

- Bhatinda plant will be ready in next 18 months.

- Per Capita consumption of Indian is 1.6 pair against Global Per Capita of 3 pair.

- Sports shoe is where easy Chinese import more prominent. GoI is trying to block it with tariff. Sparx Sports Canvas shoe contributes around 5% to 10% of revenue now. SparX demand is subdue at this time,open footwear is more in demand due to indoor use. But premium Sparx product sell will again start to increase from winter .

- Almost 10% of revenue is from online sell.

With pricing power, growing realization/premium product(ASP way below BATA but different type footwear product they manufacture ), increase penetration in South/West,East and on online Relaxo has steam left.All upto how much PE will give to the business but again with good per share earning costly business become undervalued over time.

7 Likes

RELAXO FOOTWEARS:

Concall Summary dated 2nd Nov 2020

Revenue: ₹575.9 cr (▼7.4%) Net Profit: ₹75.1 cr (▲6.5%)

FINANCIAL PERFORMANCE

- Revenue from operations in Q2 was lower than previous year by 7.38% at ₹575.87 crore. The decline in operating revenue was due to the drop in economic activity because of the pandemic.

- Net profit in Q2 FY21 increased to ₹75.10 crore as compared to ₹70.54 in Q2 FY20. Profit after tax (PAT) margin stood at 13%.

- Profit before tax (PBT) was higher than previous year by 35% at ~₹100 crore. PBT margin was 17.4%.

- EBITDA margin improved to 22% in Q2 FY21 v/s 16.8% in Q2 FY20 on the back of reduced administrative expenses and benign raw material prices.

- Other income stood at ₹5.04 crore.

- For H1 FY21, EBITDA margin came in at 19.6% v/s 16.6% last year. PAT margin was 10.6%.

DEMAND SCENARIO

- Demand saw a volume growth of 2% YoY in Q2 FY21. Volume growth in H1 was -13% YoY.

- The demand from rural regions was higher than that of urban regions.

- The south and west regions were most impacted as Mumbai reopened late from the lockdown and parts of Kerala are still under lockdown. The demand here has de-grown.

- Even in the festive season during October, demand picked up across the season except in Kerala.

- The demand and production gap still persists in the open footwear category as the demand quickly escalated but it took time for the production levels to ramp up.

- Exports demand is similar to domestic demand after Covid-19. The focus is on the major market of Gulf region. A good traction is seen in the important international markets of Africa, Gulf, Central America and Oceania.

- The company always has a capacity cushion of 30%-40% to cater to the additional demand.

PRODUCT PROFILE

- The open footwear category has shown good traction in the quarter with the brands Hawai, Flite and Bahamas performing well. A major reason for this is the work from home practice due to which the demand for formal footwear declined.

- Open footwear has a revenue share of 80% at present. The closed footwear forms 10% of the product profile in volume terms and 20% in value terms.

- The canvas shoe category has not grown. Shoe as a category forms 10% of the overall portfolio.

- Sparx as a brand has seen recovery in Q2 but it remains far from the pre-Covid levels.

- No demand has been observed for school shoes yet.

DISTRIBUTION NETWORK

- The company as on 30 September, 2020 had 396 exclusive brand outlets (EBOs) which contributed 5% to the revenues in H1 FY21. It made 6 new store additions in the quarter.

- The EBOs are display-cum-sale counters established to capture the needs and preferences of the customers. The company has no plans of increasing such outlets (despite it being non-existent in the southern region of the country).

- E-commerce has a share of 10% in revenue. It is expected to increase further by 2% in the next 6 months.

- The number of channel trades and distributors remain same post-Covid while it is being estimated that some dealers might have shut down, especially in the north and south.

- The number of dealers and distributors has increased as the demand for open footwear across the country saw growth.

- The amount of security has been revised for both new and existing dealers to bring in more serious players. The implementation of the same was due in April but got postponed to June due to the pandemic.

- The supply time from the company to the distributors remains at 2-3 days on a regular basis. The distributors have been requested to maintain an inventory of 1 month at all times.

- The same level of margin is provided to both channel trade and e-commerce.

FUTURE OUTLOOK

- EBITDA margin shall not be the same as Q2 in the upcoming quarters as the expenses return to normal levels. However, on a YoY basis, the margin is expected to be better in the upcoming quarters.

- At the company level, a volume growth of 3%-4% is expected in H2 FY21.

- The capex for the year shall be in line with that of every year at around ₹100 crore with an eye on capacity expansion.

- The objective shall be to recover the loss of Q1 in terms of turnover and growth over the next year. Over the longer horizon, a double digit growth is expected.

- Rising raw material prices can be a trouble going forward.

- The management forecasts that the demand for slippers and open footwear shall remain strong in the next 2-3 years due to the adoption of work from home culture post Covid-19 pandemic.

- It will continue to focus on growing presence in the untapped and under-penetrated markets along with focusing on strengthening the brand.

Disc: Invested in Core PF.

9 Likes

One of the facts I came across recently is

Globally Average footwear used by a person per year is between 2-3. And it higher in developed countries

Whereas India’s Average footwear used by a person Per year is close to 1.5 - to 2

I hope you find this useful.

2 Likes

Here is good report about non-leather footwear segment in india.

This report was published in sep 09, 2019

Snippets

==> There is also a renewed focus on the non-leather footwear segment around the world. In worldwide consumption terms, 86 per cent of global footwear consumption has become non-leather by volume. Herein, lies a double-digit growth opportunity which India, the second largest producer and consumer of footwear in the world, is ready to tap into.

==> The footwear sector in India is now de-licensed and de-reserved, paving the way for growth of capacities on modern lines with state-of-the-art machinery. To further assist this process, the government has permitted 100 per cent foreign direct investment (FDI) through the automatic route for the footwear sector.

==> The overall footwear market in India is pegged to grow at 11 per cent over the next five years propelled by developments in the non-leather footwear segment. Globally, 86 per cent of footwear consumption has become non-leather by volume and India is witnessing a similar trend.

==> As per industry estimates, the synthetic/non-leather footwear market in India is approximately 59 per cent of the total footwear market in India.

Disc: Not invested

2 Likes

Relaxo published its Q3 FY21 result. 12% topline growth 66% net profit growth with 22% OPM.0098bcdb-c9a6-40e9-9846-dc6cc47bf915.pdf (1.7 MB)

1 Like

Was comparing Bata with Relaxo. Both companies changing strategy and might compete directly. Will be good to see which one comes out top

Source: Right shoe to get your portfolio running...

9 Likes

A screenshot of something that appeared on my LinkedIn feed.

What caught my attention, that the Deppt head recognises the personal achievement of a Junior & the achievement is also appreciated by the Leadership team as well as its mentioned on Company page on LinkedIn.

I am sure, this kind gesture, would inspire many more stories & also talks about the culture in an organisation.

Disc : Invested.

8 Likes

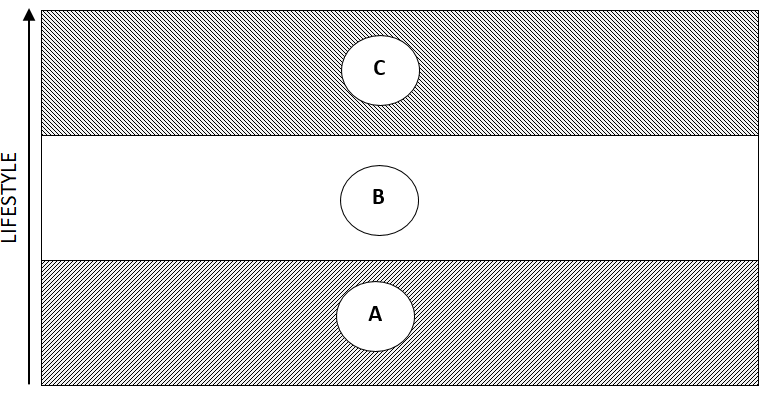

Below is my personal view for this sector

According to me, there are three segments of human lifestyle these days, which define the behavior of buying footwear:

Segment A this segment people belonging to EWS, Lower Class, Lower middle class which are being catered largely by unorganized small players, small scale industries. These people tends not pay more than Rs. 30 to Rs. 80 for footwear/sleeper. The population of this segment is huge, and the SSI also fulfill their demand by provides footwear in the range of Rs. 30 to Rs. 80 and shoes from Rs. 200 to Rs. 500.

Segment-C this belongs to upper middle class, higher class, college-going student, youth workforce of MNCs, Corporate world, PSUs, Business class people etc. in this segment people generally prefers high end branded products like from PUMA, NIKE, ADDIDAS, LEE Cooper etc. These people consider this as status symbol of for show-off whatever may be called, but the mentality is like that only.

Segment B then come segment B, where BATA, RELAXO, KHADIM etc. are playing. People from Middle Class, Upper Middle class etc. moves from non-branded products and prefer branded products at reasonable price range from BATA, RELAXO etc.

So, all the three segments are basically lifestyle of people. And the transition of lifestyle happening continuously from A to B to C. As soon as a person’s life style changed from B to C, she moved to upper level brand.

To my sense the scope of expanding segment B is not huge as people keep moving in the lifestyle chain A-B-C. Although Relaxo and BATA is expanding the capacity but the scope of organic growth is limited, growth can not be achieved through volume expansion only. The company will have to acquire high end brand to cater Segment-C (like BATA acquired Hush Puppies) or they have to lower the price to cater Segment-A.

Different views are welcomed…

2 Likes