The difference in realisation between what Relaxo makes per pair and what Bata makes is 4x. One can’t club them in one segment. Based on your categorisation, I would think Relaxo is in Segment A and now trying to move to Segment B. While Bata is in Segment B and making a pitch for Segment A and C both.

Yes, the main reason is that Relaxo is a market leader in Chappal / Slippers where Bata is no longer present. Average price in this segment is around 200/-.

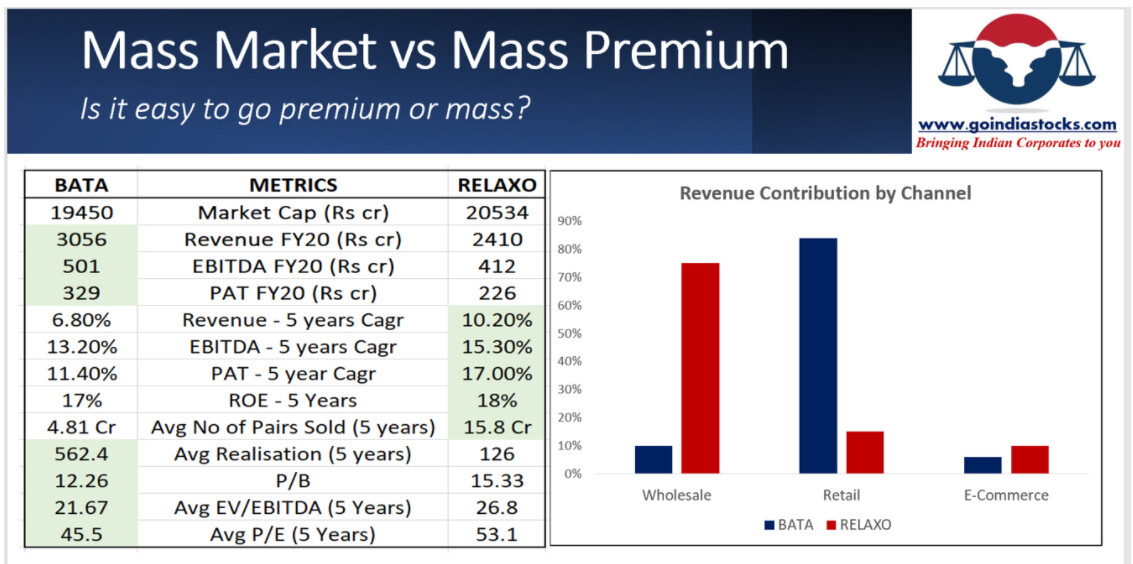

Proper comparison of Relaxo is with Sreeleathers. Bata is a bit premium overall.

Also Relaxo competes heavily against unorganised and unlisted market. For eg) in my city(blr), i have asked several local footwear shops and relaxo is not in demand , instead brands like paragon and other local brands which range from 100 to 500 are more preferred. 90% of them didn’t have any relaxo product.

I have seen Relaxo brands being sold in almost all the dmart stores I visited so far in Bangalore. Relaxo footwear is available in many local shops around HSR layout with Sparx hoardings displayed outside the store

Somehow the links might have broken.

You can scroll down here (http://www.valuepickr.com) , and check out all previous Mgmt Q&As captured by us in earlier years.

Read the interview! Thanks for sharing though its very old one… its very insightful great questions asked by you guys… do you still think or the company still believes that it doesn’t have any pricing power? And the other question you asked was how bata’s business model differs from relaxo… I didn’t get it exactly. can you please elaborate…

You won’t see relaxo just as a company but as a passion on which this huge footwear business is built.

Few things that are good and a few things that are not good in the company(i won’t say bad).

I have accumulated some of the points mentioned here and there to make my thesis.

Hope you gonna like it.

I did a google search “Hawai Chappal manufacturer China”, it took me to Alibaba.

The idea was to can someone simply order huge qty from India / China & come in this business.

My quick 5 min analysis, gave me few insights :

Alibaba has suppliers lowest from Rs 19.15 per piece. (I looked for reliable supplier by clicking on Trade Assurance). I am not regular to Alibaba, here is the link :

So one thing became very clear to me, the entry barrier is very low in this business. The target segment in which Relaxo is price sensitive & if someone with little deep pockets can create a brand & just play on pricing, can give run for money for Relaxo. Mind you the avg revenue per pair for Relaxo is less than Rs 125 which means they get more revenue from Hawai Chappal.

Would like to have thoughts of others as well.

Disc : Invested.

Let me counter the argument of low entry barrier -

Cos with own manufacturing setup, strong brand and pan India distribution will be the toughest to beat in open footwear category. Relaxo checks all three. One can certaily manufacture Hawai chappals and sell it. But getting the scale is the key here to make decent margins and RoCE. And scale is possible only with own manufacutring setup (unless you are likes of Nike). In fact, my channel checks suggest over last one year, co has only but gained market share from the small, unorganised players.

IMO, things are nicely placed for Relaxo going forward. I see Relaxo to evolve more like CROCS in next 10 years, albeit with tad bit lower ASP.

Is Marcellus selling Relaxo? I just saw in a portfolio that they’ve sold the entire stock (in this one portfolio). May just be reallocation towards better ideas (and nothing wrong with the stock per se).

He has sold relaxo, he has a view on succession planning in Relaxo. Not positve as Ramesh Kumar Dua is getting old and he thinks sons would get the top job out of the 5 kids i think.

He is buying TCS instead of that.

Marcellus can’t go wrong for even a minute, thats why he sold pre maturely. I am holding relaxo, i think he has exited pre maturely coz he manages public money so he did well for the fund. No issues in that.

Lowest being Rs 69.5

Lowest being Rs 69.5