A very rosy picture given the boom times (Sales of tech products are at all time high given festive season just ended - Diwali / Christmas) and markets are sky rocketing across the world - allowing people make more impulse and planned purchases (better affordability). In addition, WFH trend is enabling a lot of positivity across the world given no matter what industry, a camera / microphone / laptop / good phone is always needed for ability to work from home or just work remotely - not just from home.

A counter argument to WFH could be, even offices buy equipment, in fact they have more stringent obsoletion policies (renewed laptops once every 4-5 years for modern offices) as compared to individuals (Individuals might go longer with their devices and replace when its really required).

All this said, its very difficult to ascertain from numbers alone the growth path.

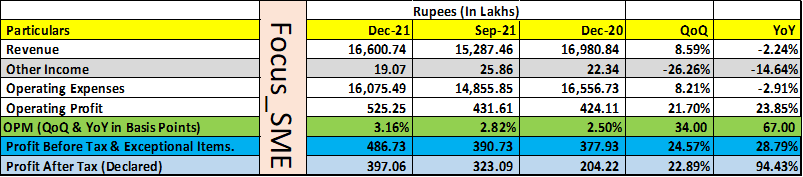

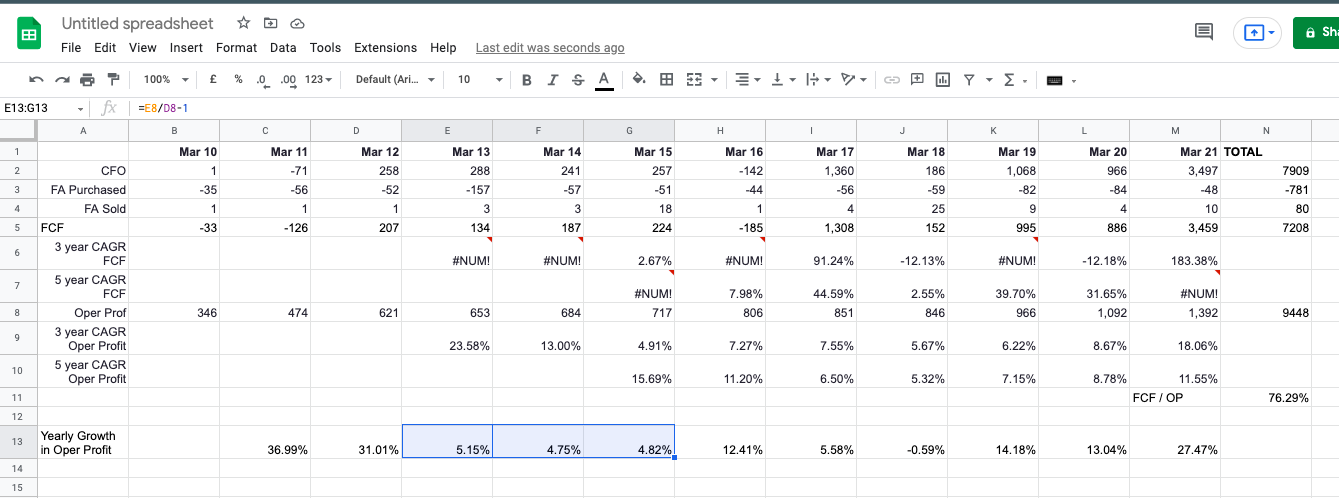

See screenshot (data source: screener.in)

In past 11 years, this business has seen more troughs than peaks.

E.g. Operating Profit growth during years ending Mar 13 - Mar 15 and then during years ending Mar 17 and Mar 18.

From limited analysis of numbers, I reckon all in all this is a cyclical business. There are downs when companies and individuals do not spend much on IT equipment and then there are times when obsoletion comes in picture, there’s too much money in the ecosystem, consumerism takes its heights and companies are on capex cycles.

If anything, I would want to buy this business for the long haul (say 15-20 years) assuming direct distribution (non online) is not going anywhere at least for the next couple of decades, but I would want to buy it during the bust cycles, when Mr. Market really punishes the valuations due to a trough in expense cycle of individuals / companies.

As for valuations:

- With current numbers in mind Positive FCF of 296 Crores for 9MFY22, simple extrapolation to ~400 Crores of annual FCF, at market cap of 12717 Crores, this business is yielding 3.14% annually in cash.

- One could get more than ~5% in annualised yield from Fixed Deposits. Considering 10 year GSEC rate of 6.8% as of 9 Feb 2022, the Free Cash yield at which this business is available is not at all appealing.

With good times (high sales, too much positivity) if the cash generation is not so exciting, I don’t think this is a candidate for re-rating (Reserve my right to be wrong).

Lastly, this is not my holding, I have been tracking developments for a while as I came across Redington when I purchased by Asus Router and have been seeing their sales/customer care office in my hometown with too many cartons of products always lying on the outside.