inventory & receivables account for 90% of redington’s assets. Working capital will always be a major drag on its cash flows because of the kind of business its in. They will never have sufficient excess cash profit for any kind of growth. Its kind of stuck in a weird spiral. Apple is its major supplier , and as apple grows redington will have no other choice but to grow or lose the apple business. But if it grows then it will lose more cash than before. This kind of forced growth over which you have no control is very harmful for the company. Look at its working capital growth . WC has compounded at 17.28% over the last 10 yrs while sales has compounded at 13.18%. Imagine a situation where you have truckloads of inventory at your warehouse ( Inventory) or truckloads of inventory at your customers warehouse ( receivables ) and that inventory has to move out mega-fast before it becomes obsolete AND that is 90% of what you do - distribute gadgets before they lose their value. 90% of your business is permanently at risk at all times. that not good for your sleep. I would avoid redington. I dont like its business model, its too risky

What you have said ia completely true. But despite this the company has managed to grow. There are only few companies in this field due to your mentioned hardships.

This also acts as a barrier to entry. Now I am not saying that this company will be a multibagger but It has strong operation skills and the growth in revenue will come from servicing and logistics.

Disc: invested a small amount for opportunistic play on Gst, apple and pixel distribution and also it’s logistics and servicing division.

A investor’s delight should not be only a growing company but a growing company which can generate good incremental cash on per Rs investment at appropriate valuation. Personally, am sure that there are much better business models available

To cut a long story short, Apple has Redington by its b***s. Its painful for redington but to avoid further pain, redington will do what apple & others tell it to do even if it is harmful to the company & its investors. Yes its certainly a barrier to entry but its not a barrier that redington would ideally want. Its stuck in a bad marriage.

-

Can anyone help in clarifying the business model of a distribution business?

-

In Redington’s case, why is it so capital-intensive and with such a low OPM?

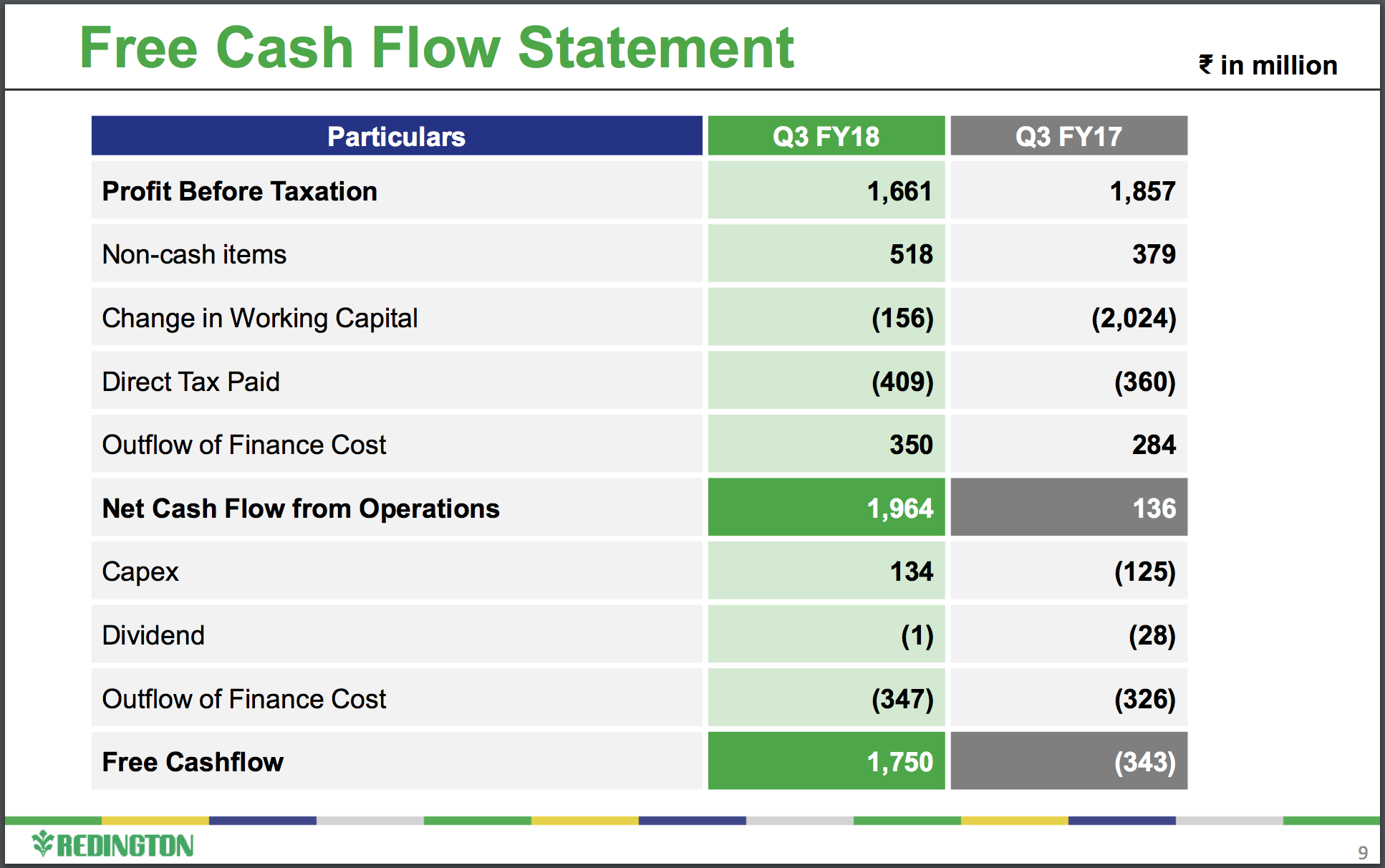

Hi @bheeshma , what are your thoughts on Redington India now after this quarter where they had positive free cash flow.

Also, now with logistics getting infrastructure status, their warehousing and logistics arm will also benefit to some extent.

Source: https://www.bseindia.com/xml-data/corpfiling/AttachHis/2dea2207-9195-407e-8bcf-fea4fb1a0ecf.pdf

Disclosure: Taken a small position.

Hi @uab59,

I am not tracking the company. A couple of investors i know seem to be positive about the prospects though. However, since its into a low margin trading business , the PE seems to be what it should be.

Best

Bheeshma

I am trying to study Redington fundamentals. Can anyone help what products they are marketing and any recent change in their business model.

Any inputs will be appreciated.

Hiii, i was checking this stock on money control and promoter holding is 0%.

Has anyone checked that

Its discussed here - its being run a professional board.

Noticed that this page is been quiet for more than two years now and thought this deserve a lot more attention considering the company seems to have reported its best ever quarter in terms of profits and balance sheet quality at a consolidated level for the quarter ended 30th September 2020.

If you have never/ not been looking at this company here is the latest investor presentation which gives most of the information you will need to get a fair understanding of what they do and how they have been performing over the years.

Just to give some highlights:

-

The company is almost fully owned by large institutional investors (with >75% of them being FPI’s and large foreign investors).

-

The company has seen dramatic improvement in balance sheet quality over the last two quarters. While I do not want to thank Covid for any reason - the disruption has really helped this company to get its balance sheet quality back to absolute pink of health - just to put things in context, back in March 2020 the company at a consolidated level reported a debt balance of 2500 Crore and a cash balance of about 2350 Crore, and few days back it reported a debt balance of 827 Crore and a cash balance of nearly 3100 Crore as at the quarter ended 30th September 2020 - this is achieved primarily by improving its AR significantly and maintaining its payables at about the same level. The disruption seems to have helped them to command better credit terms from the channel partners while retaining the existing terms with the vendors(OEM’s). Additionally the quarterly finance cost has dipped from 30 Crore per quarter last September to a meager 10 Crore now. For a company which is into large scale IT equipment distribution business working with laser thin margins, the kind of impetus this has given to its P&L and the flexibility and robustness to its balance sheet is absolutely unprecedented.

-

I believe scale the company has already achieved will make it prohibitive for new players to enter this market(while its absolutely possible for the larger players like Ingram Micro to challenge them significantly in all the geographies they operate).

-

They have a real high quality management team and a board represented by almost all large share holders. I believe the board is clearly focused on share holder returns, which is evident from the emphasis given on return ratios and peer group comparison given in investor presentation and this will help the large and small share holders alike. Additionally the company is a consistent dividend payer and taken all measures to alleviate investor concerns when ever such situations have arisen in the past(read 5 below for more on this).

-

They way they have come out of the crisis they faced in Turkey(on account of Lira devaluation a few years back) is a clear testimony on the problem solving ability of the management and its board.

-

With the the balance sheet flexibility they enjoy, they can continue to deploy money into value accretive acquisitions and grow the top line and geographical presence.

I believe the company has all the ingredients to grow and prosper both in India and internationally and they could well be entering into its best years in terms of growth opportunities and investor attention.

A word of caution: Note that the geo political issues, global trade and currency fluctuations can significantly impact the performance of the company - read about what they faced in Turkey a few years back due to Lira’s devaluation and additionally a wrong acquisition can cost them dearly.

Disclaimer: A long term share holder and my views are biased.

AJ

As expected the growth story is continuing with the added bonus to shareholders by way of Rs.11.6 as dividend for the full year.

See the Q4 presentation here.

Edit: Market has given a thumps up via an upper circuit. Kudos to the management team for putting its act together and delivering efficient performance quarter after quarter(now 3 quarters in a row).

AJ

Disclosure: Invested from lower levels and added recently.

Stupendous performance. its a cash generating machine.

Redington announces 50% increase in PAT and 60% increase in EPS QoQ !

Compared to Q4FY20, their revenues have increased 15% and PAT has increased 85% !

Compared to full fiscal FY20, their Revenues are up by 11% and PAT 47 % !

Also in FY21 their total Free cash flow is Rs. 3360 cr and their OCF has tripled from last fiscal !!

Discl: Invested

What are the reasons for such a sharp rise in profitability?? Is it sustainable? Is it that with everyone working from home the off-take of laptops and other products was high. This may not continue??

Looking at the screener data, debt has come down substantially which has resulted in 46% less interest outgo compared to last year.

Came across a very well put together research work on Redington. Read it here.

Note to moderators and fellow valuepickr’s: Not sure if what I have shared is against the valuepick’s data sharing policy. Please flag this post if it is against the forum rules.

AJ

Disclosure: Invested.

Yeah 5% div yield is not bad. 33% of Mcap in cash and reserves, and a trailing PE of 13x makes me wonder why this stock cannot be a multibagger?

Nice blog. Looking at the global peers’ valuations Redington does not seem to be as undervalued as it was before 2 back to back upper circuits. The NPM in recent past was in the range of 1-1.1% as mentioned in the blog and has now improved to 1.4-1.5% range if we add one off 89cr settlement. The improvement in margin seems to be because of debt repayment.

If we take 10% growth then they hit 62k Cr revenues next year. At 1.5% NPM it will generate close to 930 Cr profits. At 15x it will trade at around 14k Crs (The global peers mentioned in the blog trade between 10-15x). At 10x it is fairly valued. It is difficult to come to a strong conclusion because with such high revenues and 0.1% margin here and there or 15% top line growth instead of 10% can change the calculations.

The good things going for the company are:

- Good OCF this year. More than 3x compared to last year.

- Reducing debt. I don’t know if it can be reduced further or if there will be substantial margin improvement going forward based on debt reduction alone.

- With WFH sales of electronic gadgets increasing. But how long this trend of WFH can go on?

- There growth in mobility and service is strong (~20% CAGR). If these can take higher share of revenues, the top line growth can improve.

Concerns:

- More competition and that will affect the already thin margins.

- Threat from e-commerce players.

Disc: Invested. I am not a SEBI register advisor. The above note is not an investment advice but an educational post to discuss a business model.