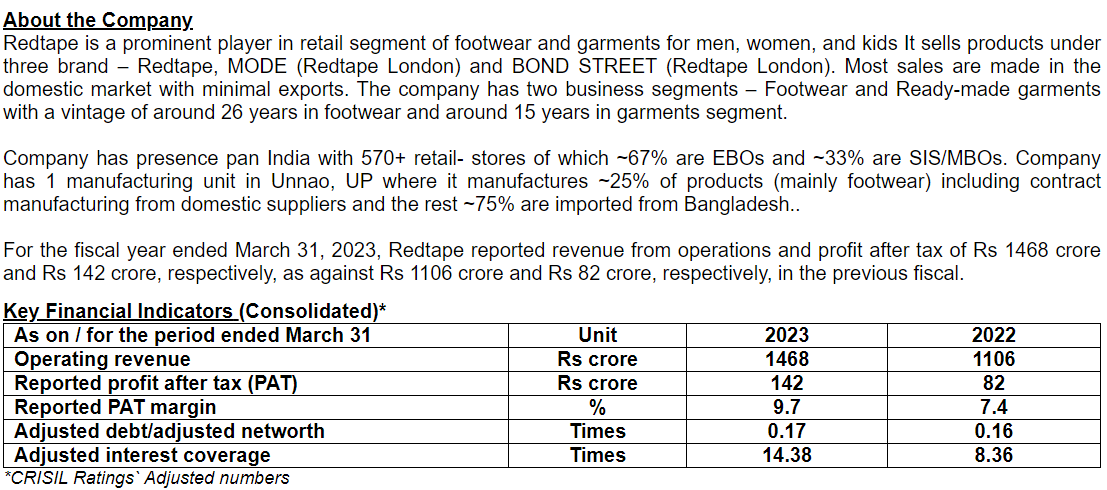

India’s trusted leading Fashion and lifestyle brand with over 390+ opulent stores across PAN India. RedTape is known for emerging as one of the Finest Brands of Footwear and Clothing for Men, Women, and Kids. It has become a complete Family Fashion Destination by providing the Best International Styles and World-Class Quality through Shoes, Apparel, and Accessories for all age groups.

The company sells in over 37 Countries and 6 Continents. It is listed among the top Footwear Brands striding ahead of the market. The brand has gained a strong foothold in the niche markets of India, the UK, the US, Australia, Turkey, UAE, France, Germany, West Asia South Africa, and others.

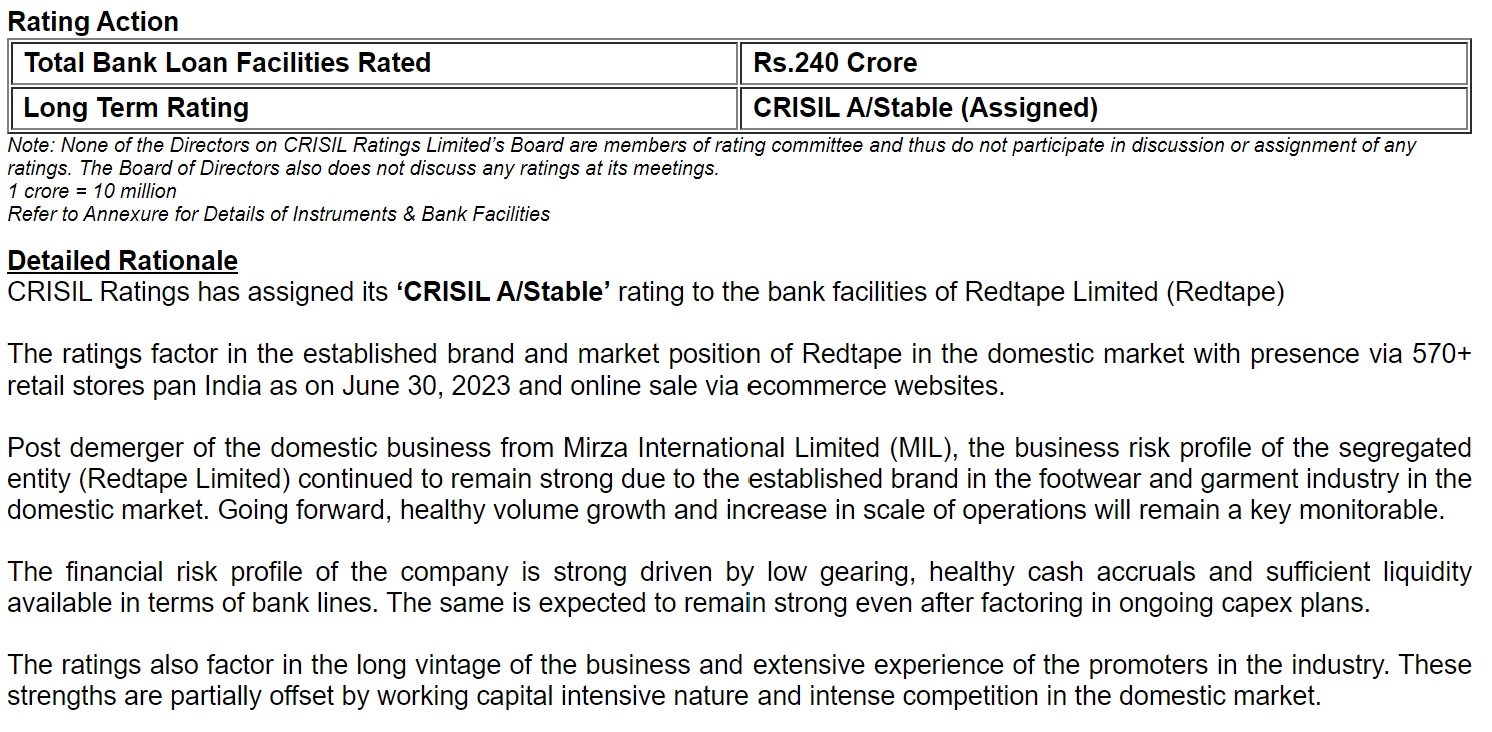

It was demerged from Mirza International in 2023.

| Narration | Jan-00 | Jan-00 | Jan-00 | Jan-00 | Jan-00 | Jan-00 | Jan-00 | Jan-00 | Mar-22 | Mar-23 | Trailing | Best Case | Worst Case |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

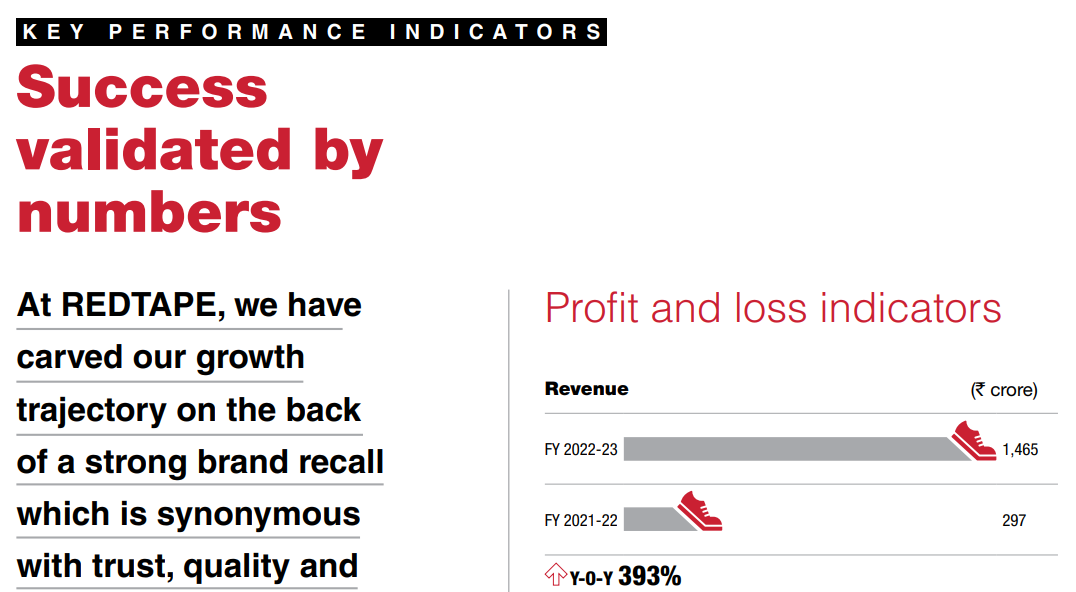

| Sales | - | - | - | - | - | - | - | - | 303.22 | 1,468.31 | 1,078.16 | 7,110.13 | 5,611.02 |

| Expenses | - | - | - | - | - | - | - | - | 255.75 | 1,223.96 | 884.63 | 5,833.86 | 4,686.73 |

| Operating Profit | - | - | - | - | - | - | - | - | 47.47 | 244.35 | 193.53 | 1,276.27 | 924.29 |

| Other Income | - | - | - | - | - | - | - | - | -0.25 | 6.65 | 4.75 | - | - |

| Depreciation | - | - | - | - | - | - | - | - | 2.43 | 44.44 | 36.56 | 36.56 | 36.56 |

| Interest | - | - | - | - | - | - | - | - | 3.99 | 17.46 | 15.01 | 15.01 | 15.01 |

| Profit before tax | - | - | - | - | - | - | - | - | 40.80 | 189.10 | 146.71 | 1,224.70 | 872.72 |

| Tax | - | - | - | - | - | - | - | - | 11.76 | 46.95 | 37.36 | 25% | 25% |

| Net profit | - | - | - | - | - | - | - | - | 29.04 | 142.15 | 109.36 | 912.83 | 650.48 |

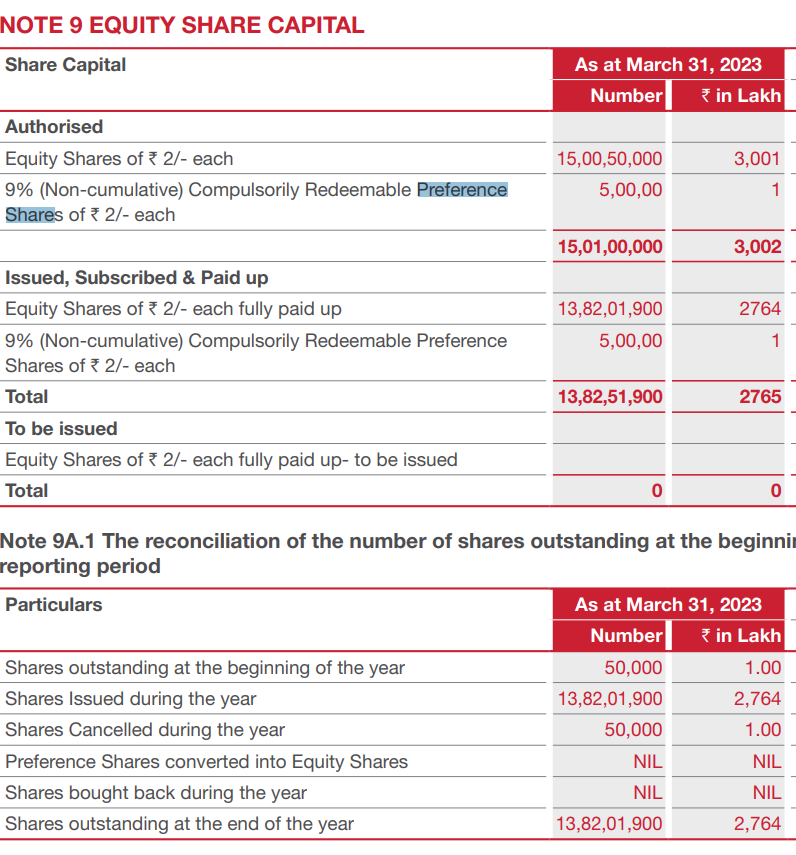

| EPS | - | - | - | - | - | - | - | - | 5,808.00 | 10.29 | 7.91 | 66.05 | 47.07 |

| Price to earning | 52.95 | 52.95 | 52.95 | ||||||||||

| Price | - | - | - | - | - | - | - | - | - | - | 419.00 | 3,497.39 | 2,492.24 |

| RATIOS: | |||||||||||||

| Dividend Payout | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | |||

| OPM | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | 15.66% | 16.64% | 17.95% | ||

| TRENDS: | 10 YEARS | 7 YEARS | 5 YEARS | 3 YEARS | RECENT | BEST | WORST | ||||||

| Sales Growth | 384.24% | 384.24% | 384.24% | ||||||||||

| OPM | 16.47% | 16.47% | 16.47% | 16.47% | 17.95% | 17.95% | 16.47% | ||||||

| Price to Earning | 52.95 | 52.95 | 52.95 | 52.95 | 52.95 | 52.95 | 52.95 | ||||||

| Source - Screener |

Risks/threats -

Economic and political factors, both national and global, that are beyond control, and factors of force majeure, may directly affect the performance of the Company as well as the Footwear industry. These factors include interest rates and their impact on the availability of retail space, rate of economic growth, fiscal and monetary policies of governments, inflation, deflation, consumer credit availability, consumer debt levels, tax rates and policies, unemployment trends, terrorist threats and activities, worldwide military and domestic disturbances and conflicts, pandemics, and other

matters that influence consumer confidence and spending.

Disclosure - Invested