Of all the REITs - Brookfield would struggle the most to lease space as weaker micro markets. Embassy has the best located assets - Bangalore ORR.

Embassy if it comes down to ~Rs.300 would be a good buy.

Blackstone sold to Funds

Does anyone know how/where to put REIT payout details in ITR2? I know what is taxable and what is exempt and I know my figures too. I just need help in putting them in the right places in ITR2. I am ready to pay you or any charity on your behalf for this knowledge. Please let me know…

I don’t know about forever but this could very well be true for next 5-10 years which would definitely slow the growth for commercial office REITs

Physical office is still a need. Will the lease terms change if workers are expected to come to office only for three days instead of five days?

Completely agreed with the logic here but we as REIT investors are not investing for future growth right-infact we will be happy to have 90% occupancy for the next many years and no growth required for that.

Plus India has a huge infra deficit and so this applies a lot less to Indian context I feel.

Views invited.

Heavily Invested

yes, now u would need a smaller office

We need to consider the fact that the occupiers/tenants have spent anywhere between Rs. 2000-4000/square foot on interiors and have themselves invested in these offices. Even though a significant proportion of employees don’t want to return to office, companies may be finding it difficult to give up office space because they’ve invested so heavily at the start of the lease term. I think several occupiers will consider taking the loss and vacating space if offices run at these low occupancy levels for much longer. Ultimately if staff come in only 2-3 times a week it will be a negative for commercial real estate IMO.

yes, your point is valid but as you would appreciate - most of the interiors have a shelf life of 7 to 10 years. So if you have already completed this time period - u may as well go to a smaller place and save on rent. Even if you have not completed this time period - but are saving on rental - u may take a call by doing analysis.

Obviously these questions are never easy and would also depend on the growth plans etc… so all these changes would occur over the medium to long run and won’t have an immediate impact.

My take is long run - office would be more of a mature asset and the growth rates we saw earlier would taper down. Demand won’t totally collapse but the growth rates in mature micro markets won’t be as high as earlier. With vacancy being on a decadal high and supply which was already under construction to come up with a lag I feel vacancy in short to medium term to remain high (we have ability to absorb two years of demand and with fresh supply u would continue to have similar vacancy numbers)

It’s better to look at the numbers of all the listed REITs. They all working on expansion and they are increasing the lease area.

India is one of the cheapest in terms of commercial real estate market and it will grow as more companies shift their base to India. Yes, I do agree that the many companies will have option of working for only 2-3 days per week from office but this will be compensated with increase in employees + many MNC shifting their offices to India.

Hi,

Anyone tracking Nexus Malls Retail REIT. Any idea when is it likely to get listed?

likely to be launched in the first half of 2023

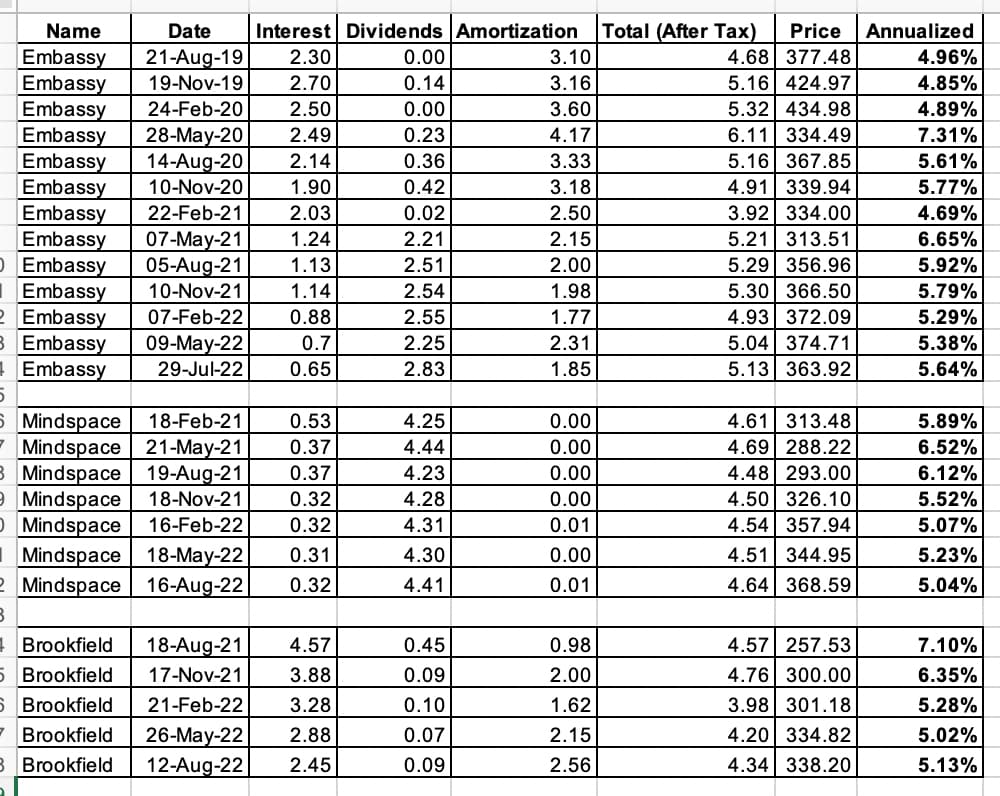

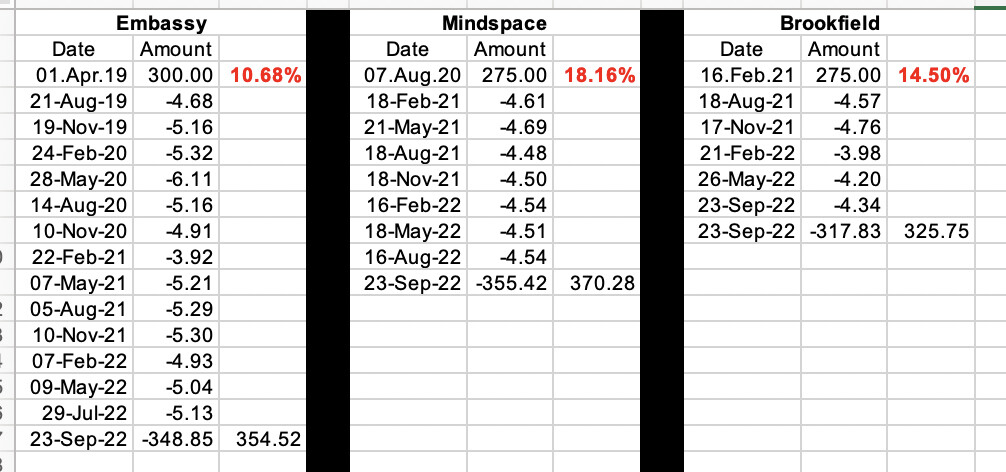

XIRR for someone if they have bought during IPO and held it till now… These are POST taxes (30% slab)

They should not be compared with each other since the time frames are different

Good one…pl share the Excel too, if possible. That will help us keep track since prices are dynamic …for example, after the recent fall in Embassy, we are closer to 6% mark now perhaps, assuming same distribution continues

This may have been answered earlier, but unable to get full clarity on below points about REIT distribution:

- Dividend component is well understood: Rental income after expenses

- Interest component: How is REIT able to generate Interest income? In fact they should have interest expenses for the loan they take for new constructions

- Return of capital: On one side REIT is taking loan or issuing new shares for new construction, and on the other side they are returning capital to existing shareholders. This is not adding up. Is this just to keep DPU (Distribution Per Unit) artificially high? If yes, then we should remove this component from our yield calculation as they are returning our own money by raising capital somewhere else.

Can someone throw light on #2 and #3.

Thanks!

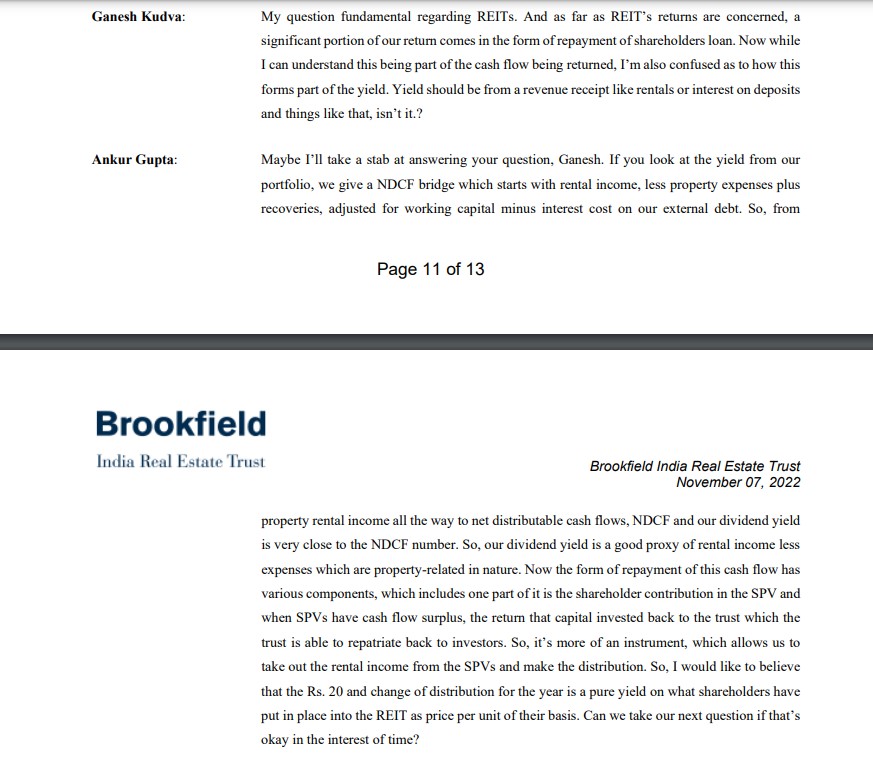

A similar doubt regarding interest component was asked in the Brookfield con-call also. REIT’s generally hold the properties into SPV (Special Purpose Vehicle). This is done to transfer the property easily by selling the SPV and just paying capital gain taxes and to reduce and isolate risks from the holding co. Now when these SPV receives rent, and have surplus cash they are transferred back to the REIT in the form of interest and repayment of shareholder loan. This is mere an accounting practice.

Regarding your other doubt about return on capital, REIT’s have to mandatorily distribute 90% of the collection to unitholders. So they have very less cash balance left to grow the assets and hence the increase the GAV, NOI and hence the distribution to the unitholders. Hence the fund manager has 2 options-

- Keep distributing full amount of collection to the unitholders and don’t take any debt. In this case the NOI would only grow at the pace of rent escalations as the growth in the total area would be very slow (as only 10% of cash would be left).

- In the second option the fund manager would use the property they already have, and by pledging them will raise debt and then use these funds to buy or construct new properties. This would lead to faster growth in the total area.

Therefore trust managers by using the same assets they have, are able to generate better returns for the trust holders by taking debt. The principal amount of these debts are generally paid back by raising further debt at the time of maturity and the interest gets paid back from the cash flow generated by rents.

In some cases at the time of acquiring new properties the REIT issues a combination of equity and raises debt to fund the asset. Even in such cases it is done in such a way that it is DPU accretive for the unitholders.

I hope this solves your doubts.

" Yields generated on three listed REITs have fallen below their listing yields, and these now return even less than benchmark bonds, data compiled by ET until January 10 showed.

Blackstone-backed Embassy REIT, for example, is yielding 6.4%, down from the 8.2% it yielded at the time of its listing in March 2019. Raheja-backed Mindspace REIT is yielding 5.7%, lower than the 7.30% it yielded when it listed in August 2020, while Brookfield REIT is yielding 7%, lower than the 7.9% it yielded in February 2021. Moreover, yields are even lower than the 7.30% offered by the 10-year government securities."

Source: