The right way to do such a comparison is post-tax comparison, wherein REITs will continue to score. I did not understand, just matching pretax yield vs G Sec. I am sure that most in this forum are in top tax bracket plus surcharges even

6 Likes

There is no comparison of REITs vs bonds. REIT asset value & yield both increases with time which is not the case in bonds.

With increase in rates, reit yield in pressure but it may be compensated by asset value increase due to Inflation.

NAV of REITs today are higher than the listing NAVs. But perception changes with price.

4 Likes

Find below the article:

Looks like there maybe some relief

https://economictimes.indiatimes.com/news/economy/policy/gst-tribunal-invits-among-likely-60-changes-to-finance-bill/articleshow/98951210.cms

Please share your views on Nexus Select Trust sets price band for India’s first pure-play retail mall REIT IPO at Rs 95-100 per share

Nexus Select Trust REIT DRHP

the price band seems reasonable given the assets and the marque clients like Apple stores

Blockquote

Nexus Select Trust boasts of 17 malls located across 14 cities, including Delhi (Select Citywalk), Navi Mumbai (Nexus Seawoods), Bengaluru (Nexus Koramangala), Chandigarh (Nexus Elante), Ahmedabad (Nexus Ahmedabad One) among others. According to the RHP, the trust’s portfolio constituted 30% of India’s total discretionary retail spending in FY20 and had an average population CAGR that was 226 bps higher than the national average from financial years 2011 to 2021. In addition to the malls, the trust also comprises three offices and two hotels. One of the trust’s properties, Select Citywalk, was in the limelight recently for housing one of India’s two exclusive Apple stores.

2 Likes

Hi Aveek thanks for sharing : My limited view as of now. Key factors to consider would be

- Where does Nexus REIT sit in the overall REIT/INVIT portfolio of individual investors (this will depend on where all one has invested)

- What distribution yield is on offer + potential growth in distribution (pre and post tax)

- Diversification from office space as all other REITs are office focussed

- Threat of online shopping. Do higher footfalls translate to higher store revenues and hence higher rentals

- Future asset development plans

Still on wait and watch on this, however will most likely take a position

3 Likes

Here are links to various interviews on Nexus IPO. What I gleaned out of this is that the yield is about 8.25% pre tax, and 7.1% post tax (doing the math, looks like it is for 30% tax bracket with no surcharge)

(timeline - 3.4)

(timeline - 8.1)

4 Likes

I wonder if Shopping Malls are really generating good business in India.

Unlike in the developed countries, malls here are restricted to luxury brands. A common Indian shopper intuitively knows that any product from a mall will be super expensive, and goes to malls to watch movies or to hang out occasionally than to do any real shopping.

3 Likes

Unlike in the developed countries, malls here are restricted to luxury brands.

Yes. This aspect has the advantage of making malls aspirational, rather than utilitarian.

2 Likes

Given the footfall and the aspirational middleclass hanging out there, and given our ever expanding population in cities, this may not be such a disadvantage.

The one factor I was keen to find is how much of funding is required to renovate. Malls get a tired look in a few years and there is always the craze for something new !! New malls with attractive interiors, gizmos crop in all the time and except the location advantage, older malls lose out. Cities are also expanding vastly and what is the outskirt today is, heart of city tomorrow !

6 Likes

Hi Steel, thanks for reply … yes i agree with your points … i am also in the wait a watch camp and will let the IPO euphoria settle before taking a position.

2 Likes

As of day 2 end, Nexus IPO is fully subscribed in non-institutional category (note- there are only 2 categories in these kind of IPOs,insti and non-insti)…overall subscription stands at 57% at the end of day 2.

Full allotment in non-insti category is ruled out, given the over subscription.

PS - Grey market premium is Rs 5 only. But, if there is one lesson from Mankind pharma ipo, subscription % can’t be equated to listing gains. That said, this is a different kind of instrument (REIT vs equity) and no point comparing. A pop in listing is unexpected in these instruments, unless one gets into a phase of Euphoric Embassy type of post listing phase. The yields and the comparison with GSec won’t justify that

4 Likes

yup … i am not an IPO guy … i prefer to wait and let the price discovery happen for few quarters then decide

1 Like

There is the TINA (there is no alternative ) factor. There is lack of alternative debt instruments (forget the yield comparison but look at the lock in etc) in the market and hence large family accounts, are pouring in the money into Nexus IPO

Disc - I have applied for the IPO

2 Likes

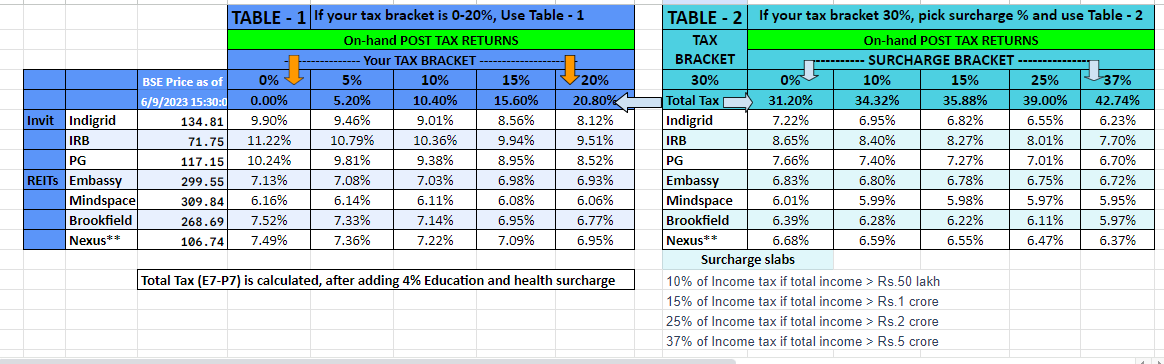

Wanted to give a comparative view of yields across listed REITs and Invits, on the prices as of 9th June 2023 (earlier I had shared it on 2nd June. There was a minor error in DPU of PG and I fixed it…won’t change anything drastically and it is a 2nd decimal correction) , and this is based on the rolling 4 quarters DPUs…Obviously, yield will differ for your tax bracket and hence pick the right slab below…

REMEMBER that these are POST TAX, ON HAND Yields for the Invits/Reits, for the price shown. **Nexus yield is based on projections gleaned out from various interviews, during IPO.

PS - Questions/Feedback, welcome

13 Likes