Embassy : cost of debt 6.9% ; leverage 22% of market value of portfolio ; committed occupancy 88.9% ; collection 99% ; distribution for the quater 5.6₹ ( 78% tax free )

Mindspace : cost of debt 7.1% ; leverage 14% of market value of portfolio ; Same-store Occupancy : 86.8% ; committed occupancy 84.2% ; collection 99% ; distribution for the quater 4.81₹ ( 92.3% tax free )

Brookfield : cost of debt 7.15% ; leverage 18% of market value of portfolio ; commited Occupancy : 87% ,same store occupancy 91% ; collection 99% ; distribution expectation till 30 sep’21 from date of listing i.e.16th feb : 12.75₹ ( 30% tax free )

*Same-store Occupancy excludes areas developed during the year

Stable results from BIRET. Based on the NDCF projection shared this seems to have the highest post tax yield amongst the 3 REITs.

Given Brookfield has put it own brand on the REIT (unlike the foreign partners in the other 2), the good properties held by the REIT and their stated effort to increase the tax free distribution this appears to be very lucrative.

Market isn’t impressed though and I wanted to understand that? Any views?

Is the NDCF projection too ambitious or the lack of properties in Hyderabad and Bangalore hurting them.

I understand the yield projection is for a period of 8 months from IPO till Sep 30, 2021 and not 6 months.

There were many questions around this as well on the concall and one specific one which asked the management what was the yield accretion upto 31 March, 2021 out of the total 12.75. Management didn’t provide any exact figure on this and also didn’t deny that the entire 12.75 is from April 1 onwards.

For some reason I was not given the opportunity to ask questions on the concall, had the following observations which I wanted to clarify from the management. Anyway have mailed the questions to them now.

Post IPO presentation on 19 March 2021 - NOI predicted to be was ~7 billion and actual achieved is 6.5 billion, a miss of 50 crores within 15 days of the update. What’s the reason for this?. If it is CAM revenue / profit, wouldn’t the management have already known it by 19 March 2021, then why did they put 700 cr NOI?

In terms of growth, talking about Identified assets Gurgaon G1 and Noida N2 - I did the calculations of Operating Area 7.3 msqf at a occupancy level of 90% with the respective in-place rents 70 and 51 psqf, it works out to roughly 500 crores of NOI operating income. The combined floor asset value is 8600 cr which is barely 5.8-6% NOI yield, it does not appear to be DPU accretive.

On NDCF, what is the definition of IPO? Please provide the date.

For point 2 mayne you didnt add the CAM revenue to the NOI?

I completely missed the NDCF being for 8 months. That makes more mathematical sense now.

If it is indeed for 8 months then seems to be fully priced at this point.

Came across a good article on Global Commercial Real estate market in latest issue of The Economist. Find enclosed link for same.

The article does cover like negative impact on Covid over relatively long term and also about likely lower office demand for office space in US and other developed countries. It also specify increased amenities and green building as key for success for new Real estate developer. Just thought this might be useful for the forum.

In same issue, another article mention very critical point about linkage between vacancy and Commercial real estate price.

The IMF reckons a rise in vacancy rates of five percentage points in all commercial property would cause valuations to fall by 15% over five years.

Great news for REITs and investors, allows so much more flexibility when investing in REITs. Also opens up the possibility of being included in certain indices going forward.

Mindpspace in Hyderabad will be opening soon could be in Sep 2021. IT Minister have official announcement can google it as Cab drivers , Canteen and local spending have to improve.

From article:

“We have been getting requests from certain accounts to allow their team members to work from Infosys campuses. In addition, some of our employees have also been asking to come back and start working from office, as a personal preference.”

After reporting results last week, Infosys executives told analysts that roughly 99% of its staff was working from home, and the company would make efforts to get “more and more people to come to office” over the next couple of quarters

This doesn’t mean WFH isn’t sustainable. WF(Native) probably isn’t for a lot of people.

People may need to rent in cities, get an inverter if needed and that’s it; WFH is now sustainable.

People don’t need to rent close to office at high rental, and commute expenses will be significantly reduced. WFH is cheaper for both employers and employees.

Hybrid model is a reality and will not have any impact on currently listed REIT. New demand for commercial space may get be slow but similarly new investment and construction activities will be slow. A Grade commercial space will always remain and REIT trading at discounts to NAV give a good opportunity for accumulation for very long term investors. Tax free dividends are adding further incentive to high tax bracket investors. Annual rent increments provide organic growth o Reit as compared to power sector Invit and for above reasons I am shifting my debt portfolio to listed Reits.

Agree, hybrid models if reality or not, may not have much effect on long term on REITs…demand and supply will adjust eventually and so would acquisition costs and entire ecosystem around it…for any good business, the transformation with economics and enviornment is key to sustainability. If we trust, Embassy/mindspace etc are good businesses, we must trust they would evolve to maybe new areas, adjust to new economics maintaining the long term growth & hence payouts…

Disc: Not Invested in REITs, periodically track as have interest and may invest in future

In my opinion, current NDCF in all three Reits are getting benefitted by reduction in costs due to refinancing of debt at lower rates. In case rates start increasing, NDCF may remain unaltered and only impact on New Assets being accrued. Managements have to consider the New asset attractiveness based on prevalent interest rates. Some impact on the Market demand of Reit units can be there but I expect the same to get aligned with NAV in the long term.

Also, rise in interest rate may be there for coming 1-2 year and should stabilize or fall as per economy growth.

I am not a Financial expert and sharing above info based on my past experience and knowledge only.

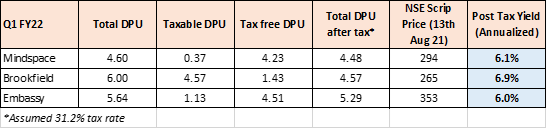

I think doing a like-for-like comparison considering the tax element it seems that all of them fall in a 6-7% range (below is what I created for all 3 REITs). Although I do agree that Brookfield seems to be slightly better basis the current price.

Thanks Ajay. Had a look at the investor docs again and this is indeed for 8 Feb to 31 Jun. Agree with you that brookfield is not comparable with the other 2 and the 6.9% in the above table is incorrect. Thank you.