Wanted to ask if anyone has any document etc which can help me understand how Interest payments by REITs later change to dividend payments like what will happen for Embassy REIT.

Also has Brookfield REIT guided in regards to interest payments reducing and being replaced by Dividend payments which are more tax effective?

Hello Sahil,

Just wanted to know if you would be interested in Brookfield REIT based on the increasing discount to NAV. Also, Brookfield does not seem to have the conflict of interest problem in Embassy (am I right on this). Also, your reasons for not diversifying between different REITs (something the PPFAS video also advised for).

Thanks

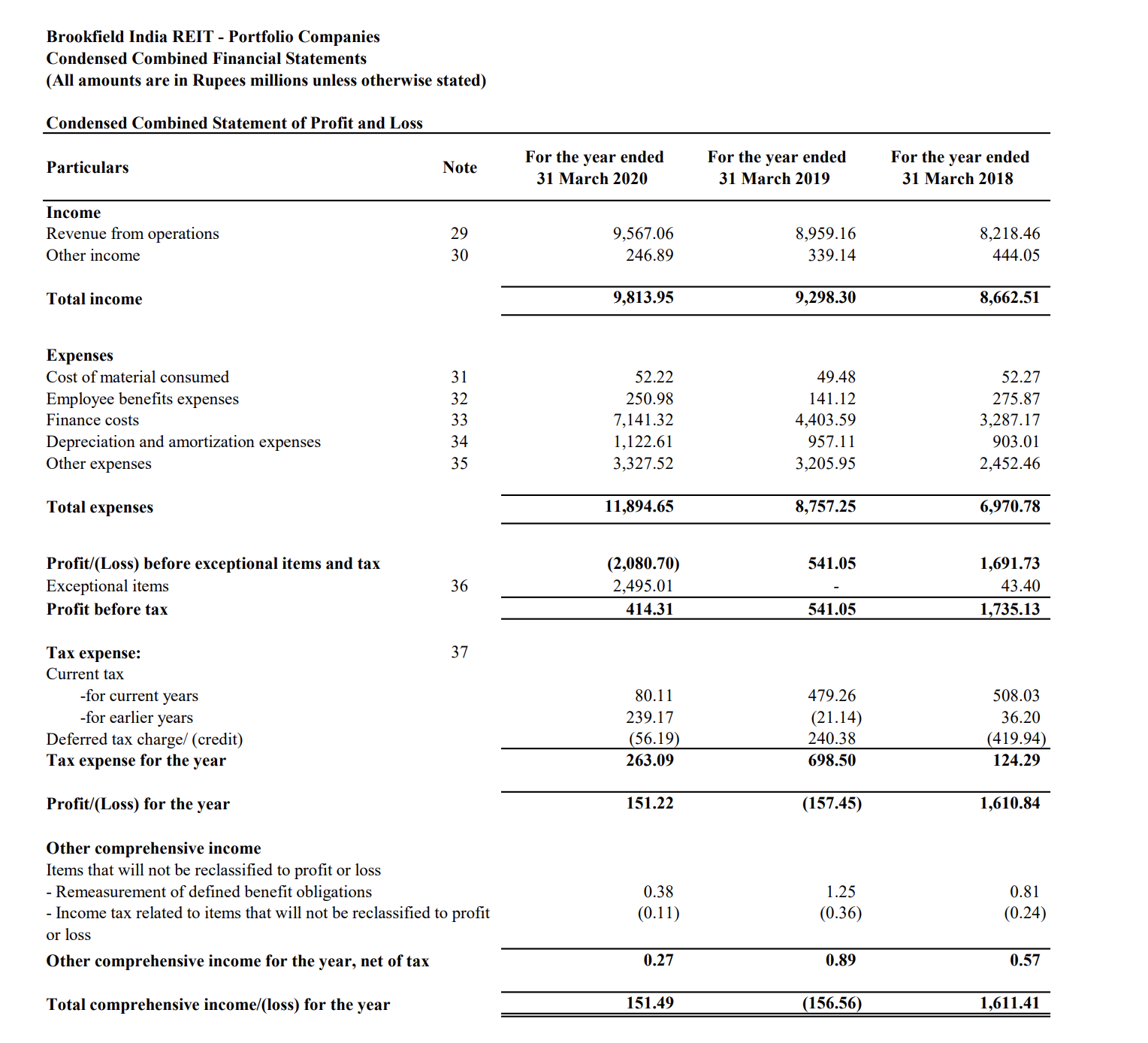

They made a loss in FY20. Why would i be interested in investing in a loss making REIT? The aim is capital protection. Look at the trajectory of the finance costs.

No. The way conflict of interest works for REITs is very different.

As i have highlighted in past on this thread, the sponsor does not get to vote on important deals involving the sponsor.

REIT structure actually benefits from having a pipeline of good quality commercial real estate projects. Otherwise how do they expand the asset base?

Where is the room for mismanagement? if the acquisitions done are at a very high price and hence not distribution per unit accretive, then all the institutional ownership would realize this quickly and dump the REIT. 90% of cashflows have to be distributed to unit holders and hence capital allocation is also not much of a problem.

If related party transactions are a concern, one should stop owning HDFC bank and HDFC RPT by themselves are neither good nor bad. One has to examine each such instance case-by-case. in Embassy’s case, all such acquisitions have been great. (My partner works at ETV which was recently acquired by embassy REIT and it is a great office space in bangalore. Have visited it personally many times).

I dont find any of the other REITs to be as attractive of an investment as Embassy. If i feel that they are attractive, then I would diversify there. Another thing to keep in mind is as per charlie munger diversification is the friend of the uninformed and an enemy of the well informed. Please see this video to know Charlie’s thoughts on diversification:

Brookfield REIT was in losses, but assuming IPO proceeds are used for clearing the debt, then it should be back in profit with positive cash flow for distribution?

losses are of no concern as REIT invests Debt as loan into SPVs… thing to see is the EBITDA and external Debt EMI… post that u need to take 10-15% as leakage due to taxation on EBITDA and you would have distribution …

What seems to be the reason for continuous in Brookfield REIT’s price. All this information was known at the time of IPO as well. Or is it just people getting out after the ipo not getting any listing premium

Spot on !..the above discussions miss the most important point. Brookfield has a short term issue of Haryana reservation BILL…which was a surprise and not declared yet during IPO. This should be stayed by court/rules made to exempt lot of IT companies or ruled illegal by SC ( follow Maratha case ). For the record pre tax Embassy and Mindspace are 40-50% more expensive

So 75% reservation for Haryana domicile means that the IT cos will have to replace every person leaving / new hire with a Haryana domicile person which is HR restrictive and some companies are clearly having reservations of continuity in Haryana plans …and BIRET is 44% Haryana weighted

Correct me if I’m wrong but haryana CM has clarified that the reservation is not applicable to technical jobs. It’s only for blue collar jobs and will only impact the manufacturing industry. Brookfields has mostly MNC and Tech tenants in Gurgaon who are not at all impacted. I know the sec 21 techspace asset and it is occupied by the likes of RBS, Accenture, E&Y, BoFA - companies which will not be impacted. Their biggest concern as of now is covid given that occupancy has dipped as per IPO filings.

Rishi

Unfortunately CM made the law under duress of the trust vote. They are now making the rules and have approached industry.

Possibly CM may have made the announcement…but local people are not sure of impact yet .

Sec 21 Dundahera asset is owned by one of my portfolio companies. Have a look IST Ltd. Vacancy is increased from 6 to 8 percent or something like that

Occupancy has declined only marginally in last 1 month and is still 90%+ which is good. Mgmt believes that the COVID related churn which had to happen has happened largely.

Little or no pressure on rentals. New leases in-line with projected rentals and contracted escalations achieved.

Business for most of the tenants (mainly IT) is back up and at good levels now; they’re hiring for future demand and this should translate to demand for more space once things open up. [I am not sure if there is a one-to-one correlation here; many cos are getting more comfortable to the idea of long WFH so hiring may not mean demand for space]

Impact of Haryana reservation bill yet to be understood as rules aren’t final. [This will be an important factor going forward as the trust gets 40%+ rents from Gurgaon G2 asset and another Gurgaon asset (G1 Sec 48) is in their acquisition pipeline.]

No details around distribution and its split into dividends / interest. So investors have to wait to analyze the yield until 1st distribution after Jun-21 results.

Good time to enter at current levels? Or is it too early and one should wait? Suggestions pls.

My view on Embassy REIT

Post Covid-1, for regular income generating investment (debt/hybrid asset allocation), I have simplified my investment with very basic question, “How has the SPV/structure faced that situation and what was impact of interest/distribution of cashflow from that SPV?”. Since Brookfield and Mindspace (just listed if my memory is correct) did not have distribution history during COVID-1, Embassy is only available choice to invest for me.

Secondly, being based out of Mumbai, I would be keen to look at REIT which have relatively lower investment in Mumbai RE. Further, I am positive about IT industry and hence would be keen to look forward to Embassy which have reasonably large assets pool from Bengaluru vis Mumbai.

While Mindspace/Brookfield have reasonable asset share from Mumbai as compared with Embassy, I continue to like Embassy currently.

Lastly, among all listed REIT, I find Embassy REIT management being most transparent and professional. This is my subjective evaluation and it may be biased.

Disclosure: I have invested in Embassy REIT and my view may be biased due to same. Reader shall do his/her own due diligence before making any investment decision. I am not a SEBI registered analyst. I am also not recommeding any investment action.

Apart from covid cases any other reason for not liking asset share from Mumbai? As Mumbai assets yield higher rates compared to other cities and space being a constraint, they are always in demand.

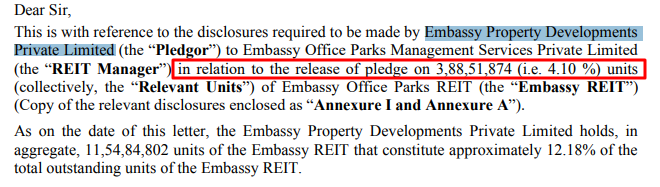

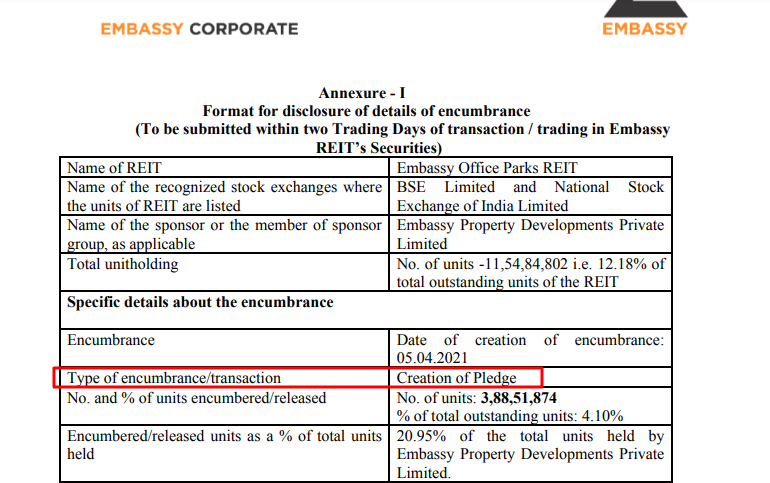

Jitu Virwani has not been that minority shareholder friendly, views on that ?

Since I already own house and tiny office in Mumbai, my exposure is materially (say 100% of RE, if one consider house and office, both for self consumption as assets). Hence, I would like to diversify. That is the main reason for wanting lower Mumbai assets REIT and not COVID. COVID may impact prospect of 1-2 year horizon, but in long term would have limited impact but for chnge in society attitude being more receptive to work from home.

In my understanding, with same Jitu Virwami, Embassy price increased to more than 500 and market cap reached to great height. Secondly, I see Blackstone as more in control of business than Embassy. Thirdly, if I look at business information disclosure and transparency on same, I find limited reason to suspect intention of Virmani.

I have created a thread on VP for Embassy REIT and would request members to post their view in future on that thread related to Embassy REIT.

Did a quick study on REITs in the USA… posting the little I’ve learnt here

Data center, Storage space REITs trade and have traded at premium to NAVs. In the future if we have more REITs on the bourses this sector is one to look out for.

At the other end of the scale Retail, Malls are usually at a huge discount.

Currently in India we have only commercial office based REITs. These are currently trading around 20 to 30 percent discount to NAV in the USA too

Historically REITs have given better returns than the S&P500 over a period of 20+ years.

Historically almost all REITs trade at or around NAV. Anytime they cross NAV it’s just been noise and misinformed traders. So buying when discounted to NAV is the best option always.

Dividend yield in the USA by the main players is approx 2.5 to 3 percent. The median is above 4 percent due to huge discounts to NAV of retail, malls etc.

Extrapolating the above for India:

Currently most REITs are far below NAV. In the long run they’ll trade around their NAV atleast. However, India is a bit unique.

Our interest rates are a lot higher than the USA. The long term trend for India has been decreasing interest rates from the 90s(double digits) to today(5 to 6 percent) and REITs can only trade at premiums to these always.

However, with these kind of instruments you have to factor in the long run…

Over the next 15 years will interest rates decrease further?

That is the trend globally and has been the case in India too so there is a likelihood they will. As interest rates decrease the premium to an REITs yield will decrease too and hence why prices of our REITs could rise much faster than those abroad. We may reach a position where the REITs here trade at huge premiums to NAV too if this is the case to counter the yield premium. There is a huge chance this could be the opposite in the short term ie interest rates could rise. But with an asset like this the long term matters for holding and the short term matters when buying

Over the next 15 years will prices of land atleast double?

At 5 percent per year they should double. Also WFH could be a trend long forgotten by then.

The Government loves investment trusts in the USA because it helps grow infrastructure without much government intervention and this could just be the start of the governments push for trusts in india. For eg the budget made it easier for foreign investors to invest in REITs here: India emerges as global hotspot for commercial real estate investment - The Financial Express

So even FIIs have an alternate means of investing REITs at bigger yields now.

All things considered at current prices even if the above long term lowered interest Vs REITs play doesn’t pan out you have land appreciation and a good yield at CMP + the huge discount to NAVs. If it does play out you could have a situation where REITs trade at 2.5 to 3 percent yields in 15 years… which means their prices will need to rise to make up for this and hence why the fledgling REIT landscape in India is interesting Vs abroad.

Due diligence will be needed since not all REITs are created equal and there may be teething issues in India. But this is a very interesting space long term