Correct, also the REIT should not take significant debt to end up servicing that in urge to grow assets…is there any regulations on that so that the managers kept by the sponsors of REIT act in favor of minority shareholders? Thanks

It is debatable whether this would be a good or a bad decision. If a debt funded purchase leads to higher yield than the loan then it makes sense to take that loan. If REIT can raise debt at 6% and get 7% net distributable cash flows, then it makes sense to take that debt because eventually the debt would be paid down and only the cash flows would remain.

Idea is not for a debate, I agree with you the decision can be good or bad. For me, this is a very big variable to track and judge for an avenue that I have chosen for regular income/capital protection. Hence not able to decide in favour till now. To each his own set of risks and comfort level. No debate, just a perspective to think and discuss. Thanks

1 Like

Let me rephrase what I was saying. If one were offering a person A a deal wherein they could buy a flat for 70 lakhs, and get 50k for the rent, for an emi of 50k should they take it, or not? From what I have seen everyone takes this deal. Because it implies that in X years, one has a flat, and the flat practically pays for itself with the rental yield.

I believe for same reason it makes sense for a ReIT to do the same as well. If the rental yield is higher than emi then it makes sense to make the transaction. Just my 2 cents.

2 Likes

Guys I’ve analysed real estate for some time but I am new to REIT space and just trying to explore for the last few days. I do have some concerns however - would welcome your inputs on these.

-

This is definitely a good instrument for earning 6-7% post tax income on CMP. However, I’m cautious of any growth in dividends here. Thing is these guys have a mandate to distribute almost all of their cash flows to unitholders and are not left with any growth capital to deploy. For addition of new assets, they will have to raise debt + equity which will lead to dilution. While earnings will increase substantially due to acquisitions, distributions / unit might not increase so much due to dilution effect. E.g. in case of Embassy, as @Krishna1 mentioned, their FY20 distribution was Rs 24.4 / unit in FY20 and their projected FY22 will also be at the same level (FY22 number is optimistic IMO though) despite adding 28% more space due to ETV acquisition. Does anyone have a view on this? Any experience from more developed markets with longer REIT history?

-

I see sponsors / promoters selling their own assets into their own REITs (don’t know the full form of ROFO

). Although regulation require these to be sold at 90-110% of avg of 2 valuers’ opinion, I do not have confidence on whether these are fairly priced transactions. E.g. Embassy REIT bought ETV from Embassy the developer at $1.3bn price. How much project cost did Embassy the developer incur to sell it at $1.3bn? Or what is embassy the developer’s profit % in this transaction? Is it market standard or higher? Will this asset be sold at the same price if not for a REIT? It seems to me that REITs might be good exit routes for developers - they have a ready buyer at a price determined by a 3rd party.

). Although regulation require these to be sold at 90-110% of avg of 2 valuers’ opinion, I do not have confidence on whether these are fairly priced transactions. E.g. Embassy REIT bought ETV from Embassy the developer at $1.3bn price. How much project cost did Embassy the developer incur to sell it at $1.3bn? Or what is embassy the developer’s profit % in this transaction? Is it market standard or higher? Will this asset be sold at the same price if not for a REIT? It seems to me that REITs might be good exit routes for developers - they have a ready buyer at a price determined by a 3rd party. -

While all the commentary in investor docs talks about WALE (or WAULT to expiry), I have not seen any mention of a similar metric called WAULT to break (tenant’s option in a commercial lease where it can opt out). Do we have any idea around tenant only break options in A-grade office leases in India? So what I am saying is that a 10 year lease with tenant’s break option in year 5 becomes riskier in current times and tenant is more likely to choose this option. So some info on breaks would help in the analysis.

Your suggestions / inputs are welcome.

7 Likes

Usually the asset addition is DPU accretive. In Embassy’s case specifically the dip in DPU over the last two years is more is due to businessmix (in addition to Office they have a chunk of income from Hotel, Food court and Power business which has got severely effected and which are not such a large part of the other REITs). I feel growth rate of 4-5% can be assumed safely - it would be mix of rental increase and DPU accretive actions like acquisitions and dispositions (though their is still time before we see dispositions)

Yes, there is always an inherent conflict and it does play out. So you can safely assume - their is a 10% valuation which gets pushed up by these guys. So it always makes sense to buy REIT only if their is a 15-20% discount to NAV.

WAULT - even though its a good data to have - doesn’t really tell me anything. Clients wont just pick their bags and leave a premised as their lock in has expired. They usually spend a substantial amount of money in interiors which they would loose to move somewhere else and 2nd factor is some of the clients who are sitting on lease deeds entered 5 to 10 years back is that they are at substantial discount to market which forces them to continue with the lease deed (unless they have a compelling business reason to move out - space not enough/ or too much, business not doing well,location problems etc.)

9 Likes

Any REIT beginners who are confused about how the income is distributed.

Excerpt from Embassy REIT AR:

The Board of Directors of the Manager to the

Trust, in their meeting held on May 19, 2020, have

declared distribution to Unitholders of 6.89 per unit which aggregates to 5,316.77 million for the

quarter ended March 31, 2020. The distributions of

6.89 per unit comprises 2.49 per unit in the form

of interest payment, 0.23 per unit in the form of dividend and the balance 4.17 per unit in the form

of amortisation of SPV debt.

The above under light of tax can be seen as →

Tax implications of the distributions in the

hands of Unitholders

The income-tax treatment for distributions by

Embassy REIT in the hands of the Unitholders

under the Indian Income-tax Act, 1961 (‘the Act’)

read with the Income-tax Rules, 1962 (‘the Rules’)

applicable for Financial Year 2020-2021 are as follows:-

• Interest income - Taxable in the hands of the

Unitholders at the applicable rates.

• Dividend income - Exempt in the hands of the

Unitholders.

• Amortisation of SPV debt- Exempt in the hands of

the Unitholders.

• On sale of Units:- Long-term capital gains

exceeding ` 1 lakh on sale of units held for more

than 36 months– 10% (plus applicable surcharge

and cess); and Short-term capital gains on sale

of units held for up to 36 months – 15% (plus

applicable surcharge and cess).

Experts please remove it if this is below layman level

5 Likes

Thank you so much for taking time to address my queries - appreciate it. Just a few follow-ups ![]()

WAULT - even though its a good data to have - doesn’t really tell me anything. Clients wont just pick their bags and leave a premised as their lock in has expired. They usually spend a substantial amount of money in interiors which they would loose to move somewhere else

Fully agree with tenants investing substantial amount in fit-outs which acts as friction against moving out. My point was mainly around the current downturn where tenants are paying substantial rents but not using the space - they will have an incentive to at least reduce the footprint, if not move out fully. Anyone who has a break coming up during this period or is not in a lock-in is more likely than before to sit at the table with the asset owner. So in a way I am suggesting that the business reason to move out / reduce space has become more compelling.

E.g. Embassy had 2.2m SF space up for expiry in current year. They could only renew for 0.7m SF. Mindspace could only manage 1.4m SF out of 3.3m SF up for expiry and early expiry (I think this is alias for break option). A large portion of these tenants (supposedly large / MNC clients) did not renew the lease although most of them might have incurred some fit-out costs. So WAULT (expiry / break) is not as relevant in a BAU scenario IMHO but its importance has increased in current times as tenants who have the option of reducing the costs are more likely than ever to do so. As an investor I would want to stick with a REIT which has higher % of income locked-in for a couple of years.

2nd factor is some of the clients who are sitting on lease deeds entered 5 to 10 years back is that they are at substantial discount to market which forces them to continue with the lease deed

With c.5% p.a. rent escalations built into the leases, are they likely to be in a scenario where they end up being at a substantial discount to the market in a decade or so? Do the market rents for offices increase at a much faster pace (I don’t have any data on this)?

1 Like

I think they report it in the filings. Basically asset values minus debt. Assets are revalued annually so this is not a volatile factor.

all REITs disclose this information. Instead of getting spoon fed - would request you to do a bit of research. In case you are still not able to find, please DM and I would send it to you.

2 Likes

Yes, clients are paying the rents for not using the space. But you need to remember - companies take such decisions keeping long term in mind and not short term gains. Imagine you are a Bank with a GCC on ORR Bangalore, you are currently not using space and so decide to move out - you move to Whitefield to save rent - moving within ORR would not be worth the loss of fit out and paying brokerage etc. Suddenly your employees are no longer keen to work for you. So what is more important - employees or rent?

Leasing is definitely slow and since international travel is restricted its making matters more difficult. In any normal year you would have 5-10% of your clients leaving and you are not able to close this space which normally you would have done. Clients would definitely use this opportunity to negotiate lower rents and market rentals would remain under pressure for medium term period (2-3 years). The growth for REITs would come from DPU accretive acquisitions and completion of under construction portfolio - Embassy and Mindspace has a portion which would get completed over the next couple of years.

yes. Market rentals have grown at higher rate.

4 Likes

Really great video explaining how ReITs work:

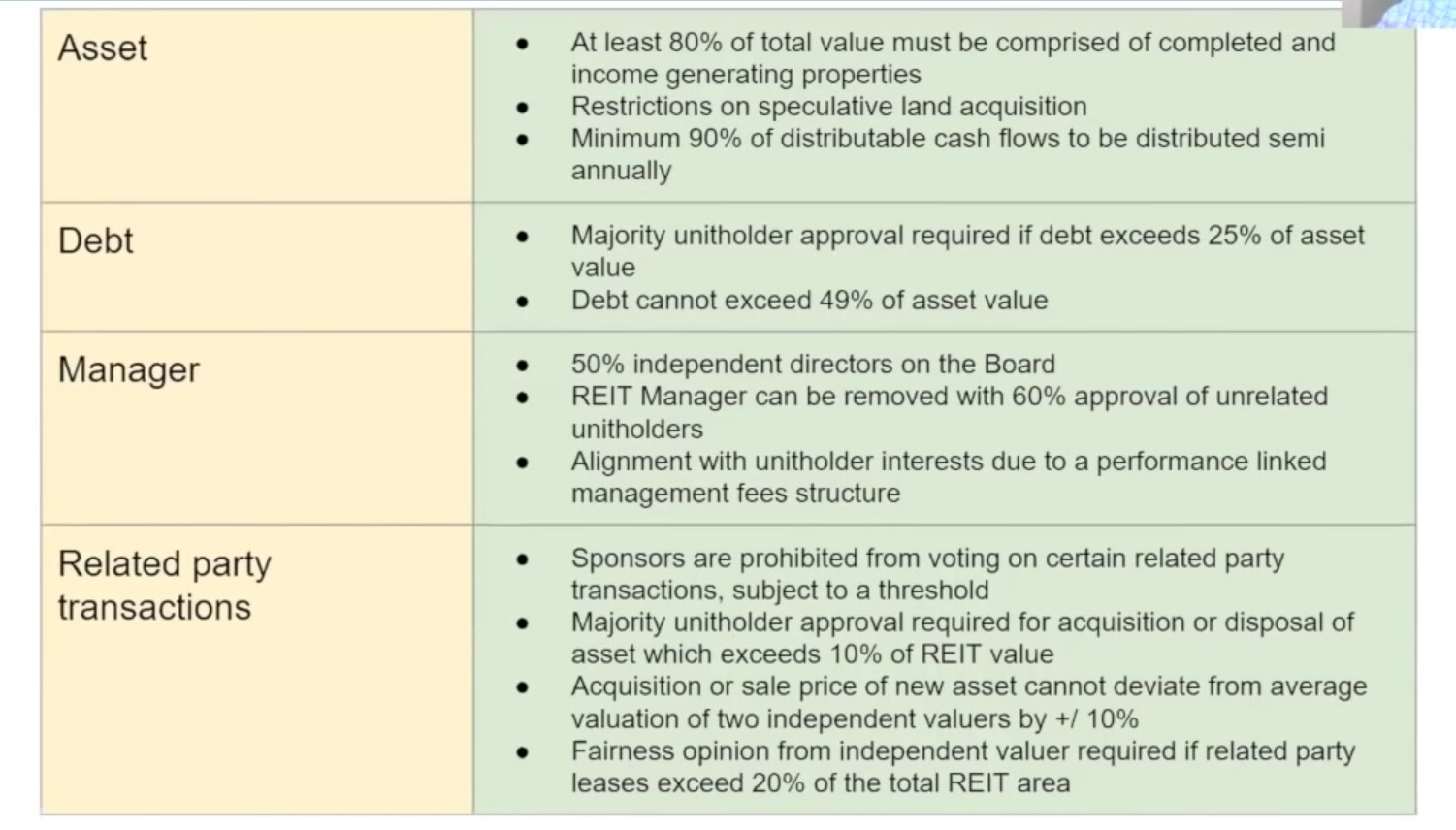

Few very interesting slides which answer some questions raised about:

RPT, Debt :

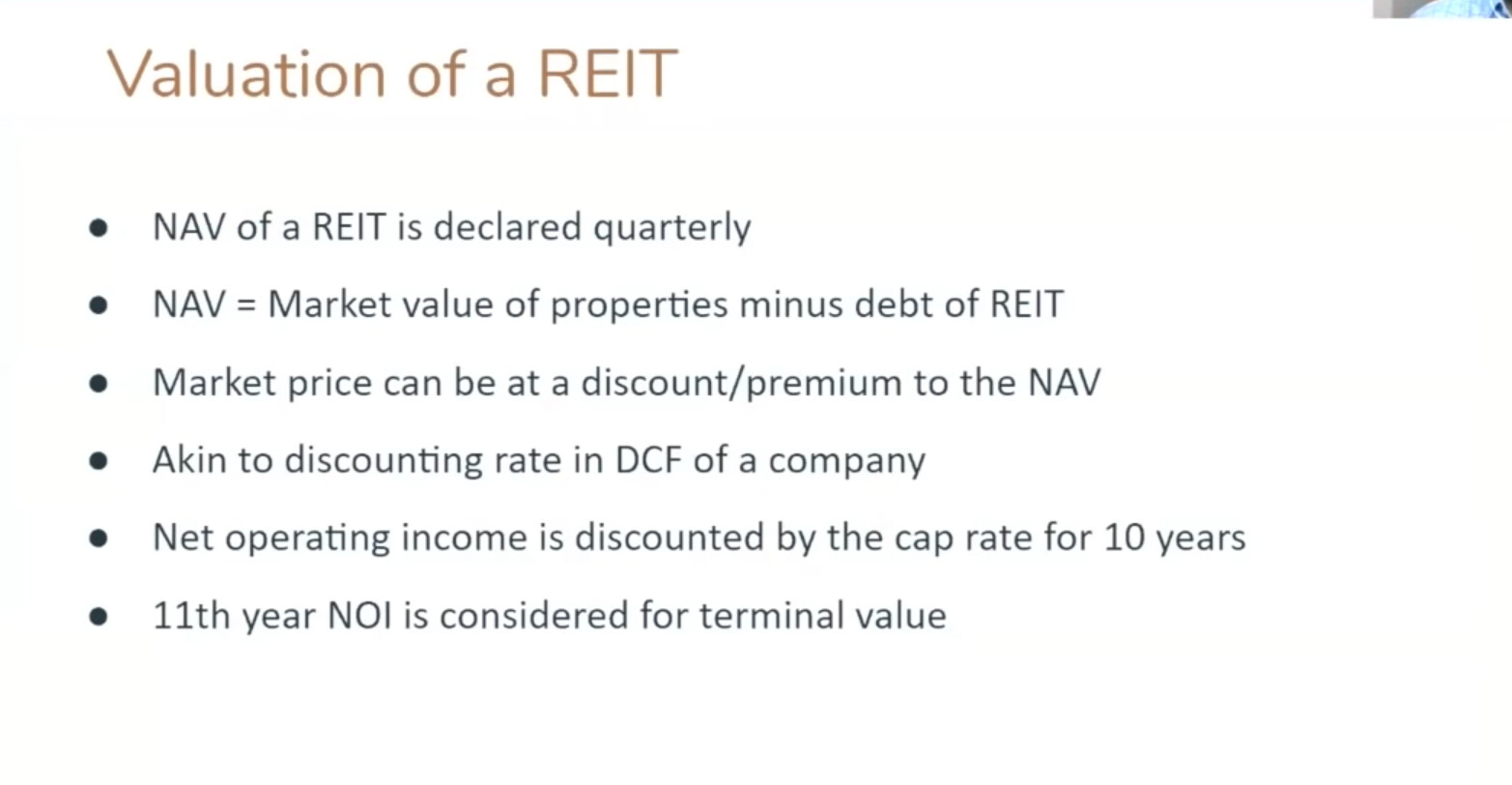

NAV calculation

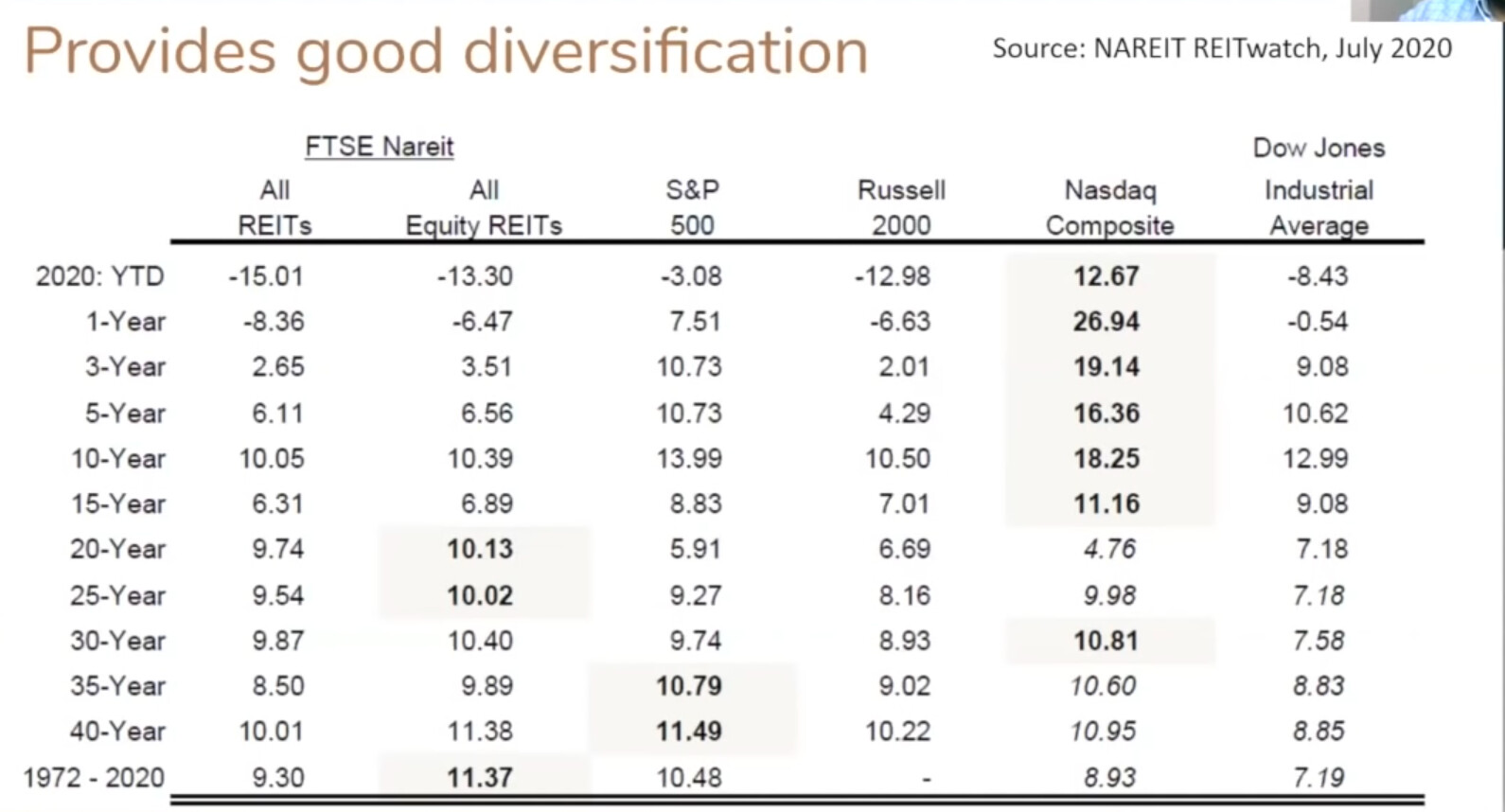

Equity REIT investments have outperformed even equity in last 50 years in US:

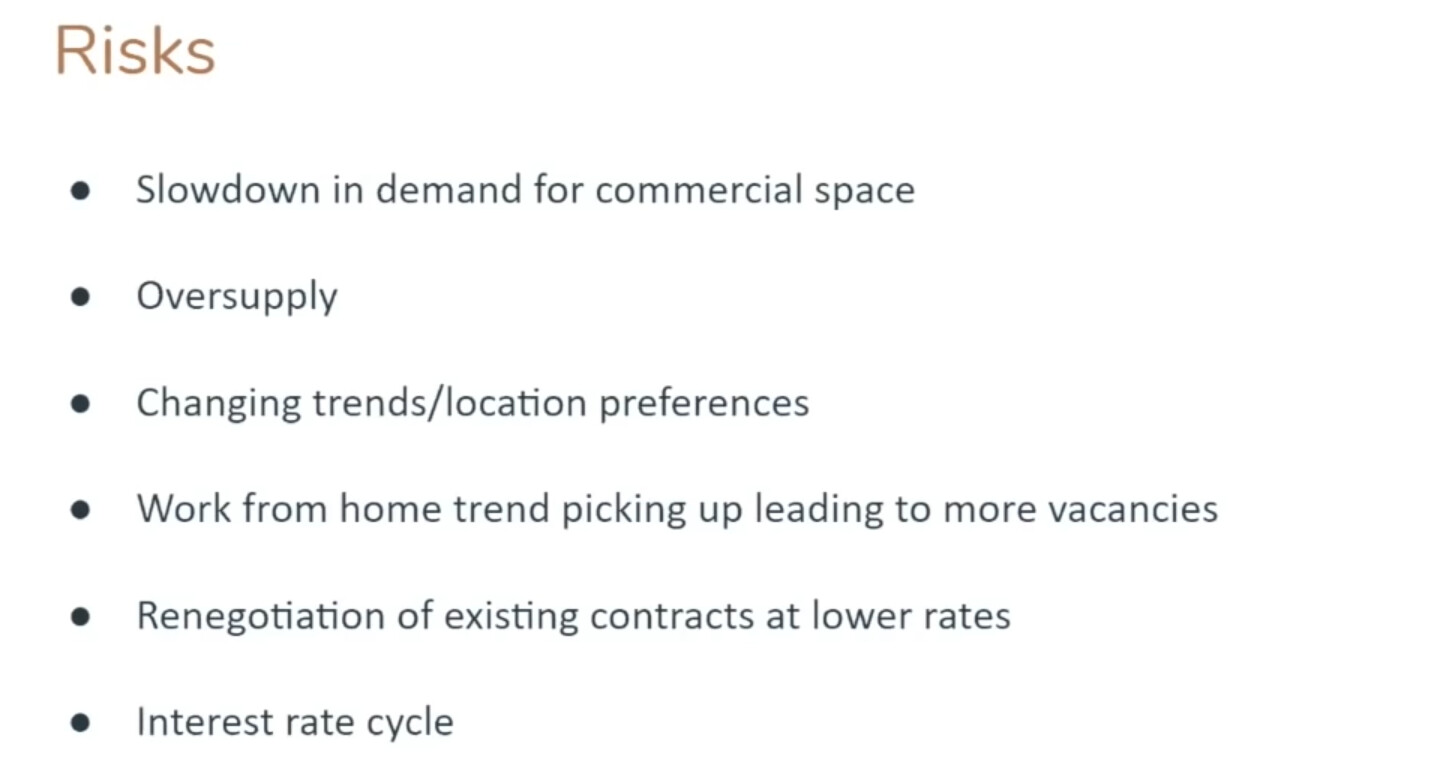

Some risks:

Disc: Invested in Embassy

4 Likes

Hi,

Can anybody give a comparison between Embassy, Mindspace and Brookfield REIT? If you need to choose one, which one should it be?

From the taxation point of view, Mindspace REIT is better than Embassy REIT, although Embassy scores big in the quality of the underlying properties, I believe.

1 Like

Brookfield, as it’s post tax return for most investor brackets is way higher…and it has a good pipeline.

Any idea why the market is valuing Brookfield REIT at the steepest discount to NAV?

Is it just a case of negative momentum after listing ? Debt levels post IPO look manageable and the properties are good.

Thanks

Brookfield REIT NAV is as of 31st March 2020, while for the others, it may have been updated on 30th September, I believe. Just something to keep in mind.

1 Like

The assets are well occupied but they are not super prime. This is not that they are sub prime. The pipeline assets are very good.

Also among the listed peers the taxation is not very friendly as distribution is mainly interest. Even though price with relative yields is comfortable vis a vis peers.

3 Likes

Hi,

How do you compare the quality of properties of all three REITs?

All three REITs have their properties at prime locations with good number of Fortune 500 Clients.

Hi Kaustav…I know the properties very very well. But you are free to make your own judgements which you should do!!

REITs in India are very complicated for me. Distributions are interest/dividends/capital return - too confusing…

I have significant investments in REITs overseas, where distributions are dividends only. Also the management structure is very transparent - internal (management incentives are very much aligned to other investors in the reit) or external (management gets a fee to manage properties - there is a conflict of interest here, but as long as it is transparent it is fine)

Also the way the REITs buy properties from related parties/promoters makes me very uneasy - what is the market price? Who decides the market price - promoters? Or is it valued independently by a certified valuer? Are they really independent?

The incentive for the management is also very confusing and I don’t think their incentives are aligned with other investors in the REIT - ie I suspect the management structure is external (they have not clearly specified this info).

My understanding is that the properties are managed externally by the manager, they get a fee for managing properties and the fee depends on the NAV! The higher the NAV the higher the management fee - so it makes sense for the management to buy properties from the promoter at inflated prices to boost NAV… If the assumption is true, NAV could collapse in the future and hence the reason why the market prices of these REITs are at a discount to the NAV

I could be wrong in above assumptions. I will stay clear of REITs in india for now until they simplify the management structure. Also they can’t increase the rents 10-15% every year/at every rent reviews - may be it is possible, but just be very skeptical of the double digit rent increase predictions from the management, this may not happen

Discl - no investments

7 Likes