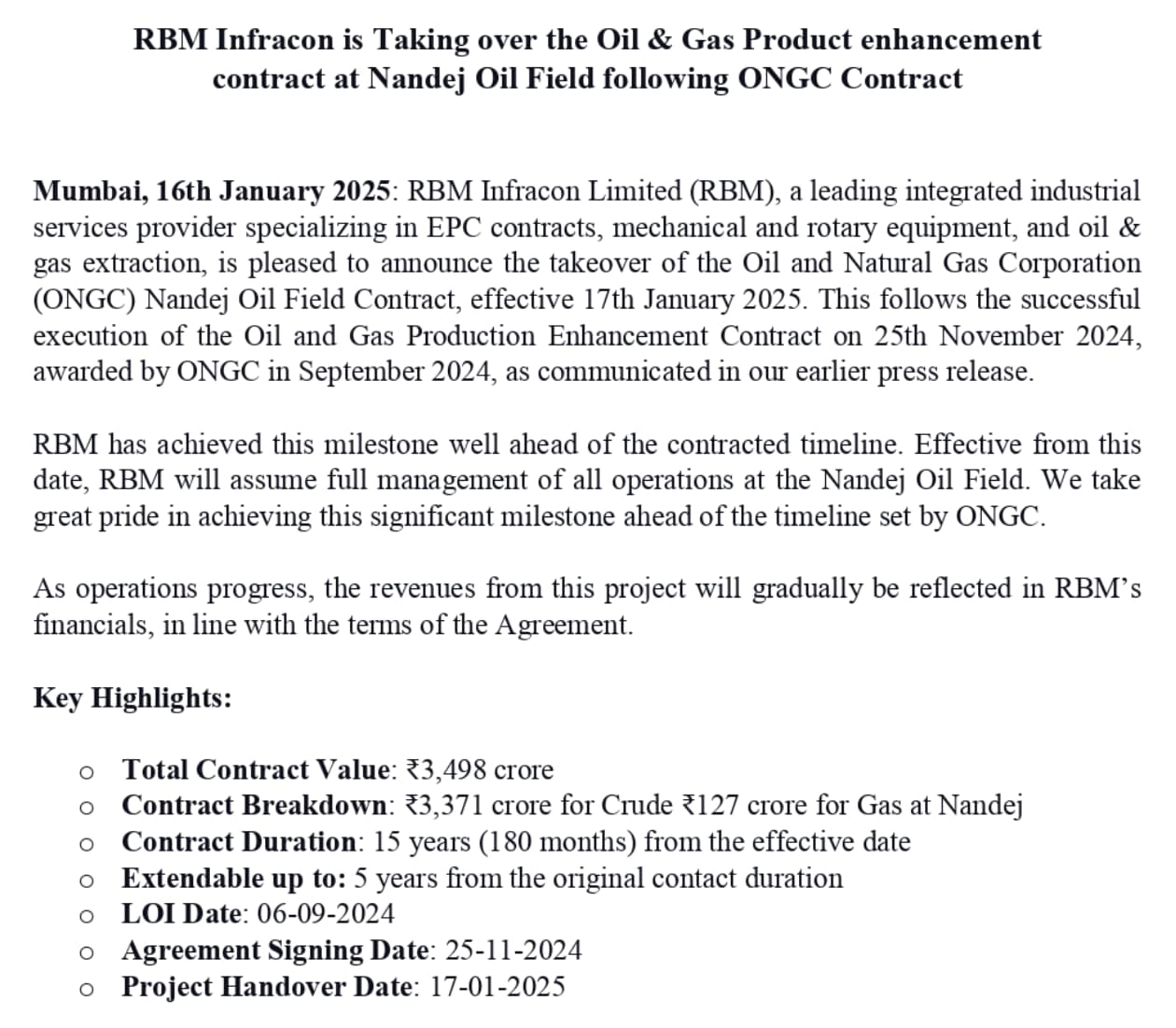

15 years is maximum limit. They can also complete the order in 12 years for eg. revenue per year will largely depend on the amount of oil extracted which no one can predict. Rough guesstimates will surely be there with company as they have hired 25 years experience personnel but not disclosed yet. As per my assumption these queries should be answered by management in Q2 concall as it will be more focussed on ONGC order and todays Green H2 order

4 Likes

As mentioned by the managing director in the last con-call -

https://nsearchives.nseindia.com/corporate/RBMINFRA_07102024174129_Press_Release_Signed.pdf

New order from L&T

https://nsearchives.nseindia.com/corporate/RBMINFRA_07102024170703_NSE_LETTER_Signed.pdf

1 Like

Discovered this thread on X, contains some info from the latest AGM.

Edit - 29/10/24

Edit - 14/11/24

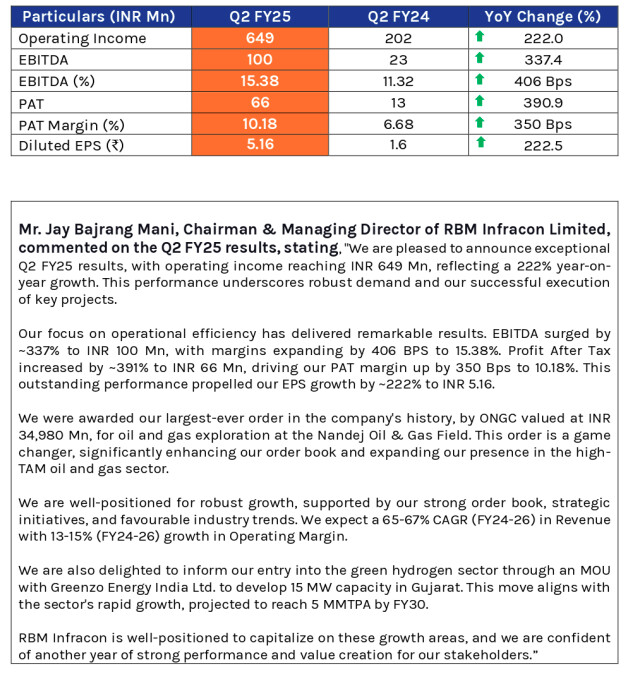

Excellent Results

YoY

Sales +220%

Net Profit +390%

QoQ

Sales +66%

Net Profit +101%

https://nsearchives.nseindia.com/corporate/outcome_rbm11_SIGNED_14112024163615.pdf

3 Likes

It seems the Management reduced their guidance for FY25 from 400 crore revenue which they had mentioned in their last concall to 214 crore (65% CAGR from FY24 levels = 1.65*130 = 214 crore). Am I reading it right?

No you are reading it wrong.

Thanks! can you please help me understand what would that statement mean in the press release “ We expect a 65-67% CAGR from FY24-26 levels….”

1 Like

| FY24 | FY25E | FY26E | FY27E | 3 years CAGR | |

|---|---|---|---|---|---|

| Revenue | 200 | 400 | 600 | 900 | 65% |

| Growth | 100% | 50% | 50% |

I hope this illustration makes sense. If not, then well I cannot explain. This is just an illustration and I am not talking about RBM in particular or their exact guidance.

https://nsearchives.nseindia.com/corporate/RBMINFRA_20112024193552_NSE_LETTER_signed.pdf

https://nsearchives.nseindia.com/corporate/RBMINFRA_20112024193710_NSE_LETTER_signed.pdf

https://nsearchives.nseindia.com/corporate/RBMINFRA_20112024193956_NSE_LETTER_signed.pdf

1 Like

Based on the guidance stocks looks quite cheap at 21.5x FY25E and 13.0x FY26E P/E

| Rscrs | FY24 | H1FY25 | FY25E | FY26E | FY27E |

|---|---|---|---|---|---|

| Revenue | 130 | 103 | 400 | 660 | 1056 |

| YoY | 208% | 65% | 60% | ||

| PAT | 11 | 10 | 40 | 66 | 106 |

| PAT Margin | 8.5% | 9.6% | 10.0% | 10.0% | 10.0% |

| YoY | 304% | 65% | 60% | ||

| P/E | 21.5 | 13.0 | 8.1 |

2 Likes

I think it’s purely a case of language fluency, most of us know that the management is not fluent in English so there is a high chance that the MD used the word Payroll instead of Contractual basis. He is just gaslighting.

1 Like

Time will tell who is right…we will meet again on this board after 1 year…!!

I have minutely gone through each and every thing…!!

Well, then you shouldn’t have missed out on the increase in material cost which is basically machinery/tools/consumables for them, might be that the nature of work changed or they have moved into automation in places they can. 1 Quarter isn’t enough to come to conclusions like this.

And by your logic or the logic of whoever the X guy is the OPM margin should have shot past the roof as the employee cost didn’t increase but that isn’t the case because other expenses increased, a capable machine can replace 100 men. The number of awards received by RBM from companies like Reliance, ONGC, Nayra Energy, Essar Oil, etc… is a testament to their quality of work. They do what others find petty. Anyway, I surely would like to see whether this investment gives me returns or lessons either way I am staying put and there might or might not be an issue but the issues pointed out here are irrelevant to me.

All the best and let’s keep learning.

3 Likes

Not neccesarily. If people are on contractual basis the costs wont come in employee cost, it will come in other expenses.

Unsavory allegations were made on Aditya Vision a few years back. See the performance of the company in terms of stock price and numbers.

I dont think ONGC is a fool to give them such a large order before doing due diligence.

4 Likes

Hi all, Their company website is showing Account suspended. Anyone know if the site was working fine earlier and it might be a temporary issue with renewal of their domain name.

Revenue in FY24 - 130 Crores

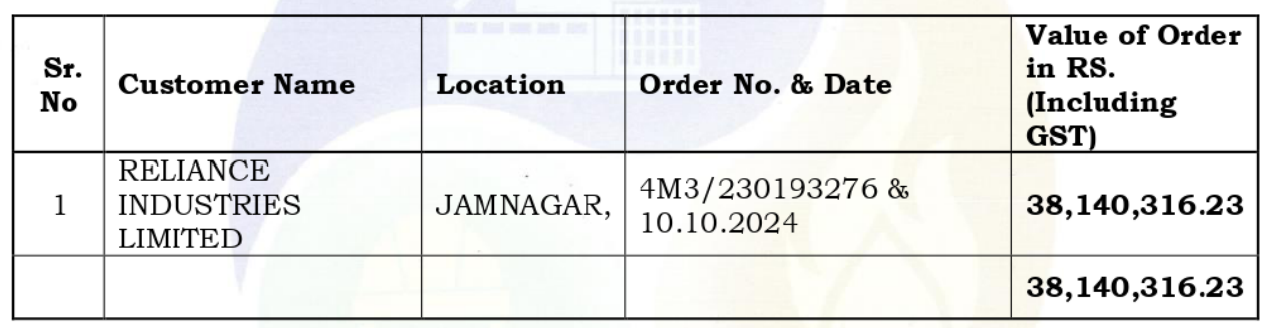

Only ONGC’s contribution in this CY - 233 Crores

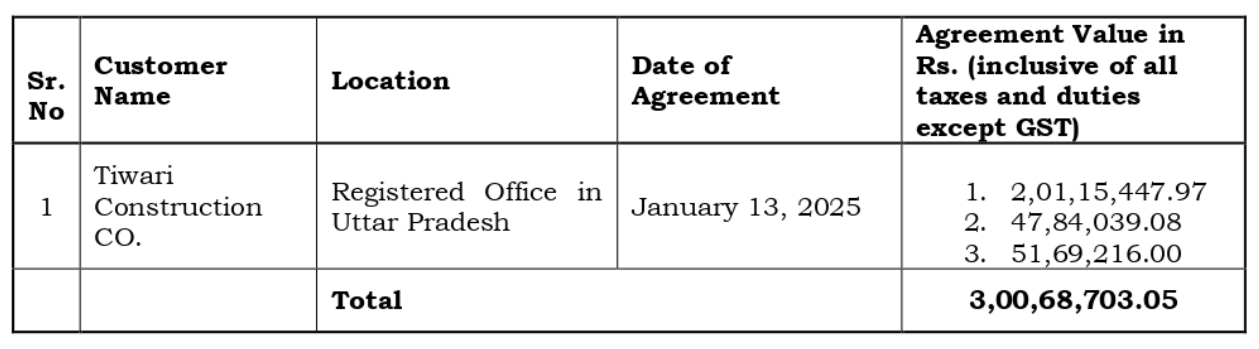

Plus many such small orders -

2 Likes

Hopefully these smaller contracts help in improving CFO which remains a cause of worry as of now.

1 Like

Bhai sab kahani he management ji…What I have observed till now…

Track cash flow very minutely please

1 Like