Compiled some notes, few days ago, Enjoy:

18.08,2024

Listed on NSE Emerge, Lot Size 200

Establishment in 1993, RBM Infracon Limited is a distinguished engineering and infrastructure company. Over the years, it has evolved into a Specialist highly professional, reliable, and safe service provider in the infrastructure service arena, aiming to provide innovative, integrated, and customized solutions tailored to client-specific needs.

Specializes in comprehensive services in engineering, execution, testing, commissioning, operation, and maintenance, primarily in the mechanical and rotary equipment sector.

This co. basically used to do the shutdown/overhauling of Nayara(Essar) and Reliance. These two companies are too big to do these kind of yearly shutdowns on their own and hence use companies like RBM to perform shutdown. But lately RBM has grown its business line and has become an EPC player.

Its expertise spans various industries, including Oil & Gas Refineries, Gas Cracker Plants, Coal/Gas/WHR based Power Plants, Petrochemical, Chemicals, Cement & Fertilizers.

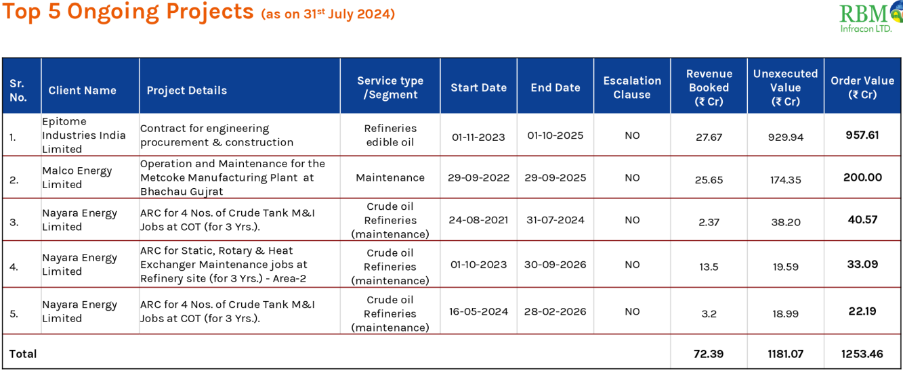

Major Clients:

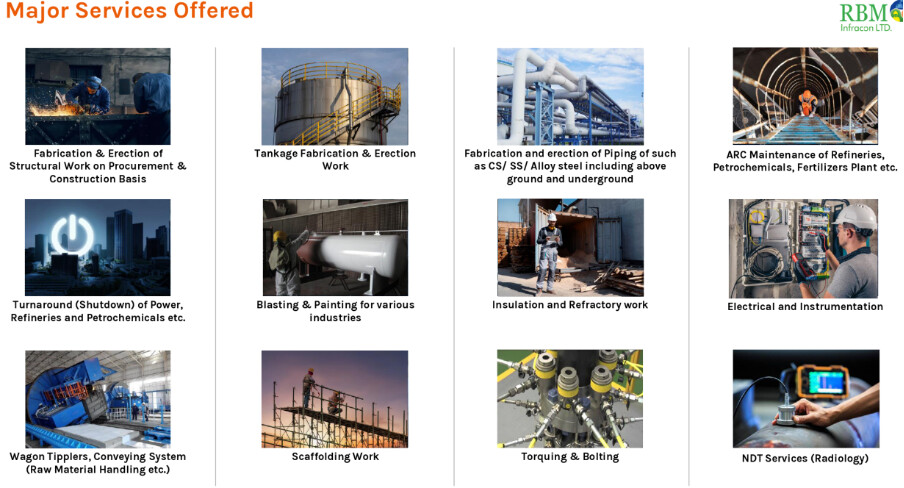

Main Lines of Work:

Piping Services

Plate Work Fabrication and Erection

Structural Steel Work

Civil Construction

Coke Plant Maintenance

Tanks, Silos, and More on EPC Basis:

Erection of Plants and Equipment:

Blasting Cleaning and Painting:

Insulation and Refractory Work

Work shop Specialists

Rail wagon loading

Operation and Maintenance services

Turnaround services

Operation & Maintenance of Heater & boiler

Operation and maintenance of Fertilizers and cement plant

In today’s interview with Tiger Assets, the management spilled some beans . It was an online event and I attended it.

Highlights:

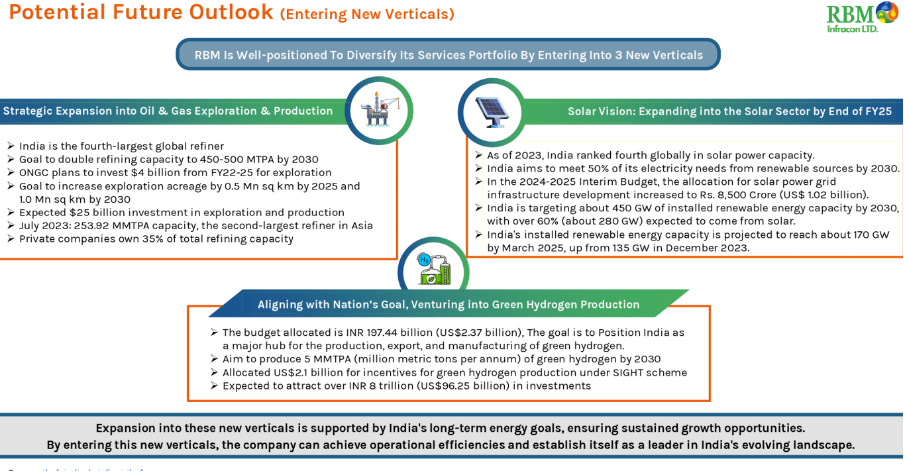

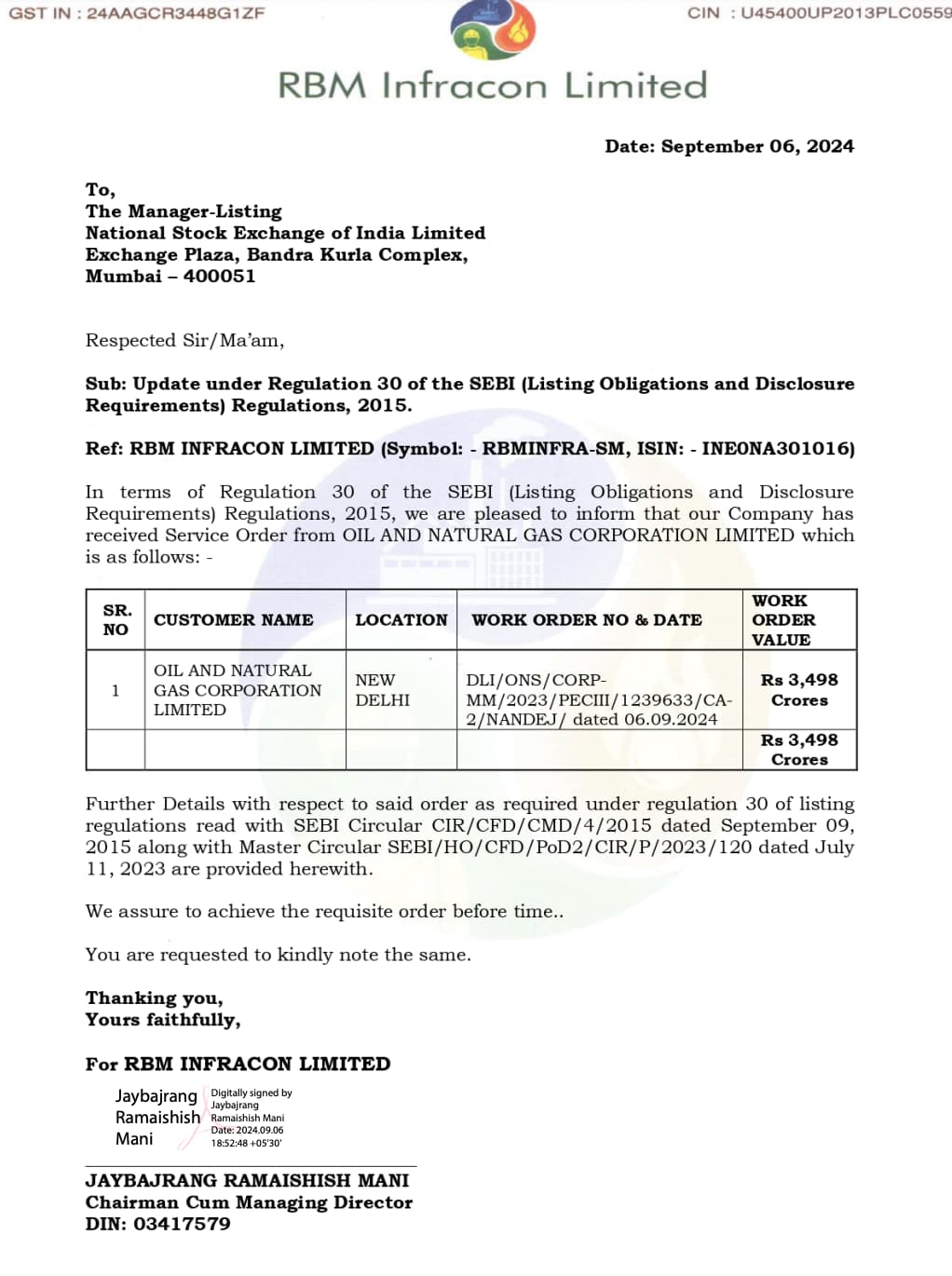

Mr Jaybajrang Mani, Chairman & MD, told that they have clinched a Rs 2000cr, 15yrs deal with ONGC for Oil exploration. The LoI is expected by 30th August. The contract will state that ONGC will allot RBM with 132 wells for digging crude oil and natural gas and they would share it a ratio of 65:35.

65% of the output would go to RBM and the rest 35% would go to ONGC. This means that for 15 long years, RBM can keep on digging crude oil and natural gas from those wells and the chairman has also assured that the revenue potential from this contract can very well go beyond 2000cr. In his own words:

“Yeh Project Toh Samander Kee Tarah Hai, Jitna Chaho Paani Nikaal Lo”

Also he told that they have almost clinched a deal of Rs 500cr, for a Solar project with Reliance. Company has worked on Solar for the past 1 year with Kalpataru and other companies.

He said that PAT can grow upto 10% from next year onwards as ONGC project is higher margin (20-25%) although Reliance can be only 6-8%.

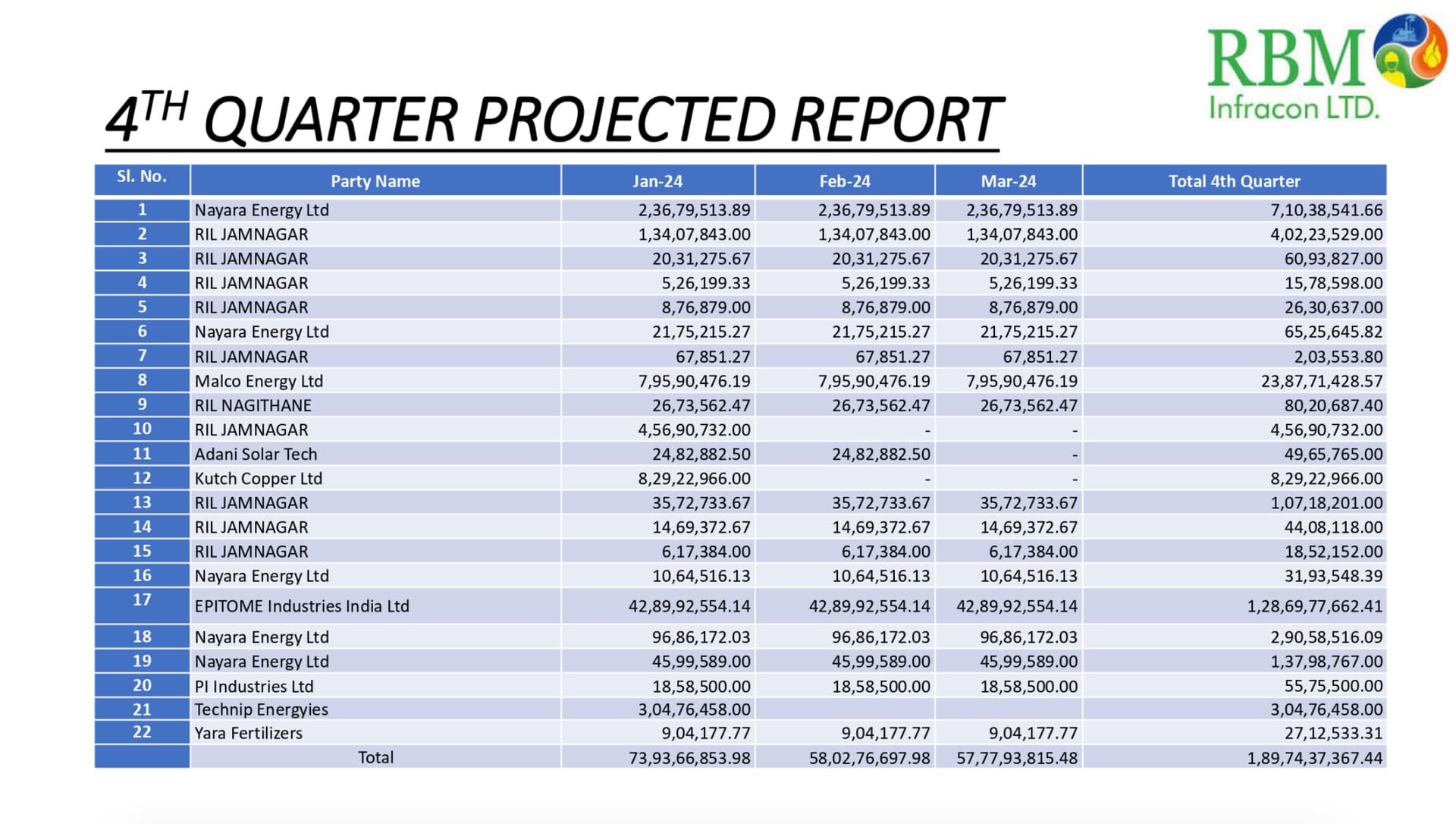

Also explained the reason for realisation of lower revenue this Q, the left over revenue will be added in coming Qs. Epitome order is done around 200cr but invoice is not generated and from next month the work will start.

The revenue guidance is Rs 400cr for the current financial year and Rs 1000cr for the next. Targeting 5000cr revenue in next 5 yrs.

The company is in negotiations with Greenzo Energy, a Gurgaon based company for Green Hydrogen project. The good news may come in few weeks. He sounded confident.

Greenzo has Govt. approvals for Green Hydrogen & Ammonia Projects.

https://www.greenzoenergy.com/

Challenges & Working Capital:

- Delays in material delivery

- High working capital needs

- Debt funding options: Rs.250 Cr preferential issue planned along with funding from bank.

Management & Operations:

- 1,700 employees (500 contract-based)

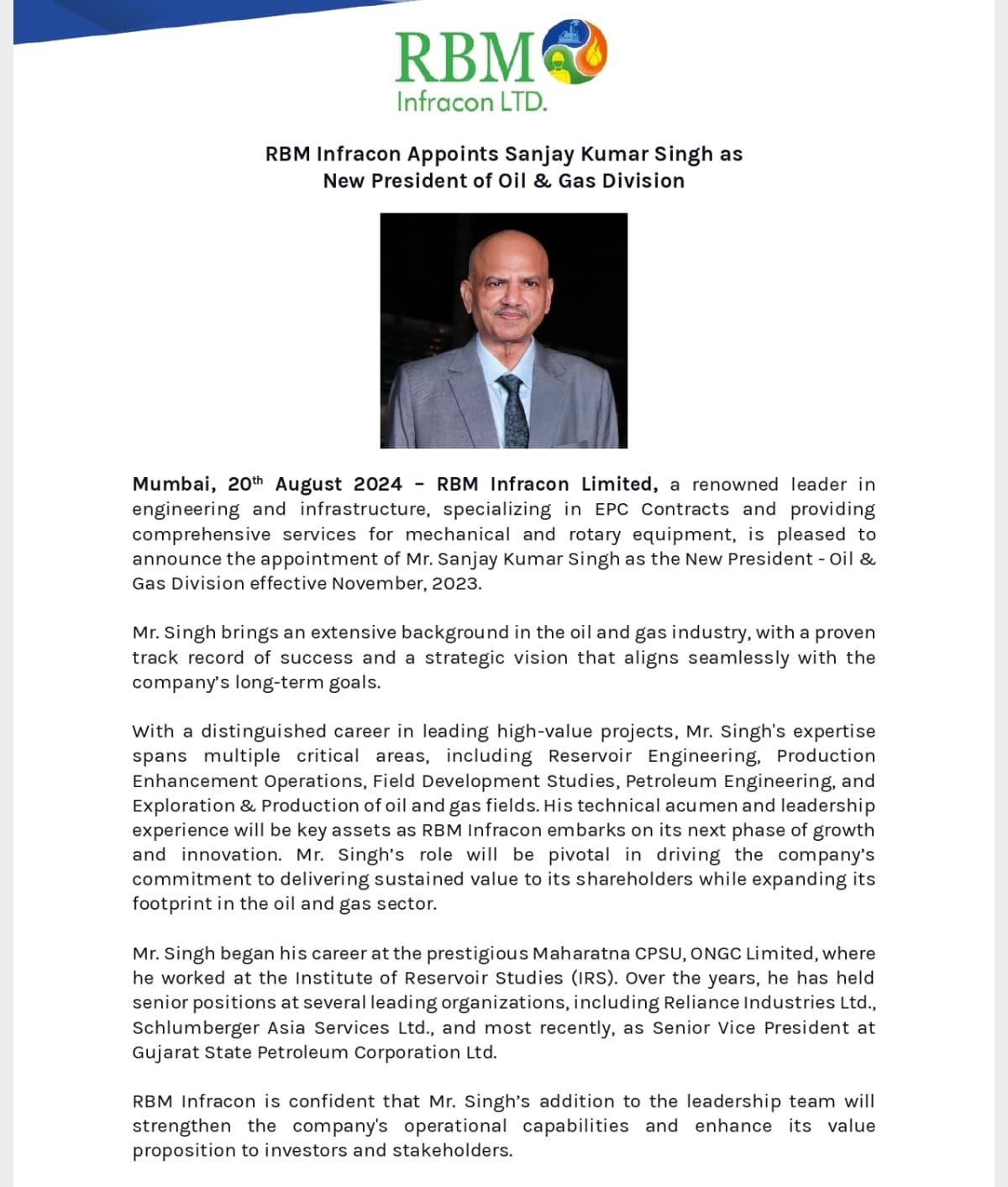

- Ex ONGC executives hired for project execution

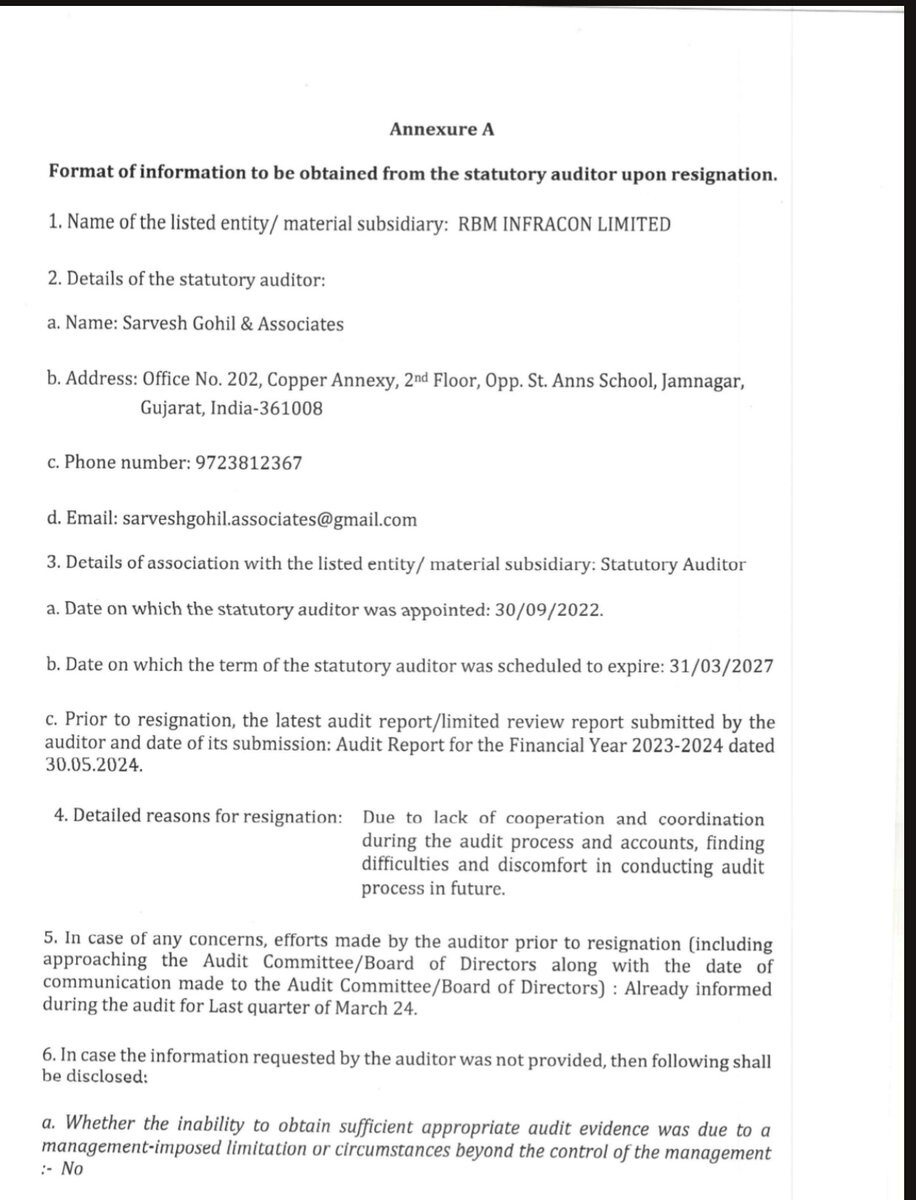

Auditor changed due to excessive delays at the auditors end. They were not able to comply with compliances on time.

Sector Expansion Plans:

- Exploring coal mining and gas sector opportunities

Capex Strategy:

- Future plans to reduce Capex by engaging more subcontractors for larger projects

The Promoter holding is shown wrongly here, its 60.53%, reduced from 72.4% as 1662000 shares have been allotted at a premium of Rs.376 per share on Preferential basis to non-promoters in February 2024. There is no insider selling.

Compiled Notes from here & there, no position as of now. Do your own diligence.