Two new filings by RBL on exchanges one confirming raising 2600 cr and the other about its key ratios and operational updates:

1 Like

1 Like

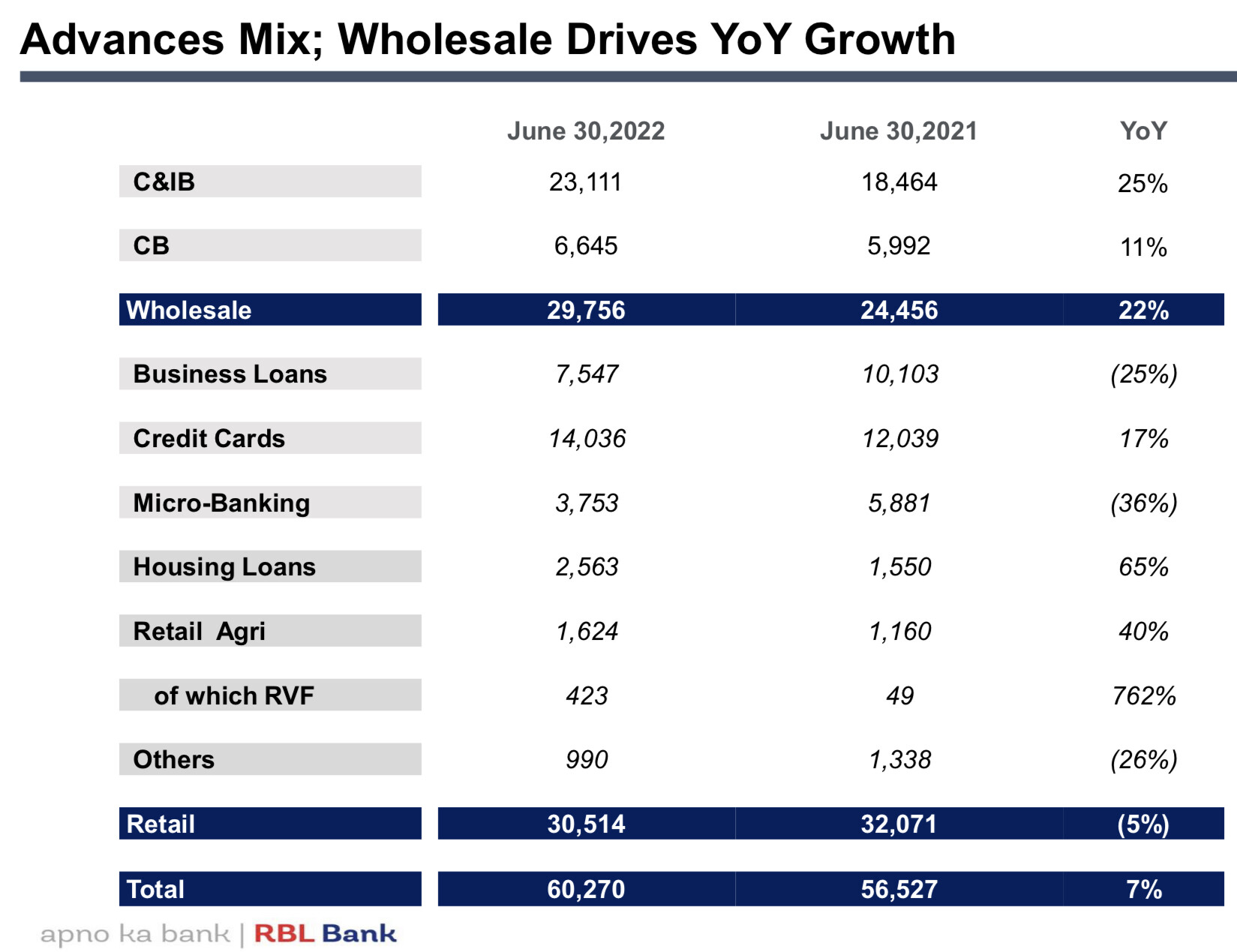

Advances have a slight growth. Interestingly retail is flat and the growth came from wholesale.

1 Like

Observation:

Almost all the active mutual funds, apart from hdfc, franklin and a few other, that had rbl bank have sold out completely

So about 350 cr of selling had to have happened in a week of dec.

Disc: recently invested, planning to hold

Some key takeaways from the call:

a) The risks on the asset side were allayed.

b) The deposits have normalized after the initial run.

c) NPAs and provisions will keep coming down.

d) maintained the guidance of ballpark 1% RoA and PCR of 65% for Q4.

The key thing for me was the increase in opex and cost to income ratio. The bank could have gone slow on the Credit card front to control the opex but the way I look at this is that the increase in opex is a matter of choice and the bank is sacrificing short term profitability over a better and more profitable book. From the presentation:

The management had said that almost 75% of the increase in opex increase came from the Credit card business which means out of the 180 cr. increase in opex , around 135 cr was for CC. If one looks at normalized levels and assuming other parameters like PCR etc remaining same the RoA could have reached the 1% number this quarter itself if the bank had chosen to go slow in the CC business.

Discl.: Invested. I have added/sold the stock in last 15 days.

4 Likes

The Ken covered RBL Bank and its co-branded partner Bajaj Finance in their story today.

2 Likes

Can you summarize this as the article is behind a paywall.

In eight years, RBL Bank has become India’s fifth-largest issuer of credit cards. The pace of this expansion has been such that credit cards account for about 20% of its total loan book—2X than its larger peers. And all of this would not have been possible without Bajaj Finance.

The mutually beneficial co-branded partnership meant RBL had access to Bajaj Finance’s millions of customers, while the latter received a share in the profits. Of its 3.75 million issued credit cards, 2.75 million cards are co-branded with Bajaj Finance.

But now, faced with high exposure to credit cards, the bank is being forced to take its foot off the credit-card pedal. And that puts its partner Bajaj Finance into a tough spot.

4 Likes

Notes from the Q1 concall and presentation:

Assets:

- Quite likely the bank is focusing on increasing the secured book on the retail assets side. MFI book degrew on the back of low disbursals in April and May to meet new MFI norms. More intent towards growing the housing and rural vehicle finance book. Running off the unsecured retail business loans book.

- Remains to be seen where they cap the MFI and cards book which will see lower growth compared to housing loans and RVF verticals.

- We had around INR 700 crores of disbursal in our retail business in Q1. This will be around 3x in Q2 and improve every quarter thereon.

- Credit cards, we issued 4.3 lakh cards in Q1, maintaining the run rate from Q4. The retail expense in credit cards also continued to show the robust growth, and Q1 has shown a growth of 54% Y-o-Y and, though of a lower base

- We have a base of around 11.5 million customers, which is getting added at the rate of 0.15 million per quarter. This customer base is coming from urban India through liability products and credit cards, from rural India to the large microfinance customer base and distribution network we have built. So natural corollary will be to expand the product line and new products to continue – we will continue to invest in these products with an aim to reach a critical size over next 2 to 3 years.

- Credit growth of 15-18% this year.

- Pre covid credit card portfolio was doing an ROA of 4%. Headed in that direction over the next few quarters.

Asset Quality:

- Asset quality fears have been allayed, the trend in asset quality continues. GNPA movement from 4.4% in Q4FY22 to 4.08% in Q1FY23. Provision coverage at healthy levels.

- Of the gross slippages in this quarter, INR 228 crores was in credit cards, INR 133 crores in micro finance and INR 205 crores in rest of the retail. Slippages in the wholesale was around INR 87 crores.

Operating Profits:

- Operating profits due to increase in opex towards branches, employee addition, tech, cards etc without commensurate increase in disbursals and the resultant fee income.

- Op profits expected to reach Q1 of last year levels in 2-3 quarters and expand post Q4FY23.

Management:

- No exits in senior management yet.

- We are not averse to hiring these skills, while I don’t think that there will be a change in the management team. The current team, which is heading it, are well entrenched in their area of operations. Each of them average 8 to 10 years of service, all of them are having. They know the bank and the DNA fairly well, and I’m very comfortable with the team, their knowledge level and their depth and commitment.

The company is carrying excess liquidity and is to fund credit growth over the next few quarters. No plans of equity capital raise over next 18-24 months. With increase in disbursals and fee income, opex trending down, replacement of the low yielding corporate book - likely for the company to track towards 750 cr PPOP by Q4FY23. Management has conservatively guided for provisions in absolute to be half of last financial year. With Q4 PAT of 340-350 cr, there is a decent chance to hit 1.2-1.25 ROAs in the exit quarter or about close to 10% ROEs.

The book had been priced nearly as like a fraud and bad loan book, but there has been no material divergence in reviews by RBI, no kitchen sinking by the new MD and asset quality has trended positively and mostly provisioned for. Will be interesting to see this story play out as cost to income and return metrics improves, along with an improved asset mix of capped but high yielding MFI, cards portfolio and a secured business loan, housing, RVF portfolio along with a higher yielding wholesale book.

Disc: Invested. Not a reco.

4 Likes

Thanks for the update. The street is not trusting the management at all and the skeptism is high in this counter due to the experience investors had in yes bank and dhfl fiasco. The market is valuing the bank at par with PSB like canara bank and bank of baroda. Significant valuation derating happened over the last 4 years. The bank is trading at forward pe ratio of 5 to 6.even If the management is able to deliver the question remains is weather the street will rerate it or not.

3 Likes

Bajaj Finance has a longstanding partnership with RBL Bank and forged a tie-up with DBS Bank India in June 2022 for co-branded credit cards. People aware of the developments say these partnerships weren’t seen as adequate to cater to the company’s existing customer base, which stood at around 60 million as on June 30, 2022. The number of co-branded credit cards in force stood at 2.96 million, or less than five per cent of its customer base. “Bajaj Finance has decided to venture into the credit cards business organically to bridge this gap,” said a source aware of the matter.

However, it is learnt that Bajaj Finance will remain committed to its partnerships with RBL Bank and DBS India. “The company will honour these partnerships and has no intention to terminate its tie-ups with the two banks,” said the person quoted above.

Source:

1 Like

Mahindra has presence in the NBFC field via M&M financial. M&M financial also has an AMC Mahindra Manulife which is currently not even in the top 10.

1 Like

Lot of positive noise related to this scrip in last two months. Mathew Cyriac picked up stake and seems like RBL is going to take advantage of PayTM’s challenges. Any thoughts on long-term investment thesis?

I have been looking at various banks in terms of valuation, growth guidance and asset quality. RBL seems to tick a lot of boxes yet the prices are not being appreciated. It trades at around 1 P/B value while some of the SFBs trade at >2P/B value. Any thoughts?

4 Likes

I think today’s beating of stock was out of proportion.

Hammering stock below the BV, & to it’s 52 W low.

I have seen this stock in past when it was garnering revenues of under 8k cr with NPAs in terms of percentage level equivalent or worse than today.

Yet trading at better valuations.

It looks like no one wants to touch this stock at any value.

5 Likes

RBL Bank’s partnership with Bajaj Finance Ltd. (BFL) for sourcing new credit cards has ended. The bank’s management conducted an analyst call today. Some of the things they highlighted that I could pick up are as follows:

Impact on Existing Cardholders

- The existing customers will remain RBL Bank cardholders, with no significant changes to their relationship with the bank.

- The value proposition for these customers remains intact, as RBL has been servicing them directly from start. Upon card renewal, a new card without BFL co-branding will be issued.

- Only a small fraction of these cardholders hold savings accounts with RBL Bank.

Impact on Incremental Card Sourcing

- Currently, RBL Bank has been sourcing 1 to 1.1 lakh cards a month, of which 30,000–35,000 were contributed by this partnership.

- Management expects to restore the sourcing run rate back to 1 lakh cards per month within 2–3 months - through internal sourcing and other co-branding partnerships.

- The cost of acquisition for BFL-sourced cards was approximately 25% lower than internally sourced cards (excluding trail costs payable to BFL).

Potential Churn or Behavioral Changes in BFL Customers

- As per them, based on past experience, the end of a co-branding partnership does not significantly impact customer behavior or spending patterns.

Credit Quality of BFL Customers

- The collection efficiency of BFL customers has been under pressure following the transition of collection responsibilities from BFL to RBL Bank, as mandated by the RBI.

- This was reflected in RBL’s Q2 results. The bank’s mgmt. expects normalization within 2–3 months.

Reason for BFL Ending the Partnership

- According to RBL’s management, BFL might be exiting this vertical as sourcing cards under the new regulatory framework might no longer be lucrative.Though they didn’t categorically say so.

- They hinted that BFL might also terminate its other co-branding partnerships (they seem tp have one with DBS Bank).

- Given the current environment, RBL does not intend to grow its card issuance beyond 1 lakh per month.

PS - Though reducing in proportion, BFL cobranded cards are still 50% of bank’s credit card AUM. Growth in RBL’s credit card vertical has been flat (1.4% qoq book growth for last 2 quarters) and this will impact it further.

My personal view is that this might need to get priced in, but post that bank not depending on BFL to such a large extent, will likely turn out to be a positive thing. For now there are other things related to how overall MFI/CC asset quality trends to watch out for.

Disc: Invested

1 Like

Bajaj also has a tie up for credit cards with other banks like IndusInd Tiger. No other banks are exiting the tieups for now, atleast.

Bajaj finance business is such that it can still run business profitably with higher NPA and lower RBI norms since it is not a bank. RBL cannot afford the same.

Alternatively, we also need to consider that Mahindra group owns 5% and recently announced partnership for m&m financial credit cards. The Bajaj-rbl breakup can be majorly due to mahindras entry. Although, the bank also has partnerships with TVS and Bank Bazaar. Remains to be seen if they continue of break other partnerships too.

Cancelling profit sharing partnerships can also mean better profits if sales is not a priority right now.

PS: RBL credit cards are not exactly lucrative or customer friendly. The credit card vertical needs a total overhaul to even stay competitive for now.

1 Like

Update: Bajaj has also exited the tie up with DBS.

Also, IndusInd seems to not issuing new Tiger cards.

RBLs current value seems to be waiting for the bank to set its house in order before it rerates.