So you mean to say a person who single-handedly pivoted the business to over 50% earnings growth (CAGR) is bad at business management? His family issues are no new surprise, a similar sell-off was seen when father and son brawled publicly. Very poor family man but a Great business man for sure and he isn’t the only one at the top level management, right?

No, I meant desperate times and mgmt will do things that will impact the business beyond imagination. Remember Satyam?

1 Like

The PE is not adjusted for other income of a Q. It would be like at 18/20 PE after adjusting

1 Like

Yup, but that isn’t how it always works. Let’s see how the market likes it—adjusted or non-adjusted in the coming days. For now, there are multiple factors to consider before we completely eliminate the other income and don’t forget that the median PE i mentioned is also other income adjusted…what did the other income do? Made the company net debt-free 2 years before anticipated, cut free from the FMCG business which was anyway anchoring things down. I understand that this isn’t a high-speed grower any more reason why it always trades at a discount but this discount is a little too much as per my understanding when companies like Vedant Fashions, Trent etc… trade at a PE of 80,178 then a PE of 7(20) is a little too low for a business with a recall value like Raymond and an amazingly well doing real estate business.

The stock was anyways in an upmove setting new highs before all this mess happened. let’s see how things roll…

Disclosure - Now Invested

2 Likes

If governance goes up Debt gets retired, the brand is strong and does deserve better multiple.

Also the true unlocking of RE business has not happened as yet

Realty business going strong!

Why do they need to create so many real estate subsidiary companies? Are there tax advantages?

Not sure about the timelines of this case and payments made by Gautam Singhania / Raymond group

If it were true, was this ever disclosed to the exchange by the company?

Not sure if this will turn out to be a good news soon OR going to be an overhang if the tussle gets prolonged

1 Like

Any views on the post de-merger valuation of Raymond Ltd & Raymond Lifestyle?

Raymond Ltd will have Realty business, along with the land bank & 66% of the merged engineering business “newco” (post completion of Maini precision acquisition). Realty division will have EBITDA of about 300 Crores in current fiscal. Engineering business will have EBITDA of about 220 crores.

Raymond Lifestyle will have 1100 crores EBITDA

Raymond Ltd will have good growth mainly due to realty division

Raymond Lifestyle will have a modest growth I suppose (have to watch how Ethnix scales up). A positive point is that they will be net surplus cash as this entity received the FMCG sale funds

Appreciate inputs on how to value the above two companies, thanks

2 Likes

I am also tracking the demerger news. afaik , they are waiting for approval from NCLT and demerger agm will be held on 28 feb 2024. dont want to miss demerger opportunity like mirza and redtape . However the only difference is the cyclicality of raymonds lifestyle

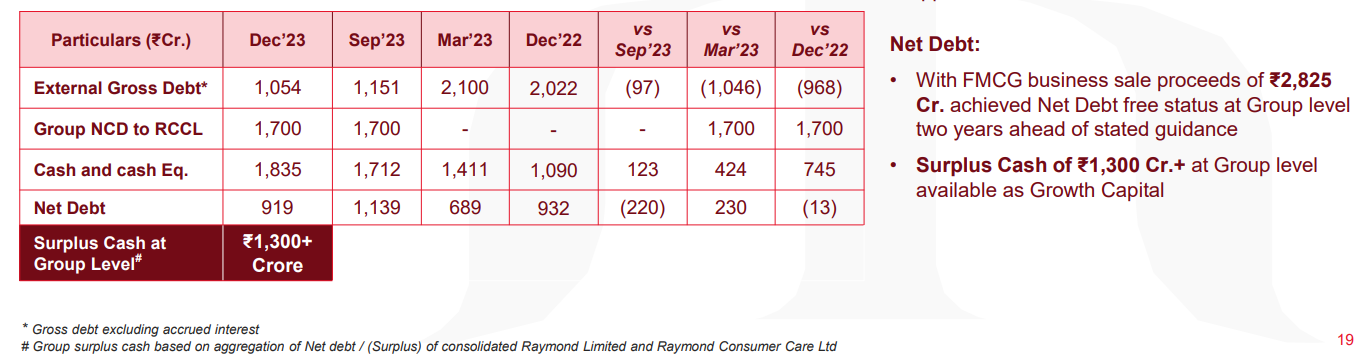

though they have been saying the company is debt free, why are they paying almost rs 400cr interest per year? I have tried to understand their complicated scheme of arrangements, but not clear why isnt the debt reduced as they claim. And was the JK house built really out of company’s cash, and it is more like chairman’s and family residence? that really shows the governance in poor light…

1 Like

They are not “debt free” but “net debt free” (have more cash than the debt)

Please see details from investor presentation

Page 16:

Interest on Group NCD’s issued in Q1FY24 to RCCL for ₹1,700 Cr

This is intra-group NCD and interest outgo will get reversed post demerger (I guess this will boost profits in the next fiscal)

^ Q3FY24 and 9MFY24: Includes interest on lease liability, unamortized transaction cost for external loan prepayment through RCCL NCD proceed

Page 19:

1 Like

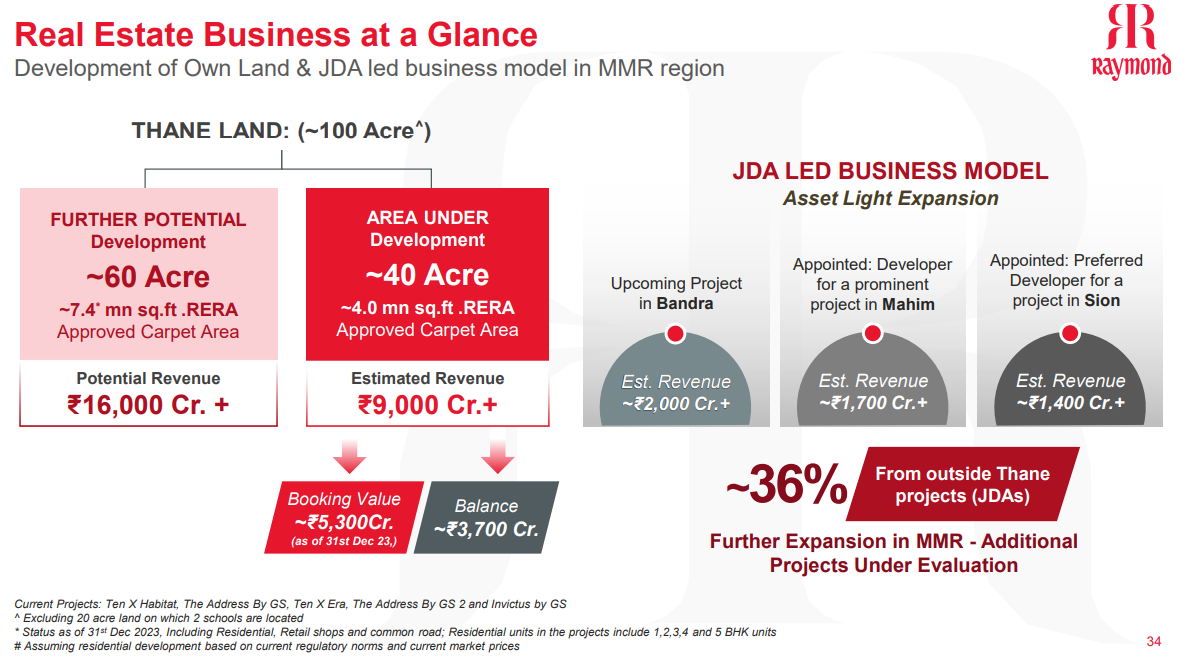

Raymond Ltd has a total of 120 acres in Thane, the split of which as below

a. 20 acres where school is located

b. 40 acres where projects are under construction

c. 60 acres of prime residential area where projects are not planned yet

Does anyone know the land value of these 60 acres in Thane where they are located?

2 Likes

Interestingly, comparing it to Vedant fashion (sorry, may not be apple to apple), the lifystyle apparel business of Raymond(I have extrapolated from avalaible last 2-3 qrtr) does a 3.7cr per store compared to Vedant fashion. However the profitibility looks way different. for any investor , its important that the business is disciplined , efficient, and and generates returns and has simple balance sheet structure.

| Apparel_revenue_Cr | Apparel_EBITDA | No_of_stores | Per_store_AR_cr | Per_store_OP_cr | |

|---|---|---|---|---|---|

| Raymond | 5500 | 850 | 1500 | 3.7 | 0.6 |

| Vedant | 1350 | 655 | 670 | 2.0 | 1.0 |

Also, there was a question in last concall about the ebitda of real eastate business. The management answer was, around 25%, considering it builds on its own land and at an avg rs 20k a sqrft, its too low , compared to something like Oberoy Realty which does EBITDA of 50%

Even though it looks undervalued, but in my opinion economics and efficiency of the company is subpar …I hope restructuring and reorganaising playout, however, from the call it didnt sound like the company is emerging stronger very soon.

Raymond Realty has launched its first JDA project

1 Like