Few articles based on Jefferies’ buy; target price / valuation etc. Since then Raymond is down by more than 10%.

Disc: Invested

Hi,

I haven’t seen many spin offs. I had a question relating the same.

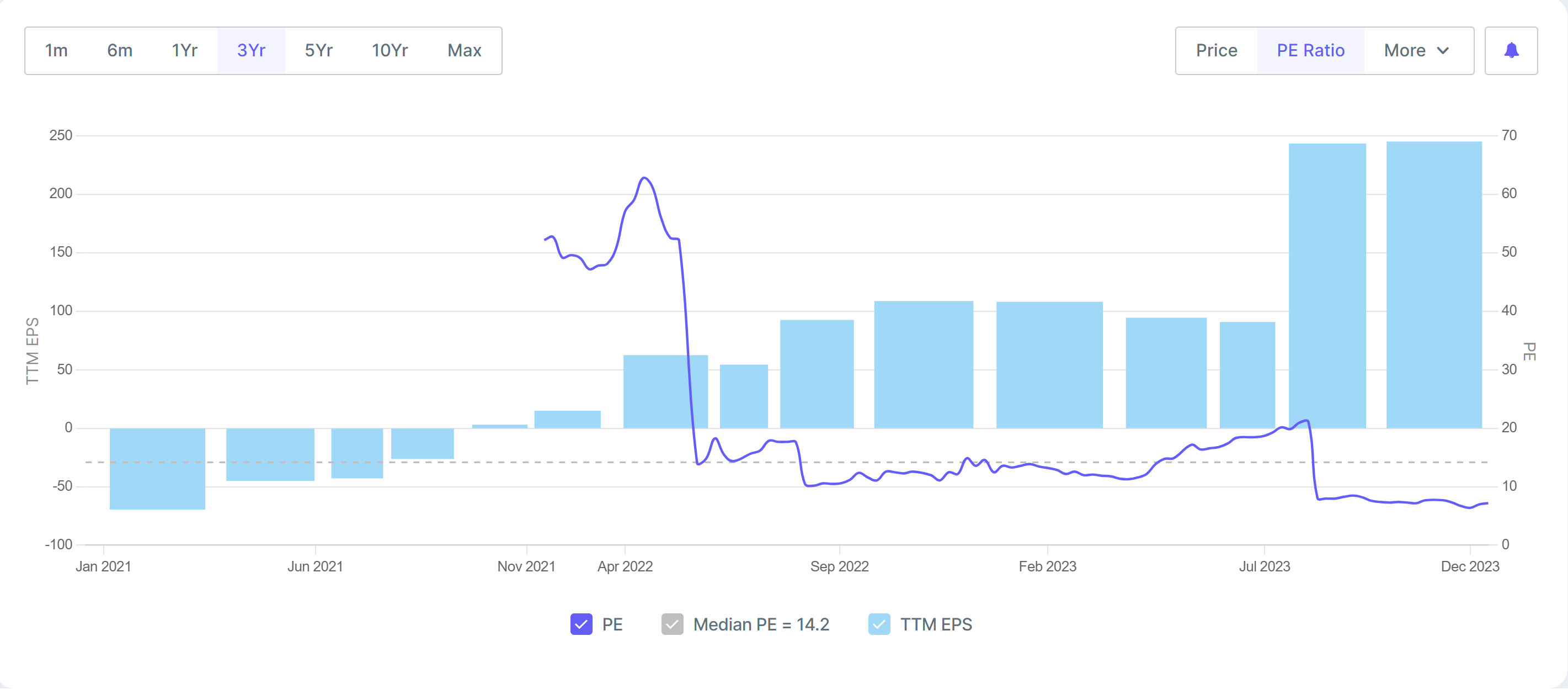

Observation. TTM P/E for Raymonds is 9, removing the 1000 Cr cash because of sale of biz. So roughly TTM PE should be 18-20. I was checking the Industry media PE for both Fashion brands and Realty cos. Both have a aprrox median PE of 30+ So ideally the valuation multiples of both separate entities would rise to industry median figures.

Does this re-rating happen usually post spin off or could happen before too?

1 Like

the new valution adjustment starts getting reflected after record date of spin off is annouced… that is my observation…

1 Like

About the PE for fashion brands

-

Companies like Trent & Aditya Birla Fashion keep acquiring new brands and keep growing them. Trent is particularly good at it and has very high PE, AB not that much

-

Companies like Vedant Fashion is focusing on particular segment and goes very deep in it (wedding and festivity ethnic collections like Manyavar). Margins are very high in this and hence commands high PE

-

Raymond has a mixed business on the lifestyle vertical

a. Core textile business

b. Few own brands (Raymond, Colorplus etc) and doesn’t add anything new (or add very rarely)

c. As mentioned above, the new brand they added is Ethnix and want to grow it like Manyavar of Vedant

How do you compare Raymond life style with that of companies mentioned above?

That’s a fair observation. And I’m a novice maybe I’m wrong but I’ll try to explain better what I meant by the comparison my facts may be a little off but just sharing my rationale

- Companies like Trent & Aditya Birla Fashion keep acquiring new brands and keep growing them. Trent is particularly good at it and has very high PE, AB not that much

- Trend PE is 165 & ABFRL is a loss making company, hasn’t posted a profit in the last 4 years. I don’t know how to judge if a company is fairly valued when it’s loss making and to be honest tracked it at all

- Companies like Vedant Fashion is focusing on particular segment and goes very deep in it (wedding and festivity ethnic collections like Manyavar). Margins are very high in this and hence commands high PE

- Agreed Vedant Fashion is a great company shows from their profit margins and ROCE and maybe a multibagger in the making but capital is finite and I wouldn’t be interested in Vedant Fashion at these valuations

- Raymond has a mixed business on the lifestyle vertical

a. Core textile business

b. Few own brands (Raymond, Colorplus etc) and doesn’t add anything new (or add very rarely)

c. As mentioned above, the new brand they added is Ethnix and want to grow it like Manyavar of Vedant

- In one of the interviews the CFO of Raymond mentioned that in every wedding at least 1 Raymond suit is used (Not quoting paraphrasing). That to me highlights the power of this brand. In spite of having such a strong brand they never killed it because of governance issues which also lead to too much debt and looks like both are resolved.

- Looks like management is getting aggressive in their approach they plan to get 500 new franchisee outlets. And moving from asset heavy to assets light model for expanding their footprint.

- Ethnix looks like a great expansion. Every year we hear this wedding season will be the biggest we’ve had so far and I believe this trend will go on for another decade the way our population is skewed.

Here’s a list of other branded play with their earning multiples

Redtape - 52x

Go Fashion - 82x

VIP - 84x

Indian Terrain - 57x

- When I talk about Raymonds as a fashion and premiumisation play I don’t mean to compare it with the MANYAVARs of the world and hence not looking for a 70-80x earning multiple but a reasonable 30x won’t be too much to ask for considering their brand recall and their distribution.

2 Likes

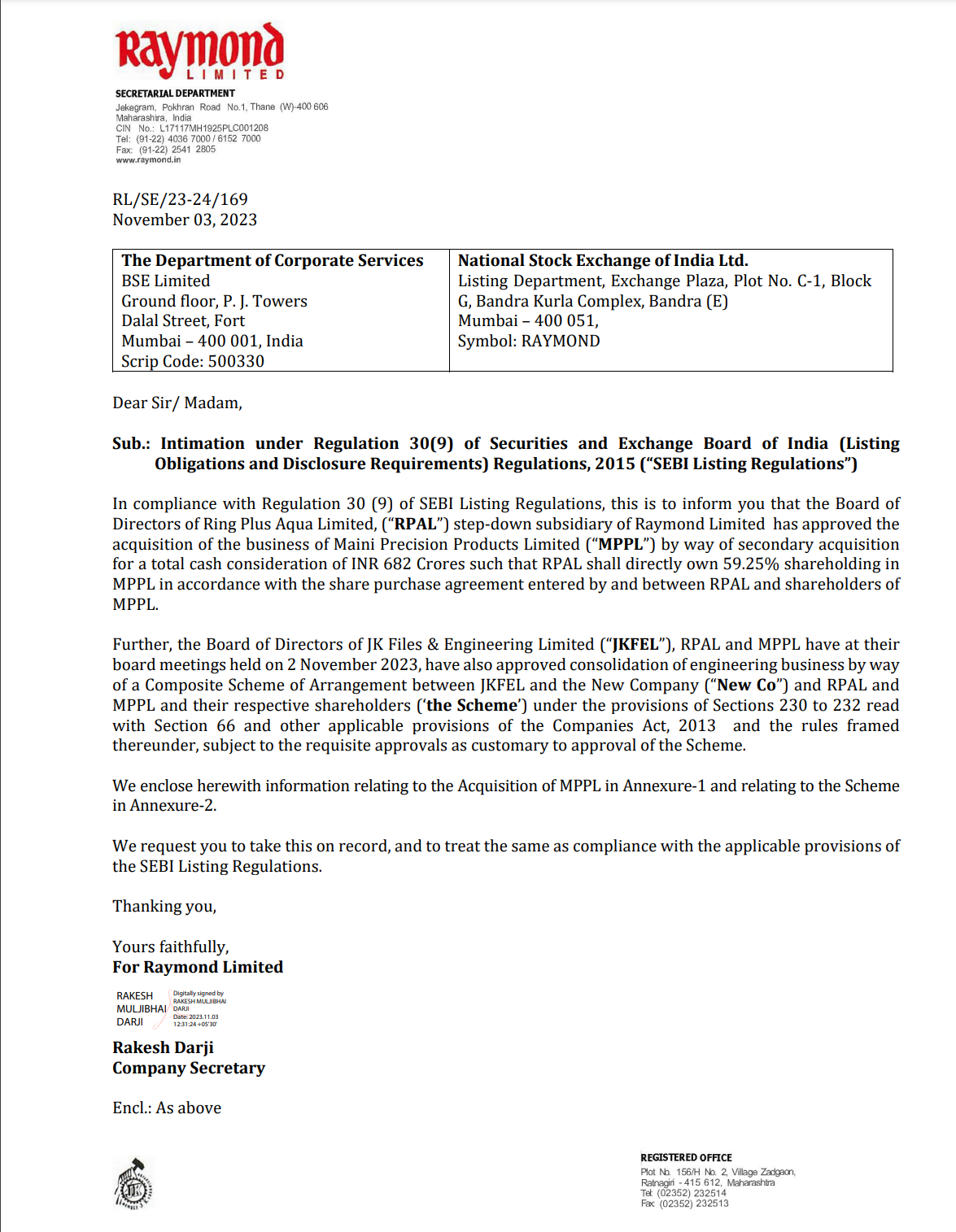

Raymond Limited is informing these regulatory bodies about certain business decisions made by the company.

Here’s a simplified explanation:

- Raymond Limited is a company in India, and they are writing this letter to inform the stock exchanges about two important decisions they’ve made.

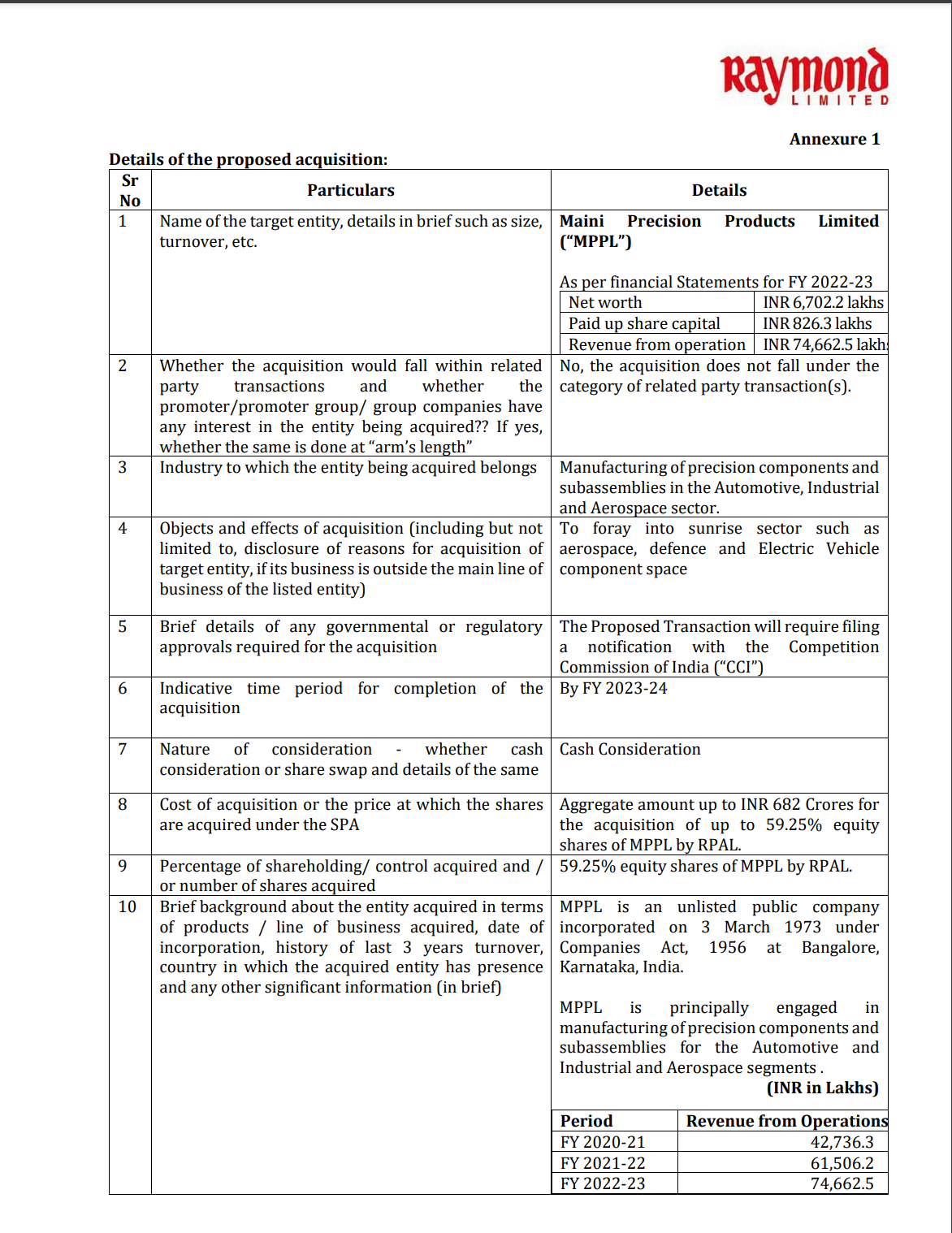

- The first decision is about a company called Ring Plus Aqua Limited (RPAL), which is a subsidiary of Raymond Limited. RPAL is going to buy another company called Maini Precision Products Limited (MPPL) for a total price of INR 682 Crores (Indian currency). This means RPAL will own 59.25% of MPPL.

- The second decision involves three companies: JK Files & Engineering Limited (JKFEL), RPAL, and MPPL. They are planning to combine their engineering businesses into a new company, and this process is called a “Composite Scheme of Arrangement.” It requires certain approvals.

- The letter provides details about the acquisition of MPPL in Annexure-1, including information about MPPL’s financials and the reasons for the acquisition.

- Annexure-2 provides details about the Composite Scheme, including the entities involved, the division to be demerged, and the reasons for this restructuring.

In simple terms, that Raymond Limited is making some big changes in its business by acquiring another company and restructuring its engineering business.

1 Like

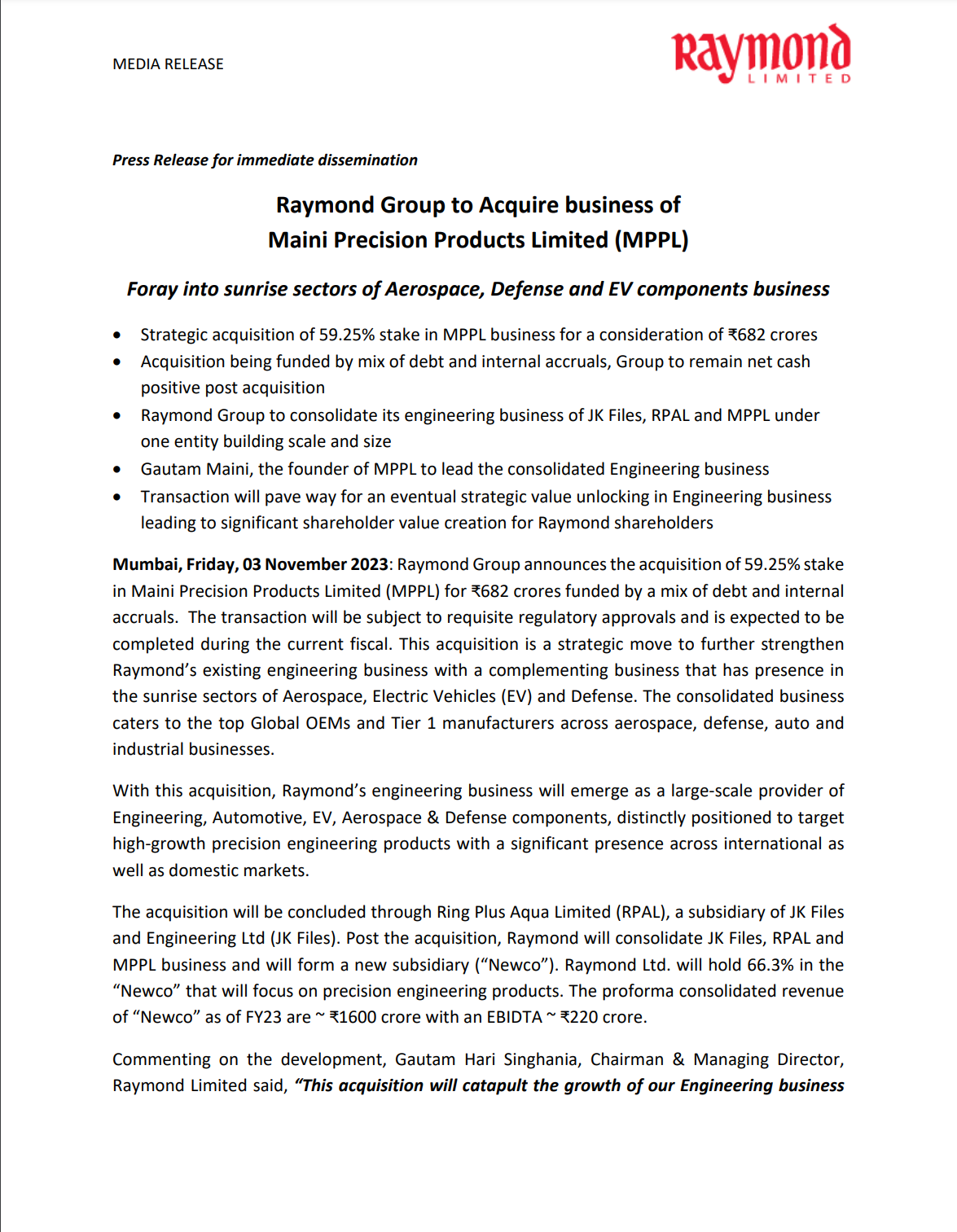

Raymond Limited notified about two important updates:

- They’re buying a 59.25% stake in another company called Maini Precision Products Limited (MPPL) for ₹682 crores. They’re using a mix of debt and their own money to pay for it. This will help them expand into growing areas like Aerospace, Defense, and Electric Vehicles (EV).

- They’re reorganizing their engineering businesses by combining them into a new company. This new company will focus on precision engineering products, and Raymond Limited will own 66.3% of it.

This is a strategic move to grow their engineering business and enter new, promising industries. They’re excited about the opportunities this will bring. The acquisition will be subject to regulatory approvals and should be completed soon.

5 Likes

Hi - Can anyone share how they are sensing Raymond vis a vis other fashion brands on the ground? I looked up Amazon, and that does not show good reviews/traction - this was for ethnix by Raymond - the brand they are banking on as growth driver.

If theres anyone from Mumbai, can you share thoughts on Raymond launches? What’s the market pulse? Though it says 80%+ inventory sold, is this being sold at discount given its a new entrant? If not, why are people choosing Raymond over other established real estate players?

Thanks in advance

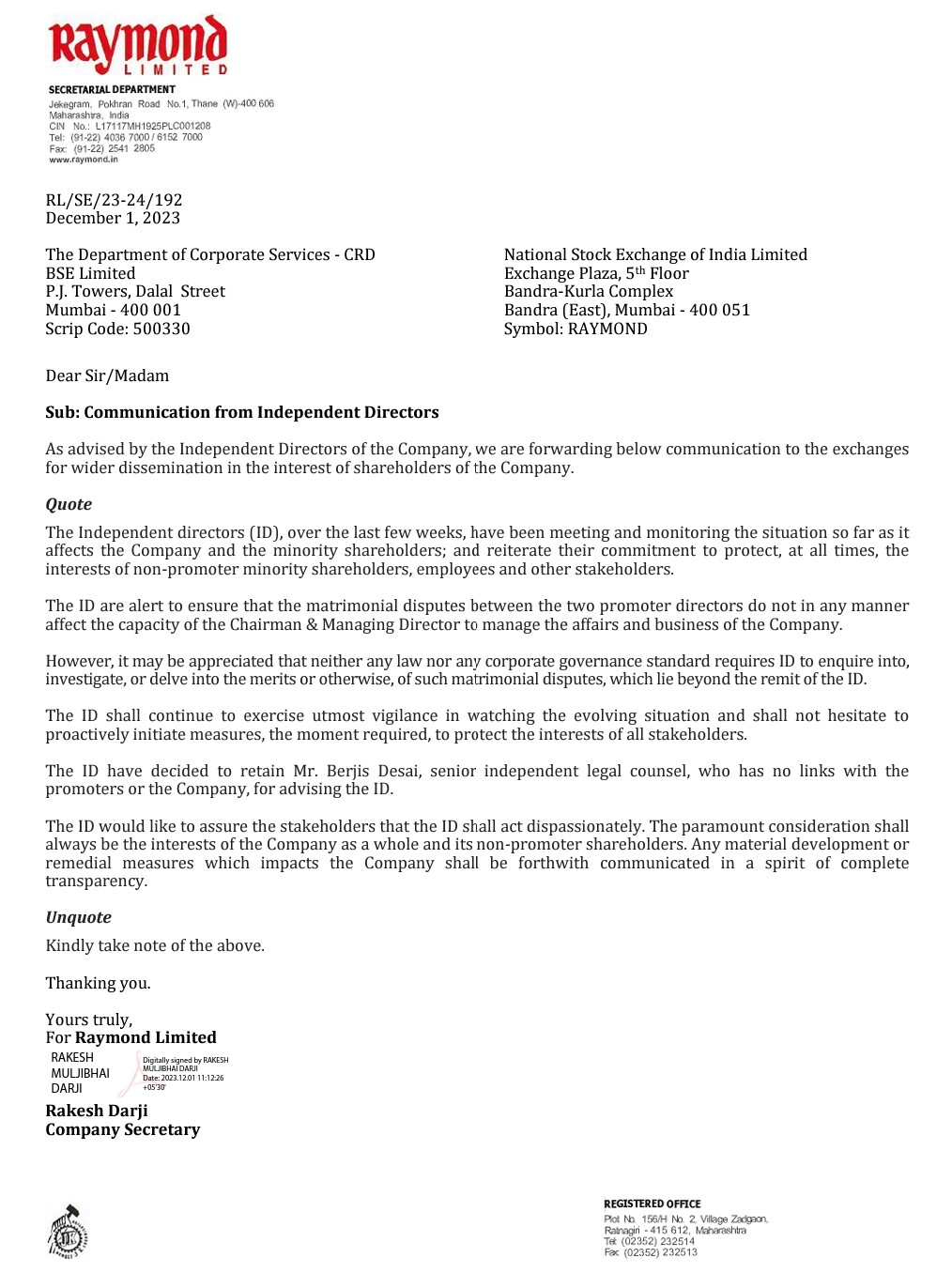

Are the ongoing personal issues of Gautam Singhania going to impact the business in any form, given that his wife is also a board member and is seeking a major share of his wealth, which I guess would also involve shares of Raymond in an indirect way?

I noticed this article today. Didn’t subscribe to read the content as it could just be speculative.

1 Like

The company is doing too much of things. Sale of one business division, acquisition of another company, jumping into real estate earlier. Plus now all this family feuds.

It seems more like instead of core business management, they are focusing on everything else plus distractions/ corp governance issues, media attention inviting things too much.

I may be wrong but I have booked loss and came out

Their core business was textiles. Diversifying the business is not a bad thing given the fact that the company is almost 100 years old and diversification is necessary.

Creating separate companies (lifestyle, real estate and engineering), each with its own management (and that too by professionals and not just family) brings focus

Textiles to real estate may sound odd but the trigger for that is the land bank they have. They could have just sold the land and taken the money and distributed it as dividends or invest further in core textile business. But they saw it as an opportunity to diversify and grow which seems to be working with the revenues they are generating

The latest acquisition of Maini precision looks little aggressive but it clearly shows that they want to de-merge engineering business as a separate entity and want to grow it

7 Likes

Textiles and apparels have many new areas in themselves like fast fashion and others to crack. The focus might have gone there instead of completely different businesses.

Further, for me so much of churning in business model is a big no no. Plus corp governance issues with all the complications happening on promoters front also a big challenge. Many easy opportunities available in the market.

Real estate is the only new business they have ventured into off-late. Engineering business is something they have for a long time. If you see the history, they have tried few other businesses like steel etc and have come out of it.

Family issues are concerning but there have been no major corporate governance issues for past few years. Bringing in outside (family) professionals to run different entities was a good move in improving corp governance. They have been very transparent since past few years

2 Likes

I also had this guy feeling from whatever I read in interviews of the involved parties (that Ambni’s may be fishing in troubled waters or may be troubled itself fuelled by them.

Raymond’s is doing wonderfully well under GS…He himself invested back his share of money received from consumer deal by subscribing to equity at market price.

Iets see if GS will overcome this tide. I feel he will

1 Like

1 Like

Textiles and apparels have many new areas in themselves like fast fashion and others to crack.

They tried apparel (Parx, Park Avenue, Color Plus).

But issue is lack of focus from promoter front and old lala culture.

lack of focus from promoter

GAUTAM SINGHANIYA was a playboy and a social animal like his father. He never took great interest in business. He once even said that everything is for sale as long as offer is good. (context is apparel / textile division).

He has 2 daughter and they are in teens. So they won’t be joining management anytime soon.

old lala culture

They have brought outside professional to run as CEO but they never replaced the middle management.

So, many time, good initiative never gets IMPLEMENTED. Most of the newly introduced feature never reaches the end customer / retailer. Middle management is still stuck in old thinking and all they care about themselves and their sales target.

Disclaimer - I am Raymond authorized retailer for last 16 years and I am selling Raymond Suiting since last 30 years.

11 Likes

No objection to the proposed Scheme of demerger from BSE and NSE. Now, company will file application with NCLT.

2 Likes

Do family issues impact earnings growth?

Will it stop people from buying Raymond?

Will it increase the debt?

Will it hinder day-to-day operations?

Will it cause any monetary loss to the company, apart from a few shareholding pattern changes?

If the answer to most of these questions is a NO then why trade at a 7-odd PE when the company’s median PE is 12-14?

I don’t think this low valuation will sustain for long.

Heard mentality sometimes does present good opportunities.

Never under estimate the ability of bad management to ground a good business ![]()

3 Likes