Expecting JDA launch in FY24 after approvals

It seems JDA which is redevelopment project which is being done with CRD group in East Bandra along Western expressway under MAHDA.

PS: Check out Capacite Infra also it seems it offers good value at current levels (There was an unnecessary derating from rating agency which caused fall)

Ethnix rollout going as per plan 59th store done

The 59th flagship store of Ethnix By Raymond is now in Chennai's Pondy Bazaar. Spread across 3000 sq ft, the store offers an impeccable range of ethnic wear embodying the best of design and craftsmanship. pic.twitter.com/F4mu6g661t

Raymond Realty completely dominating in the region and segment in which they operate. It even excludes the Pre Bookings that have happened in Ten X Era as their registrations must have not taken place yet.

Also today there is a press conference at 3.30 PM. I am expecting this deal and maybe some other things which can be good triggers to be announced.

Stock has already run up but still it is an undertracked and undervalued company.

Along with the deal, they are restructuring the business (not sure how to look at it)

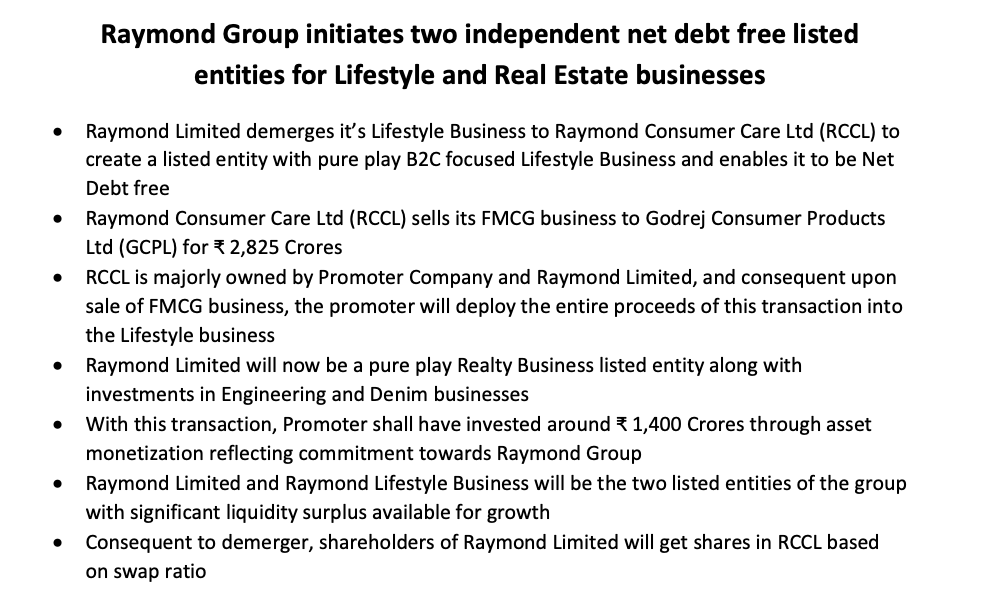

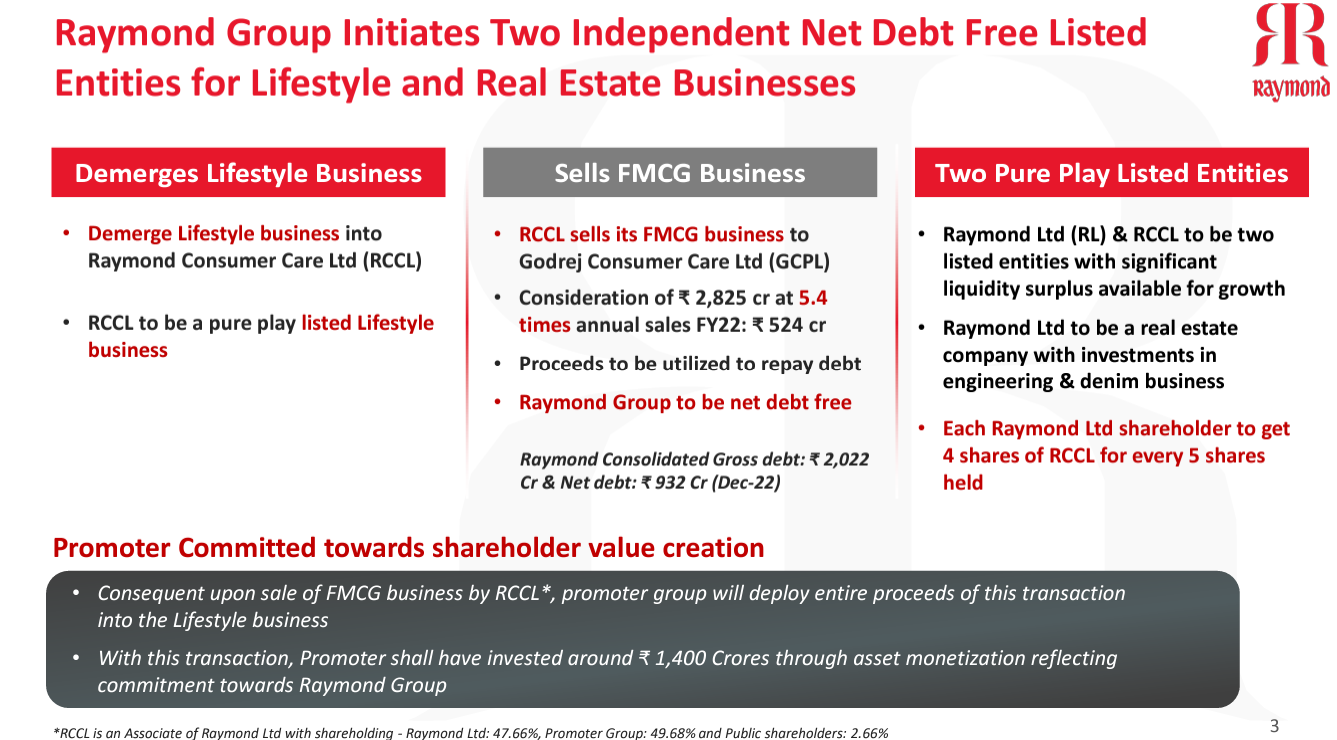

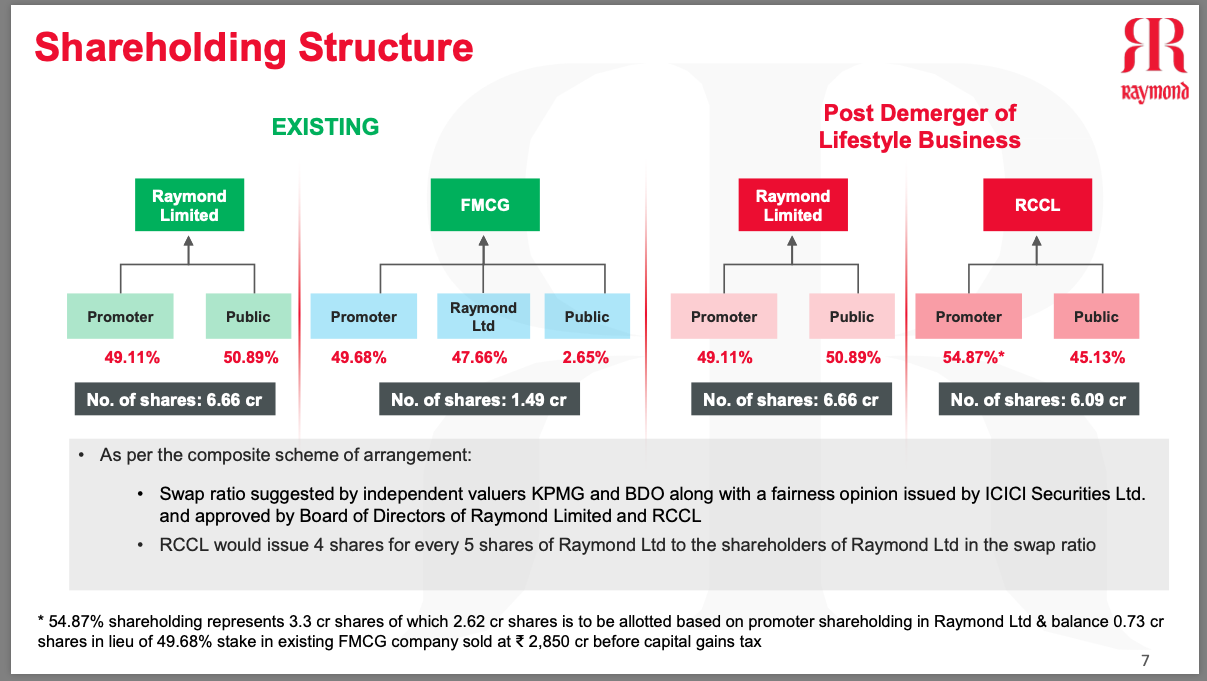

Raymond Consumer Care Ltd is an associate of Raymond Ltd (where Raymond Ltd holds 48% and Singhania family holds 52%)

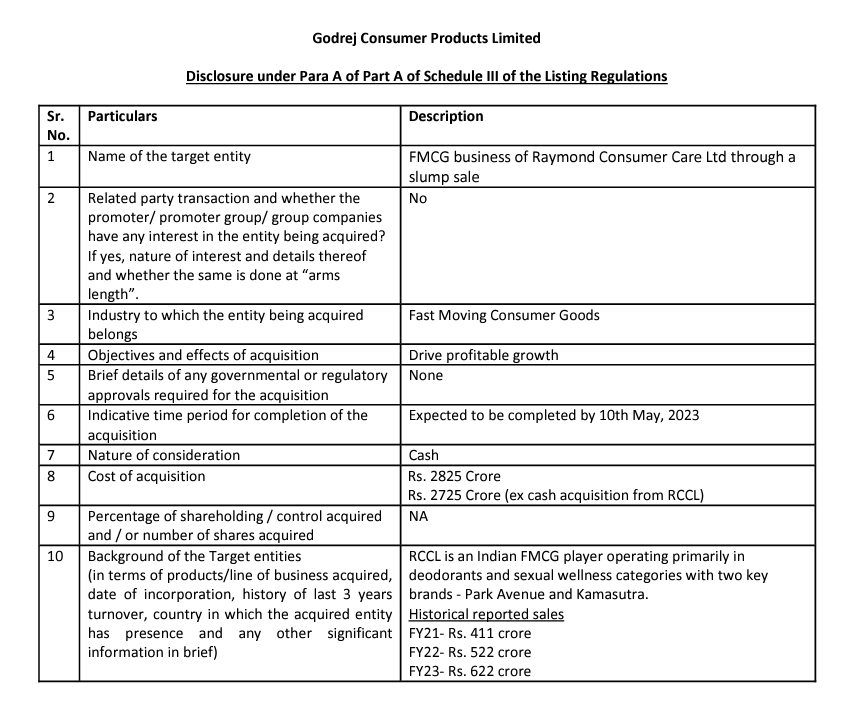

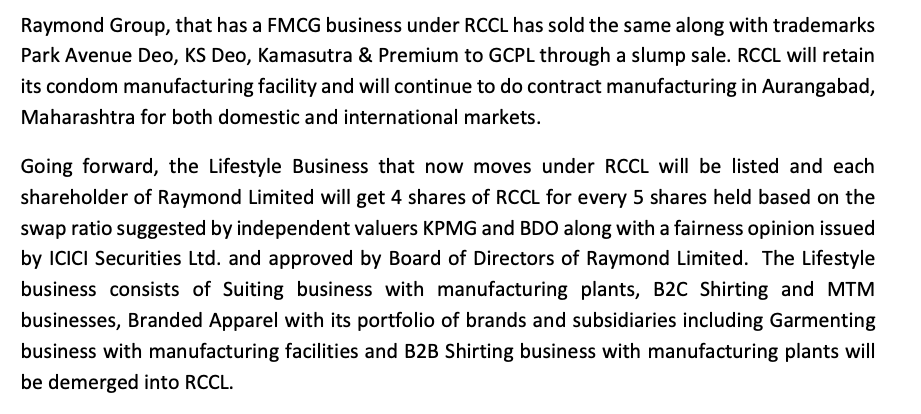

Raymond Consumer Care houses the FMCG business, most of which is being sold to Godrej Consumer Products Limited for 2800 Crores

Raymond Ltd will demerge it’s entire lifestyle business into Raymond Consumer Care Ltd and will list it as a separate entity (the new entity will be (net) debt free with the money coming in from Godrej Consumer Products)

Shareholders of Raymond Ltd (the current listed company) will get 4 shares of the new to be listed company Raymond Consumer Care (4 shares of Raymond Consumer for 5 shares of Raymond Ltd)

Raymond Ltd will become primarily a real estate company with investments in Engineering & Denim business (and will be debt free)

Experts - please share your views on how you see this and if this is beneficial for us investors

Management is also under compliance they cannot talk too much. Q4 results will be announced in around 10-12 days expect some great in depth presentation. We will have to wait.

Till then Enjoy the Gains

its a demeger we have been waiting for … we get 4 additional shares of Raymond textile business for ever 5 shares of Raymond which will become purely Real estate company…that is what i understood…

Any details of following queries will be highly appreciated:

1).What will be the Shareholding solit of RCCL

( promoters and public) post this restructuring excercise is completed?

2). What is the rationale of 4 shares of RCCL for 5 shares of Raymonds? Shouldn’t it be 1:1? Since promoters already hold 52 % in RCCL wouldn’t it dilute the public shareholding?

Note: i haven’t done any calculations. These are just queries in case some fellow members have already done it.

since promoter are putting proceeds of sale in RCCL their shareholding will increase against new shares unless there is some other structure. Which means promoter shareholding will increase and public shareholding will be lower in RCCL

I would assume that new shares in RCCL will be issued to promoter at valuation arrived at for demerger.

the swap ratio of 4:5 would have been arrived at after considering the increase in shareholding of promoter post infusion of money in RCCL

Swap ratio suggested by independent valuers KPMG and BDO along with a fairness opinion issued by ICICI Securities Ltd. and approved by Board of Directors of Raymond Limited and RCCL

54.87% shareholding represents 3.3 cr shares of which 2.62 cr shares is to be allotted based on promoter shareholding in Raymond Ltd & balance 0.73 cr shares in lieu of 49.68% stake in existing FMCG company sold at ₹ 2,850 cr before capital gains tax

Can anyone clarify how 2850 crores that FMCG business gets is going into RCCL?

FMCG is currently owned 50% by promoter group (mostly Singhania family) and other 50% by Raymond Ltd & small public holding

Post deal & before de-merger:

FMCG entity has 2850 crores, of which half goes to promoter group and rest mostly belongs to Raymond Ltd, which includes us - shareholders too

Post de-merger:

Raymond Ltd transfers lifestyle business into FMCG entity (called RCCL), for which all shareholders get 4 shares of RCCL for every 5 shares of Raymond Ltd (us, public shareholders and promoter group)

Promoter family retains their share in FMCG / RCCL

In the press conference, GS mentioned that promoter family is fully investing their share of 2850 crores into RCCL. If that’s the case, will RCCL get the full 2850 crores and thus even the gross debt of 2022 crores gets paid off and the remaining few hundreds of crores remains in RCCL books?

They said they will fully invested from their share of FMCG sell. Not Rs.2850crs. Even they said so in total they are investing Rs.1400 crs in the company. That includes Rs.350crs from the sell of the land in 2019 or so

My conclusion from their latest presentation:

After Tax they will receive approx. Rs.2200 crs for FMCG. Considering promoter stake of 49.68% it comes around Rs.1095crs to promoters. they have issued 0.73 crs shares of Raymond Consumer care against the same amount . so it comes around 1490 Rs per share.

please correct me if i am wrong in my understanding for the same.

The latest presentation gives a slightly better picture. From the sale to Godrej, the post tax realization is 2200 Crores. The promoter family is not cashing out, neither does Raymond ltd and hence the entire 2200 crores stays in the books of RCCL.

Raymond Ltd has a gross debt of 2000 crores and net debt of 932 crores as on Dec 2022. When the lifestyle business is de-merged into RCCL, am not sure how much of the gross and net debt will move from Raymond Ltd to RCCL.

The presentation says the overall Raymond group (Both Raymond Ltd & RCCL) will remain NET debt free and cash surplus of 1300 crores. I am not a finance expert but if they intend to pay off the debt, they should not mention the term NET DEBT FREE but should just mention as DEBT FREE, isn’t it?

I assume that if they don’t pay of the debt, then quarterly earnings will have an interest cost. Is that correct?

In today’s conference call, CFO indicated that all shareholders of RCCL (promoter group and shareholders of Raymond Ltd) will be allocated shares at the price of Rs. 1450

Does this mean, RCCL with an equity share base of 6.06 crore shares are valued at (6.06 * 1450 = 8787 Crores)?

Raymond Ltd’s market cap on today’s (April 28, 2023) is around 10,590 Crores. Does this mean they value the real estate & engineering business at roughly 1800 crores?

It is not the job of independent valuer. They must have valued the lifestyle business which is getting transferred and cash balance due to FMCG slump sale. Its the implied valuation that we are calculating by subtracting for the rest of business i.e, Raymond Realty + Thane remaining Land Bank + Engineering + one signed JDA of Bandra (2000 crores expected revenue over 5 years) + Raymond UCO Denim (50% JV) +JK House.

Calculations at CMP ~ 1600

RCCL valued at 1450

4 RCCL for every 5 Raymond Ltd

This implies that (5/4)x1600-(1450)=550 550 rupees per share or 3663 crores is the value assigned by market at CMP to these assests.