A detailed article on the demerger transaction. Check it out - Raymond to follow the industry trend by hiving-off Core business

What happened to the demerger. Wasn’t it supposed to get completed by April 1st 2020?

Concall highlights

Company has launched customer initiatives such as Tailoring subscription program, Garment Exchange program - which witnessed good response from customers post Pan India launch in TRS network

Raymond has also recently launched an anti-viral technology based fabric -VIRASAFE which protects against bacteria and virus and is also anti-odor & sustainable

They have enhanced omni-channel capabilities by bringing entire EBO offerings online, revamp own website ‘myraymond.com’, moving from physical trade show to digital platforms, strengthening 3rd party tie-ups and such other initiatives launched to help driving sales

In Tools & Hardware business, Raymond resumed their production in May in order to

cater to its pending exports orders. Currently, the business is at ~95% of Pre-Covid-19 levels.

Auto Components business is clocking ~90% of revenue of Pre-Covid-19 levels primarily

led by revival in domestic market.

Real Estate - Till date, the company has already received bookings of 963 flats (60% of total inventory of ~1530 units) with booking value of INR 9.7bn. In 1QFY21, total bookings were to the tune of 13 flats. The company has completed construction of 6 slabs for 3 towers as on date. The company is engaged with potential buyers through video & audio calls and also providing virtual tour of the project & sample flats and has been able to convert few customers

The FMCG business under ‘Raymond Care initiative’ has launched a range of sanitizing

products including hand cleansers, hand wash, high alcohol content cologne along with

floor wash meeting the highest safety standards, affordability and ease of usage for consumers.

By June end, 80% of 1332 stores had reopened.

Till date, the management has confirmed full year rental savings of INR 480mn; of which

INR 174mn was booked in 1QFY21.

Net Working Capital reduced by INR 3.05bn to INR INR 15.5bn primarily led by collections from receivables.

Raymond issued NCDs worth INR 1.45bn during the quarter.

Net Debt at INR18.27bn was marginally lower than March’20 levels at INR 18.59bn with Net Debt/ Equity ratio at 0.8x in June’20.

1 Like

Has the record date been fixed for the demerger or can one start accumulating at this point?

In FY21 annual report it is mentioned that ratio of short term debt/long term debt improved significantly.

“FY 2020-21 witnessed a major change in the

consolidated debt structure of the Company. The short term debt to long term debt as a percentage of

net debt improved from 79:21 as on March 31, 2020 to 17:83 as on March 31, 2021 with long term debt having 3-10 year maturities”

Same is visible in the balance sheet. But what could be the rationale of such a move ?

- Is it because long term debt costs less than long term debt ?

- Or is it an attempt to move bulk of the debt to the Non textile arm during demerger ?

1 Like

“Each shareholder of Raymond will be issued shares of Raymond Lifestyle in 1:1 ratio, in consideration for the demerger, and Raymond Lifestyle will be listed, with its shareholding mirroring that of Raymond. Of the total consolidated debt at Raymond (excluding Raymond UCO), about 75% of debt and 60% of cash and liquid investments will be transferred to Raymond Lifestyle.”

so majority of debt is going to be pushed on the “to be listed” Raymond Lifestyle entity as per Crisil…

1 Like

@Ysr - As per today’s notification, i see demerger plan has been withdrawn. I might be wrong but this is what i see.

"In order to enable and execute the above decisions, the company has withdrawn the de‐merger scheme of Lifestyle business announced in November, 2019. These actions will enable each of the businesses for monetization which will fuel growth and deleveraging. "

2 Likes

so is the idea now to sell off the non core business ie power tools, files, engineering ?

seems like this is a good idea on the surface…

Yes to monetize. Infact the engineering business itself worth the total market capbof the company. So essentially you sre getting fmcg, b2c brand business and real estate Close to for nothing. Huge value on table.

Disc - 15% of my portfolio. (Special situation category investment)

2 Likes

Old Demerger Plan Cancelled ???

Seems like you arw a new member here. Please read entire thread before asking questions. Redundant questions are poor reading experience for members.

2 Likes

Good Q2 results. In a 100% covid-free time, the topline and margins will be even better. (Stock price is not reflecting it though). Hope they come out with a clear monetization plan with timelines

There are many news about Raymond now a days. The latest one is as below

JK Files (India) IPO: Raymond Group plans to soon list JK Files - The Economic Time

It seems Engineering business needs to be listed separately via IPO

Is this IPO differ from Demerger?

What is the benefit for existing retail shareholders?

Thanks

Hi,

There is official announcement of this on BSE and NSE. This will help to reduce debt on the book of Raymond Ltd.

Prashant

We have understood that Raymond balance sheet will be deleveraged, so Raymond will be re-ratated.

Are existing share holders gets any shares from JK Files when JK Files listed in NSE and BSE?

ET now mentioned IPO valuation of around 2000 crores with a 700 crores IPO a few months ago. So it would be in that range I guess. I hope the entire IPO funds are used to reduce debt and not to invest in other divisions. That’s the main advantage for existing shareholders of Raymond as this should re-rate the Raymond group valuations (hopefully)

2 Likes

Thanks for this info  .

.

I too believe the same.

I believe during evaluation of Engineering business, Raymond too would undergo revaluation

1 Like

Raymond (JK Files & Engineering) has filed its red herring prospectus for IPO (OFS) of 800 crores

Total equity shares: 5.2 Crore shares. As it’s OFS, this will remain the same post IPO

H2 FY22 financials:

Consolidated Revenue : 399 Crores (Source: Q2 Investor presentation)

EBITDA : 58 Crores (Source: Q2 Investor presentation)

Net profit (approx) : 37 Crores (Source Q1 NP 17 Crores from prospectus, Q2 is own calculation)

On an annualized basis, we can safely assume 80 - 100 Crores net profit.

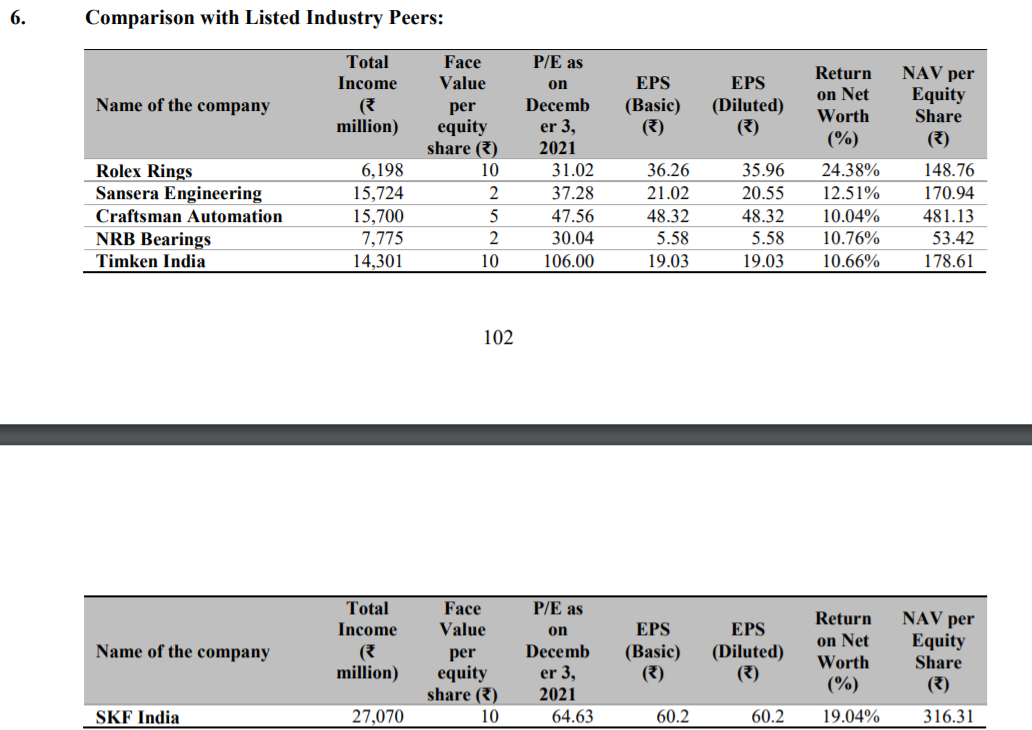

In DHRP, industry valuation comparison is provided as below

If we assume 100 crores profit and a PE of 30, it comes to a valuation of roughly 3000 crores (approx Rs. 600 price per share). Company has negligible debt but I don’t know their current capacity utilization and capex plans. If anyone gets to go through the DHRP in detail, please do share your findings and analysis. Thanks

Thanks for sharing the details. I am trying to read more from the prospectus.

Just a note about revenue and profits:

FY21 was a slow year, hence revenue and profits are low. FY22 H2 revenue is already at 400 crores compared to full year FY21 revenue of 550 crores. For a normal year (and extrapolating H2 numbers to full year),we can expect revenue north of 800 crores and a net profit of more than 75 crores.

1 Like