Raymond is showing decent turnaround with ref to opening new stores and getting rid of laggards. Over all segment wise I see good growth prospects. New Amaravati plant post inauguration will add to its growth overall. Any views!!!

Hello Friends… I have tweeted Gautam Singhania to request him to lead the Earnings Call himself as he is the managing director

Request you to kindly like it/retweet it.

1 Like

Raymond is preparing for the launch of its residential project in Thane. The project is called Raymond Aspire & the project website is up now… It will have 2 BHK and 4 BHK flats.

2 Likes

Can someone please share summary of the article. Its a paid link.

Clarification from raymond

1 Like

Seems like BQ have not done their homework prior to publishing. I feel like it is important to seek clarification from all parties incl. investor relations before publishing such articles, especially if you are a reputed news house.

Such false accusations only cause more harm to retail investors in such companies. However if such allegations are backed by solid data and statements from the required parties, it can be of great help to retail investors. Such articles only create noise and cloud the judgment of small time investors who lack the resources and know how of the bigger instituitions and investors.

Discl: not an investor in Raymond.

Couldn’t agree more. What is surprising is the way they timed their release. Not sure why they brought it now when biggies are going down one by one. Lot of vested interests here. Not possible for a retail investor to separate the wheat from the chaff!

Discl. Small allocation

It will be important to track divestment of its non-core businesses (not land). I think divestment of those businesses will be a big kicker to the company’s future.

@1.5cr News article on splitting businesses in two entities. Usually promoters create such arrangements neglecting minority share holder’s interest and keeping assets/cash to themselves. Is there some indications on fairness to minority shareholders. What is the likely impact of the demerger from shareholders point of view

3 Likes

Important thing to see would be how they structure the group debt. That would be something to consider.

As long as retail have the perception that the father was duped. I doubt we will see much retail particiaption apart from trading on the scrip.

Debt structuring post demerger remains the key thing to watch in my view. In the consolidated entity they had land worth close to entire market cap. (this was being monetised clearly through sales and RE project). They had other auto ancilllary etc: businesses. That was to be hived off as well. So the entire market cap was covered by non-core asset sales (back of the envelope of course). They had debt of approx. 2800cr. So entire debt could be wiped off by non-core asset sales and they would perhaps be left with some surplus as well. In addition to internal cash flows to pay down debt. As of now I cant find any clarity on how debt is going be structured between the entities. Obviously the hope is that the demerged entity has little to no debt.

Senior members/long time investors can throw some more light on this. This is all the half-baked info/insghts I have haha!

2 Likes

Concall notes post the restructuring and dilution.

Front facing, corner land and is a prime piece of land. 20acre sold at good valuation for a mall. Selling such a big piece at these valuations is not easy. Objective was not to dilute, it depends on the demand, buyer requirement. Hence this parcel was sold first.

Total proceeds are 650cr+50cr contingent to some obligations. I2R conversion and other items (brokerage etc) were 200 cr. another 100cr tax. Leaves 350cr, which is being deployed.

Promoter stake will go up from 43.83% to 48.21%. There will be a 10% dilution. Promoter got this stake at Rs 674, the stock has already shot to 800+ post the announcement.

Demerger of lifestyle business. It will pay royalty of Raymond brand (perpetual rights) to existing co in % of revenue OR a fixed number, whichever is lower. Raymond brand will not be owned by promoter in personal capacity, the brand can be used later to expand into other areas. Ex, real estate projects can carry the Raymond brand. Remaining brands- Park avenue, Parx, Colour Plus to be owned by new entity. “These are as per transparent governance best practices in the market eg Tata does it”.

Existing co has potential to be RE company along with auto/hardware. Land bank remains.

-

80acres of land can be 1) developed jointly 2) Sold 3) ….??

-

FMCG stays here so they will have rights to the brand.

-

B2B business- pending case. It belongs to lifestyle ideally but it remains in holdco. When dispute is resolved, it can be transferred. Options such as slump sale will be considered then.

-

UCO denim business was a JV investment, it will remain here. Challenges of excess capacity in industry but we are running at full capacity. Last 3 years cotton shot up 30%, this year we expect it to soften. Outlook is positive because of cotton prices, indigo import. The business is EBITDA positive but not PBT level, it will break even at PBT level.

Debt of 2750cr reduces by 350 cr, Interest saving of 24cr

NET debt will be 2000cr. 65% is WC loan, 35% term

Working capital moves with respective business. Total split will be approx. 75% in lifestyle, 25% with Raymond ltd.

My assessment is that the management has done this in a pretty transparent manner even though many people on call sounded unhappy with parts of the restructuring/transaction. Management has executed what they had promised in last 2-3 years.

2 Likes

http://www.raymond.in/sites/default/files/Embarking%20on%20Transformation%20Journey.pdf

Presentation on demerger etc:

Did they throw any light on why they did not try to push the FMCG business into the demerged entity?

FMCG earlier consisted of 2 companies, JK Helen Curtis and JK Ansell (which was JV with Ansell and the partner stake was bought out) . Integrated these 2 companies now to form Raymond Consumer care, which is a 100% subsidiary of JKIT. In turn, JKIT is an associate company where the Raymond Ltd own 47.6% stake, and 49.3% with promoter.

FMCG Turnover is 650 cr with EBITDA margin of 5.5%. 3 years ago, turnover was 400cr. “Idea is to scale this business, investment happening in new categories in men’s grooming. Further value unlocking opportunity exists and it is clearly in our radar”

1 Like

200cr for conversion & brokerage!? Isn’t this too high? 10cr/acre or 28.6% of transaction value! This must be usage change (industrial to commercial).

Yes that’s what it says. Everything put together was 200cr.

" The company also announced the allotment of 33,38,278 equity shares worth Rs 225 crore and 18,54,599 compulsorily convertible preference shares of Rs 125 crore to JK Investo Trade, an associate company against the infusion of net proceeds of JKIT land sale that was announced in October 2019.

A total of Rs 350 crore will be used to repay the debt, thus deleveraging the Raymond balance-sheet.

The company had received around Rs 700 crore through the land sale.

The infusion of net proceeds of JKIT land sale in Raymond Ltd will help the company in debt reduction."

The above statements are from articles in moneycontrol. As a retail investor my worry is what was the need for equity dilution . The money obtained by selling the land parcel ( 350 crore post transactions and taxes) could have been infused directly into the company for debt reduction. What is the need to issue 225 cr + 125 cr rupees worth shares ( equivalent amount of money infusion ) to JK Investo trade ? As an investor in Raymond company, I feel some percentage of the land deal should have come directly as the company is also a part of holder of the land. Having associate companies with different holding pattern among promoters, shareholders and other partners makes it confusing and not a retail investor friendly governance.

Disclosure : Invested.

The land which is sold was owned by JKIT and the proceeds would go to them. Now if the 350cr post expenses and taxes has to be used, it would have to be given out as a dividend and 47% of this 350cr would have gone to Raymond Ltd, but only after levy of a dividend distribution tax. The remaining amount would have gone to promoters. In my view, given the current structure, they have done the best possible thing to infuse the money in Raymond.

This is a legacy issue which they cant change overnight. But I think management has really done well on all promises made in recent years. There is a clear change in the way management has performed in last 3 years. At which point the market takes note of this is a different issue.

2 Likes

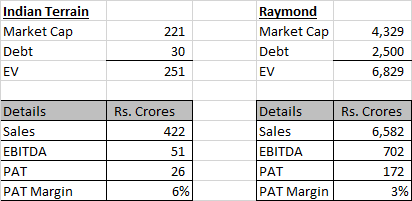

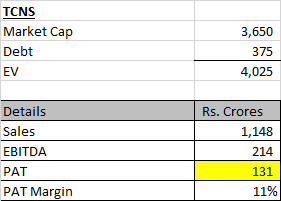

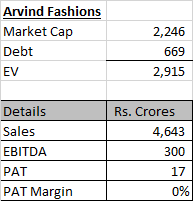

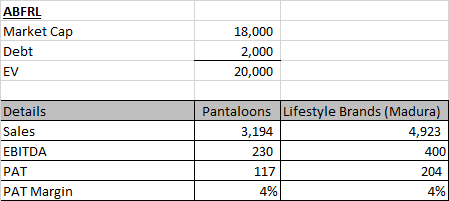

Some data on Raymond and its competitors -

-

PremiInvest bought FabIndia for 4500 Crores for 8% stake in 2019. FabIndia had sales of 1100 Crores and PAT of 116 Crores

-

PE Firm Kedaara Capital valued Manyavar at 4000 Crores for a 10% stake in 2017. Manyavar had sales of 500 Crores and Profit of 90 Crores

-

Now Raymond does sales of 6500 odd crore and optically speaking has an equally decent brand like FabIndia and Manyavar and should also be valued north of 4500 Crore.

-

The problem however is in the PAT margins. While Manyavar shows a PAT margin of 18% and FABIndia shows PAT Margin of 18%, the PAT margin of Raymond and other players are as follows. (Not taking EBITDA margins due to constraints on lack of data , and hence comparing EV)

I feel that problem with Raymonds is their Franchise model, where bulk of margins end up going in hand of franchise.

While for Manyavar and FAB India this comes on books, however they have a huge fat Rent/Employee Cost on their books.

Even with this thesis when we proceed, the rent of Raymonds is very similar to Manyavar and, FAB India and TCNS and hence this low PAT margin is perplexing

8 Likes

So as per latest presentation the co has approx 1600 Exclusive stores (TRS + EBO). Though there is no breakup between Owned + Frnachise.

This also needs to be tracked against Manyavar and FabIndia.

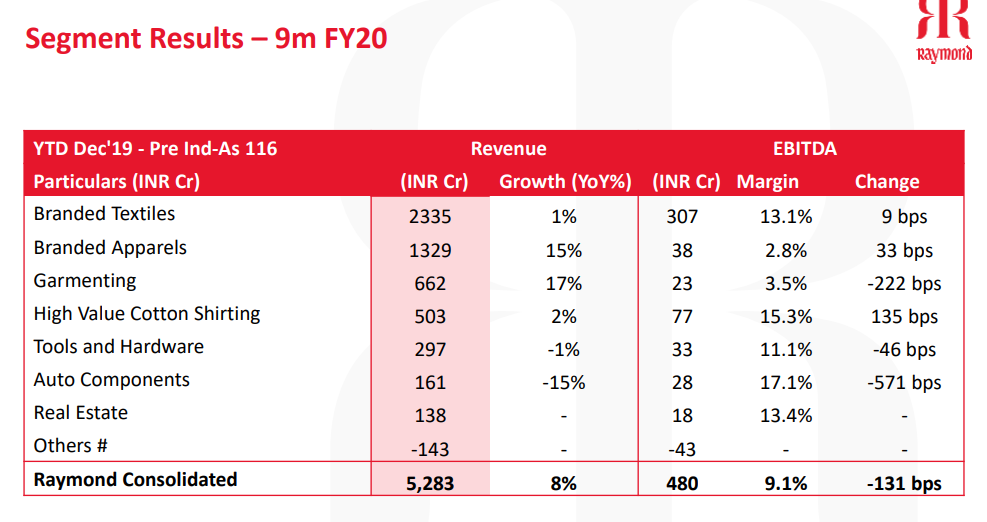

The bigger problem however is…2% Margins in the Apparel segment. This looks like a trading entity and from optical eye it gives an image that bulk of the value in the chain is captured by Franchisees instead of Co.

Branded Textile is the only place where co enjoys some pricing power with bulk of Revenue and EBITDA being contributed by this

Mind you, Interest and Depreciation is a real cost in this business.

Have a look at 4th Coloumn

If I were to now value Raymond for the demerger, I would value the textile+Apparel biz at 7-8times EV-EBITDA or so, because the texture of the performance makes me believe that in essence this is a Textile Co and doesnt make money in Apparel

2 Likes

Sanjay Behl, CEO-Lifestyle Business, Raymond Limited, steps down

96a06f61-c81d-4d55-98ef-ef2fda335f39.pdf (692.1 KB)