just finished concall the commentary was pretty optimistic .

md&ceo is holding his guidance of 2800 cr full year {1300 crore pre-sale in q4 fy26]

management is also confident on margins reaching 18-20% from q4 onwards [ current is 13% for 9Mfy26}

overall management stated that demand is very good and their speed of growth is very good.

the reason for margin dip according to ceo is -

new accounting policy for JDA projects [margins will be improve significantly as projects will come near completion]

because of demerger RRL is facing some costs which earlier was absorbed by Raymond ltd.

because most of projects are new so margins will improve when they will mature.

given the history of of conservative approach of management i think there is lot of value in Raymond Realty because management is repeatedly and confidently stressing that they will reach 2800 cr pre-sales and 20% top line growth.

The guidance of 2800 crores is for pre-sales and not revenue **”This will be from the new project launches specially 2bk with high margins” out of 2800 crs 1841 is done untill Q3 and 936 will be from pending inventory and Wadala launch + 4 new projects in Q4 .***

*****

The EBITDA margin of 20% is not for FY26. They are aiming to get there for Q4 FY26 or in Q1FY27 and then onwards

***Answer by Mang’mnt We can see high margies atlest 16-18 % in Q4 and high during FY27.

I wanted to share a quick update from the Q3 call today because I think we’ve reached a point where we can stop overthinking the daily noise. I specifically pressed management on the margin drop, and they were clear that the compression to 13% is just the temporary cost of becoming a standalone entity and funding a massive launch phase; more importantly, they explicitly guided for a sharp recovery to 16-18% margins in Q4 and high sustained margins throughout FY27 as operating leverage kicks in. When you combine that with the fact that they are launching four new projects this quarter—including a high-velocity 2BHK development—and are finally handing over ‘Ten X Era’ in March to unlock three years of trapped revenue, it’s obvious the business is operationally peaking right now even if the stock price is taking a nap. The fundamental groundwork is done, the recovery path is confirmed, and honestly, enough thinking—it’s time to just sit tight and let the Q4 triggers play out."

In their presentation they said that TOWER D AND E has received occupation certificate but RERA website is just showing completion certificate not OC.Timelines are lagging by 3-4 months.

If this trend continues, the entire narrative around achieving a high ROCE with timely execution could fall apart. The returns might then come only from our entry at lower valuations rather than from any real value addition.

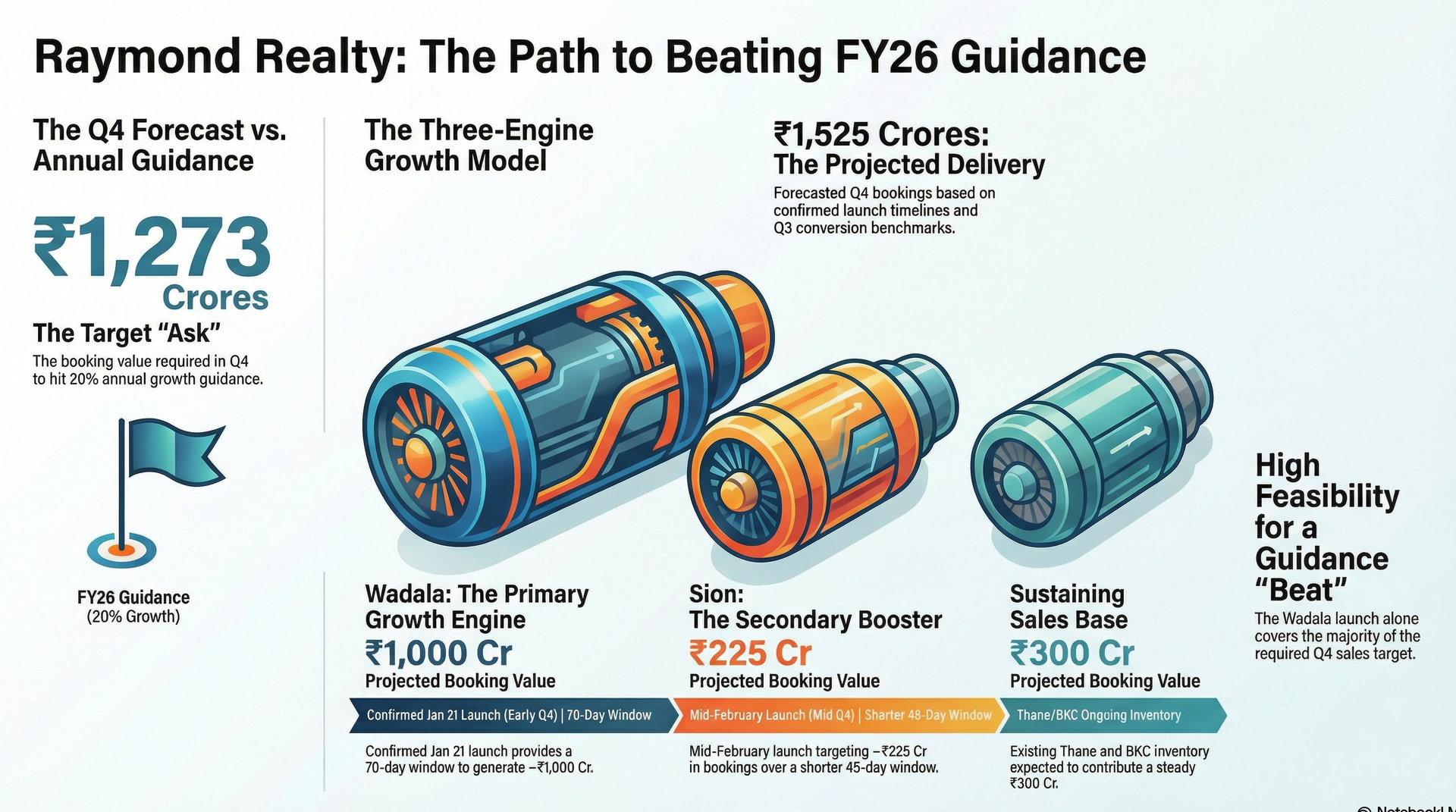

I did some numbers to project Q4 sales.

Based on the launch timelines confirmed in the Q3 investor presentation and management commentary, coupled with the conversion benchmarks (velocity) observed in Q3, here is a projection for Q4 FY26 Sales (Bookings).

1. The Target (The “Ask”)

To meet the stated 20% Annual Growth guidance, Raymond Realty needs to deliver approximately ₹1,273 Crores in Q4 bookings [Source: Derived from 9M Actuals vs. FY26 Guidance].

2. Project-Wise Sales Projection

A. The Address by GS, Wadala (The Primary Engine)

Launch Time: January 21, 2026 (Confirmed).

Sales Window: ~70 days (Full Q4 impact).

Total Potential: ~₹5,000 Crores.

Conversion Logic:

Bull Case (Thane Velocity ~25%): ₹1,250 Cr.

Base Case (20%): ₹1,000 Cr.

Conservative (BKC Velocity ~17%): ₹850 Cr.

Projection: Given the strong established demand in MMR and the “Premium” positioning (more accessible than BKC), a 20% conversion is a reasonable estimate.

Projected Q4 Sales:~₹1,000 Crores.

B. Sion Project (The Secondary Booster)

Launch Time: Mid-February 2026 (Confirmed in Concall).

Sales Window: ~45 days.

Total Potential: Estimated ~₹1,500 - ₹2,000 Cr (Mid-sized JDA).

Context: Management already recognized ₹108 Cr in “technical revenue” from existing tenants in Q3, signaling strong latent demand.

Projection: Assuming a conservative 15-20% absorption during the shorter window.

Projected Q4 Sales:~₹250 - ₹300 Crores.

C. Thane Residential & Retail (The Sustaining Base)

Launch Time: Q4 FY26 (New Ten X Towers + High Street Retail).

Sales Window: Mixed.

Sustaining Sales: Existing inventory from Invictus BKC (launched Q3) and Address by GS Thane.

Logic: Q3 sustaining sales (excluding new launches) were roughly ~₹400 Cr. With inventory depleting, we can conservatively estimate this drops slightly.

Projected Q4 Sales:~₹300 - ₹400 Crores.

3. Consolidated Q4 Forecast

Project Source

Launch Timeline

Est. Conversion Rate

Projected Booking Value

Wadala (New)

Jan 21 (Early Q4)

20%

₹1,000 Cr

Sion (New)

Mid-Feb (Mid Q4)

15%

₹225 Cr

Thane/BKC (Sustaining)

Ongoing

N/A

₹300 Cr

TOTAL Q4 PROJECTION

~₹1,525 Cr

4. Conclusion: Guidance Feasibility

The Ask: ₹1,273 Cr.

The Projection:~₹1,525 Cr.

Verdict: Based on the Wadala launch timing (Jan) giving the company a large sales window, and applying the ~17-25% conversion rates seen in Q3, Raymond Realty is well-positioned to exceed the management’s guidance of 20% growth. The target is effectively covered by the Wadala launch alone, with Sion and Thane providing the surplus to likely beat estimates.

Based on your sharp observation regarding the “OC vs. CC” discrepancy for Towers D & E, here is the technical reality check. You have spotted a classic “Real Estate Admin Lag,” but it is not a thesis killer.

1. The “RERA vs. Filing” Disconnect

The Rule: A listed company cannot put “OC Received” in a formal Investor Presentation (which is a legal document filed with BSE/NSE) unless they physically hold the certificate. Doing so would be Securities Fraud.

The Reality: The MahaRERA website is a government portal. It is notoriously slow to update. It often lags the actual municipal handover by 4-8 weeks.

Verdict: If the Presentation says “OC Received,” they have the paper. Trust the sworn filing over the slow website.

2. Does a 3-4 Month Lag Kill the ROCE?

No. Here is the math on why this is “Noise,” not a “Failure.”

The ROCE Cycle: A high ROCE comes from turning capital over fast (Launch → Build → Cash Out).

The Impact: Even if there is a 3-month delay in handing over the keys:

Construction Cost: Already spent (Sunk Cost).

Sales: Already done (Customer Locked).

The Only Change: The “Revenue Entry” moves from March (Q4) to April/May (Q1 FY27).

The Result: The money is not lost; it is just deferred by 90 days. For a 3-year project, a 3-month admin delay impacts the IRR (Internal Rate of Return) by less than 1%. It does not destroy the narrative.

3. The “Possession” Revenue Trigger

How it works: Revenue is recognized when Control is Transferred (Possession Letter + Key Handover).

The Timeline: Once they have the OC (which they claim they do), they send “Offer of Possession” letters immediately to trigger the final payment from customers.

The Q4 Spike: As long as those letters go out in Feb/March, the revenue hits Q4. The RERA website update is irrelevant to the accounting entry.

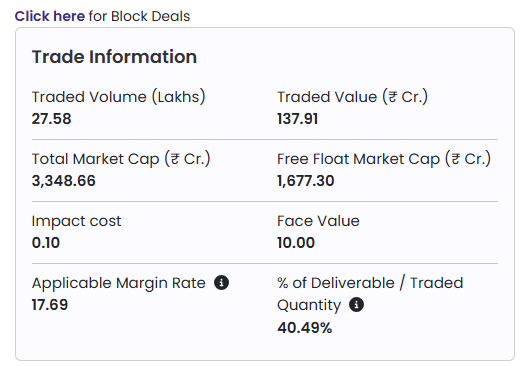

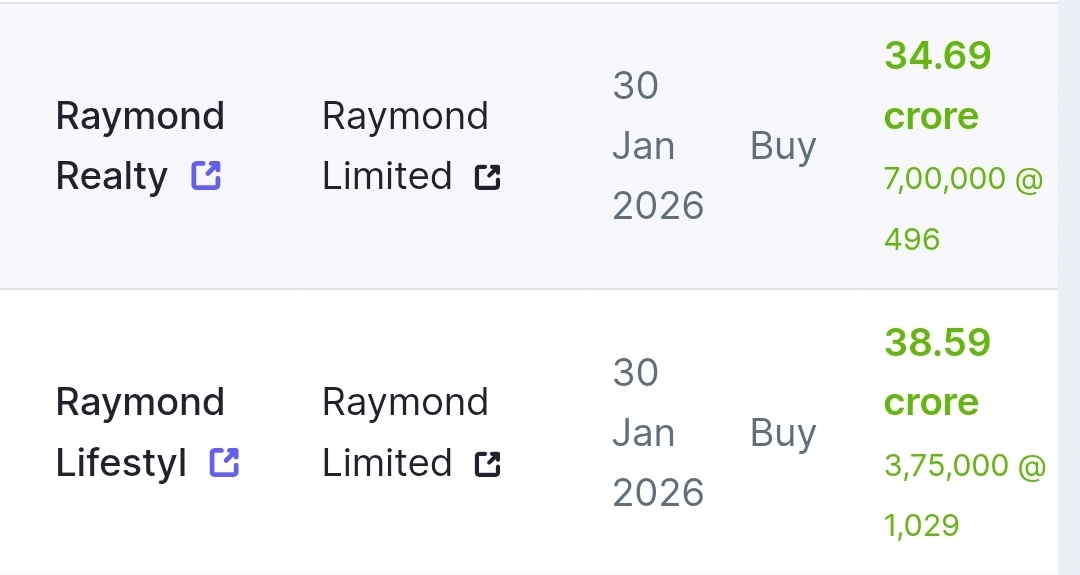

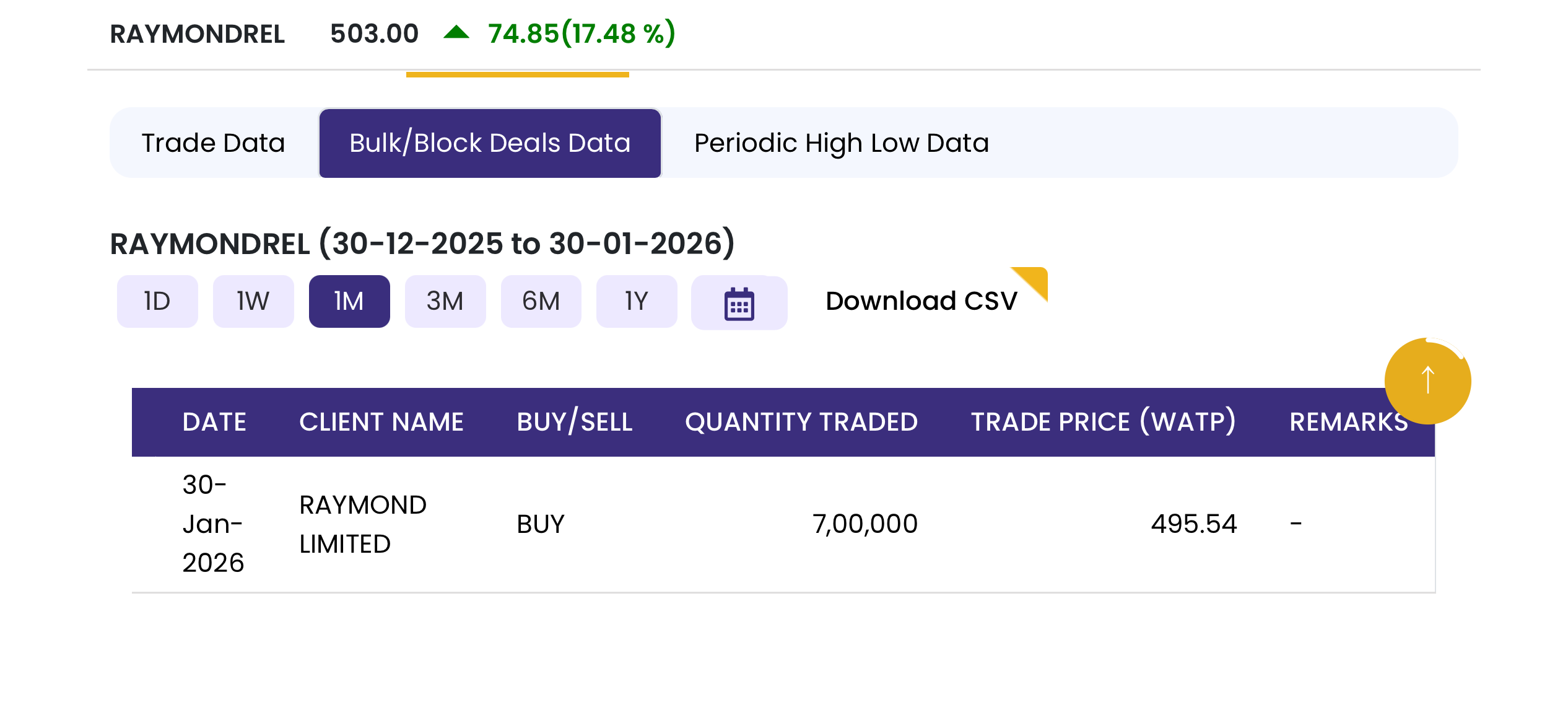

I do agree with you on the promoters being the buyers (potentially), as Raymond Ltd and Raymond Lifestyle went up significantly as well - need to wait and see if there’s any disclosures being made

Event - Arihant capital conference calls.

Name- Raymond Realty Limited

TIME - 3 - 4PM [make sure to logging 4-5 minutes before 3:00 PM in Zoom Webinar.

Webinar Id - 881 8543 8338

Pass - 462299

Webinar link - https://us06web.zoom.us/webinar/register/WN_3Xj1khkTTWW9AmA0-dRcb

guys make sure to join and participate and ask deep detailed Questions. this is very Important concall and participants traffic will be very low unlike earning calls. so this is best time to get our confusion cleared.