@Azhar_12 No dearth of names from the Realty space in the below list. The sector is going through tough times, same is evident in Q3 results. RRs Q3 also should be out soon, numbers/ outlook will give some picture where it stands vis-a-vis.

Disc.: not invested, not a buy/ sell advice. Please DYOR.

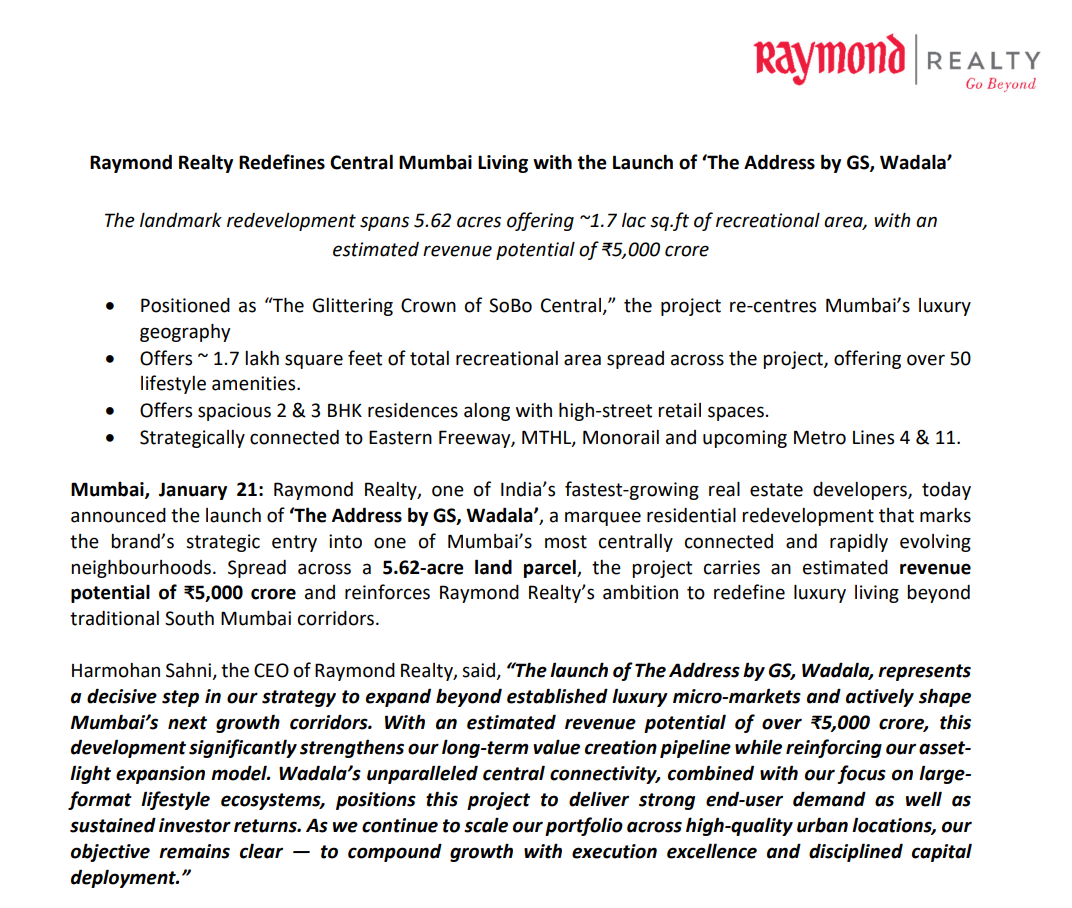

The Address by GS, Wadala launched officially. It was planned by Q3 end itself, so a delay of 3-4 weeks here.

One thing that I have a doubt about is that at the time of signing of project they mentioned GDV of 5000 crores. According to JDA documents available on RERA website, the revenue share of 62:38 is mentioned with 62 being with RRL and rest with the partner (Messrs Renaissance Spaces) who is managing the slum rehabilitation associated with this project. So, a conservative revenue potential estimate of this project will be 3100 crores if my understanding is correct.

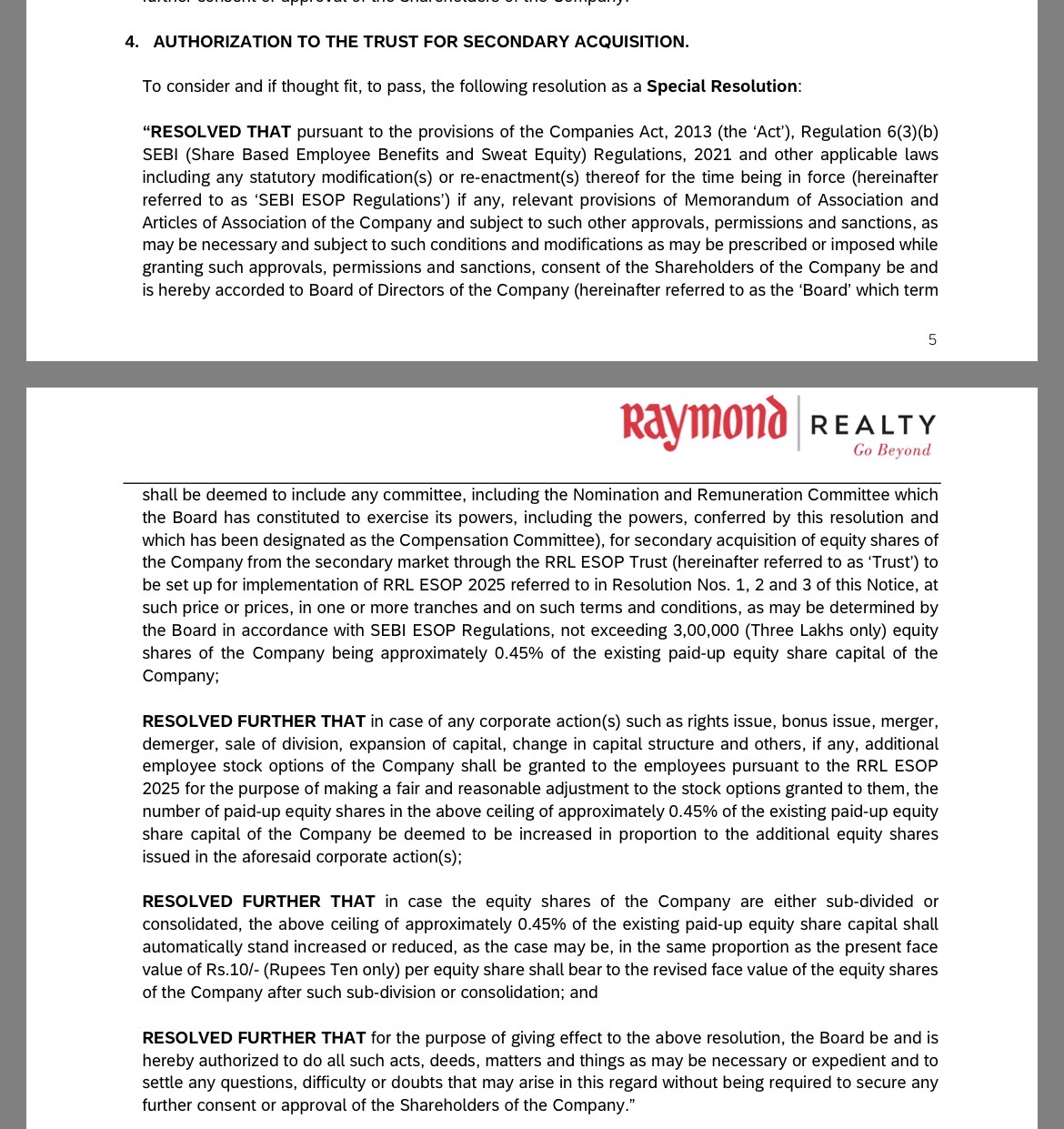

Raymond Realty wants to create a trust to issue ESOPs with an exercise price of INR 404

What’s interesting is that they have also included a proposal to buy 3,00,000 shares from secondary transactions (from the public markets) for the trust that wants to give 16,80,000 ESOPs.

so if the shareholder approval goes through after voting period after February 21st, we have a buyer (the company and the trust) who is happy to buy 3,00,000 shares at any price below 404 as they will ultimately issue this to the company employees at 404 (exercise price)

Thane micro market has two peculiar features existing at the same time.

One Over supply and second increasing prices. Both can’t happen at same time.

So my thinking is there is over supply in Thane but of undesirable projects. Good projects are selling like hot cakes and that’s why prices are increasing. There undesirable projects leads to headlines like inventory of 72 months.

This paradox exists almost everywhere and I talked to few local property dealers to confirm this and they say this phenomenon occurs almost everywhere.

I am not from Mumbai.So if anybody local can confirm this trendz I will be greatful.

So basically they will buy @404 or any price below that , meaning that there is a temporary bottom until they complete all the purchase necessary, which is a good thing right?

This is out of topic question , does any one knows how reality stock revenue is calculated is this based on sales or the % of constructions completed for ex: sales in Q3 or % of completion of project in Q3

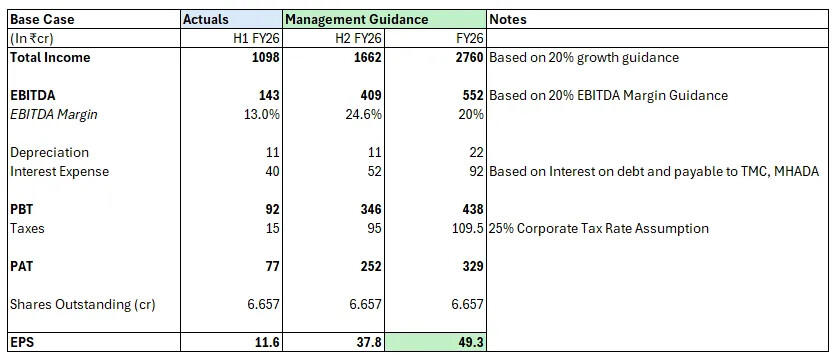

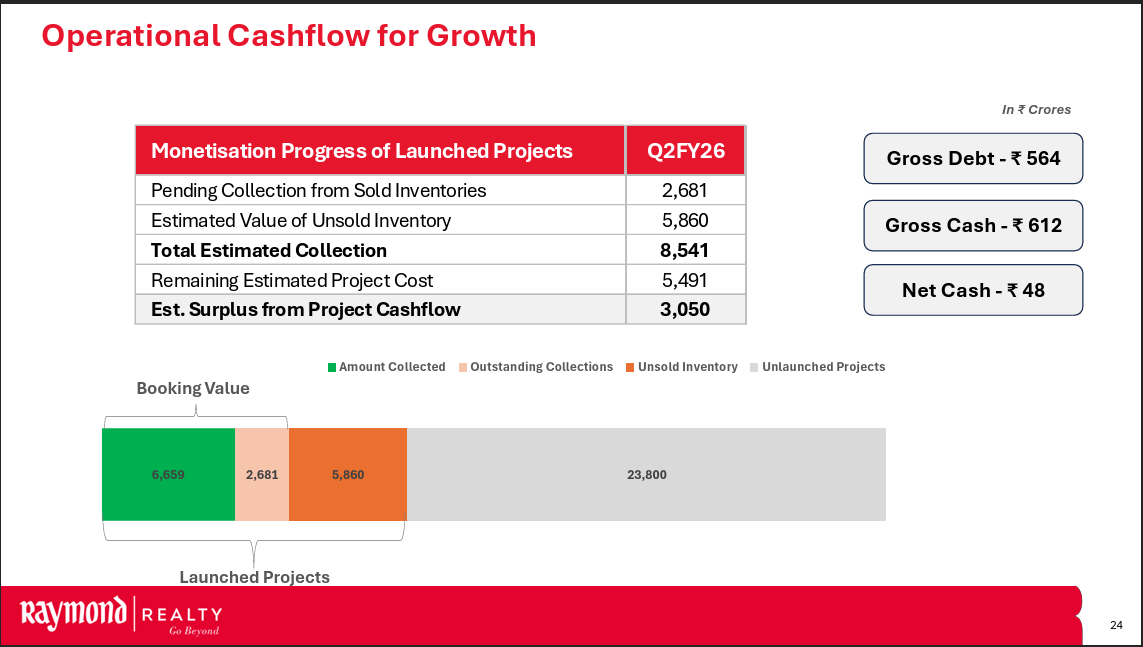

Slight arithmetic error here, so projected booking value for H2FY26 as per company would be ~ 2050 crores and taken together with H1 numbers, pre sales for FY26 should be ~2800crores which is growth of ~21% YoY. Given the history that the management is conservative in giving guidance, my estimate of pre sales for FY26 is between 2900-3000 crores.

Thank you @yeshas7 I got you. complete make sense now I will be continue invested on this , Expecting good results then in Q3 today , I will add concall details in the evening

In the investor presentation (attached screenshot), can anyone clarify the numbers for revenue recognition? For eg, in the BKC project launched last month, they have recognized 175 crores revenue in Q2 (way before project itself was launched). The revenue recognized 261 crores is higher than the booking value of 224 crores….

Same for the Sion project, revenue is already recognized even before project launch.