CEO expects very good second half due to new launches

1 Like

Hey @yeshas7, thanks for your continuous information about the raymond reality.

I have a small doubt, as you mentioned.

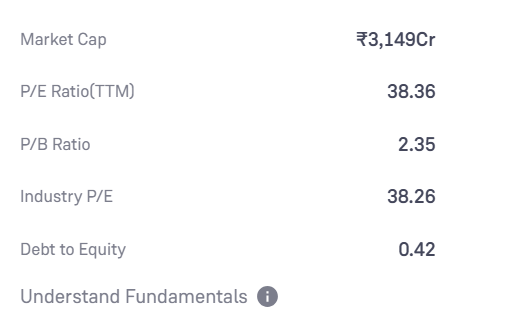

but on grow it’s showing 38.36 more than industry average

I believe that the 38 P/E showing is the industry P/E and not stock P/E.

As for calculating P/E,

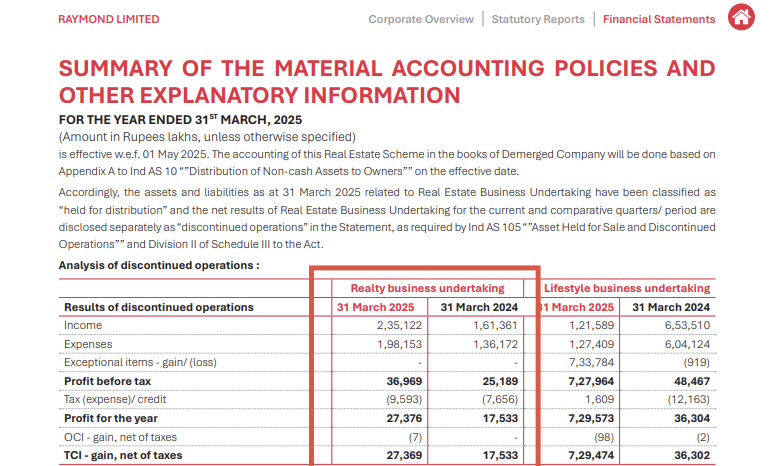

The Raymond Realty financials don’t show the full picture prior to the demerger (which was 1st April 2025)

Pursuant to the approval of the Composite Scheme of Arrangement by the Hon’ble National Company Law Tribunal, the Realty business of Raymond Limited was demerged into a separate entity, Raymond Realty Limited, with effect from April 1, 2025 - the appointed date for the demerger.

It is important to note that prior to the demerger, the Realty business formed an integral part of Raymond Limited. Hence, in the consolidated financial statements for the period preceding the demerger, its results were presented as a discontinued operation in the Raymond Limited Annual Report FY24-25. Following this demerger, the financial results of Raymond Realty Limited from April 1, 2025, onwards are reported independently.

Basically, before 1st April 2025, Raymond Realty Limited held certain assets and projects and had its earnings and Raymond Limited held the other real estate projects, so when we look at Raymond Realty financials in the audited statements it only shows the EPS coming from certain projects.

But if you want accurate FY2025 numbers for Raymond Realty as a whole, it is in Raymond annual report

So 274 crores PAT divided by 6.657 crore shares outstanding gives you EPS of INR 41

At current price: 483/41 =P/E 11.78x

I have created estimates based on management guidance for FY26 EPS of 54

Based on this estimate forward P/E of 9

Quite low

Happy to answer any questions

7 Likes

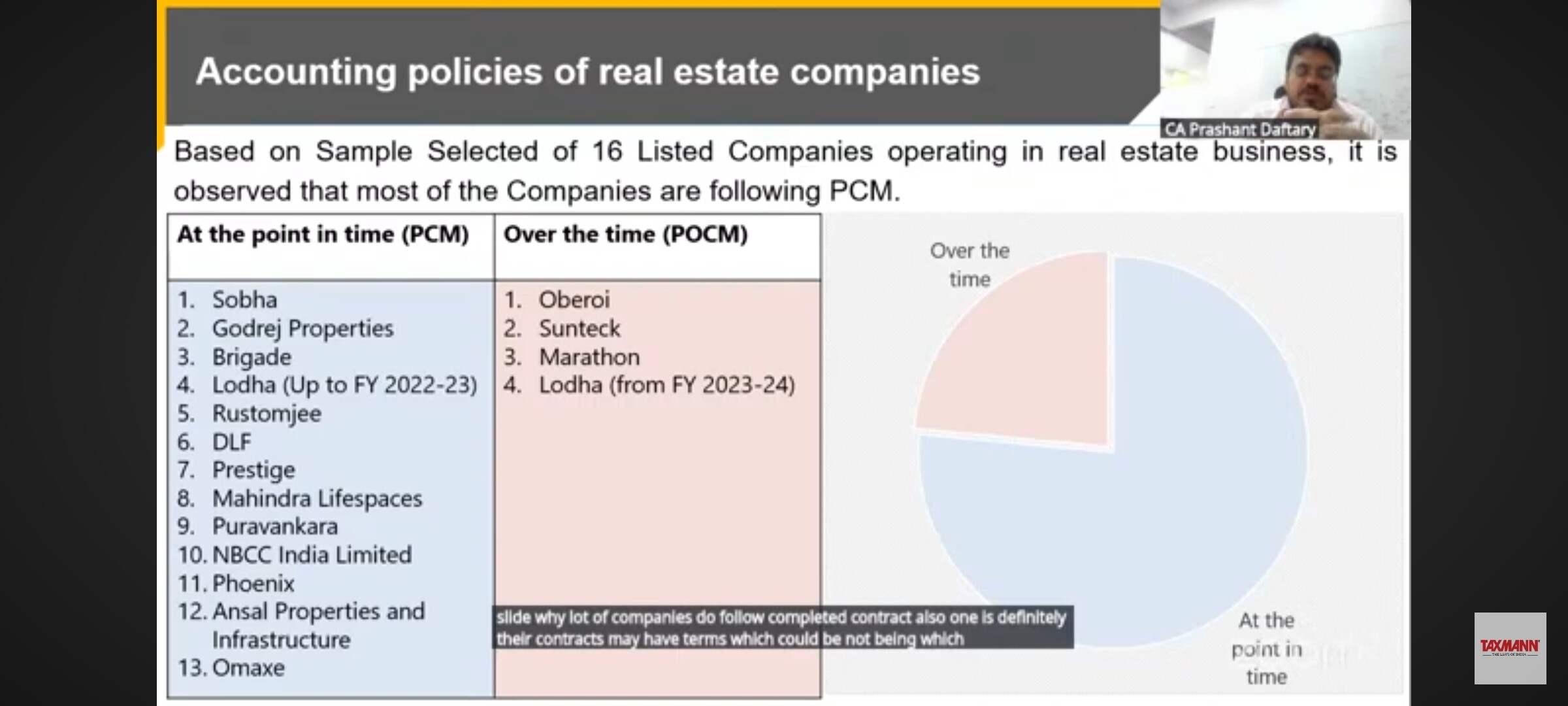

Raymond realty is following Percentage Completion Method (POCM) over Project Completion Method (PCM) which means revenue is recognized as the result of Construction of Project Progresses not on the sales of flats from buyer

Real estate is generally a highly cyclical business

Below is the write up to understand the cycles in Real Estate which happened during the past 20 years

We must be prudent as value investors to take care of the above variables even though it is fairly valued at this CMP 471

To know more about AS Standards for Revenue recognition in Real Estate

3 Likes

While I can appreciate the cyclicality of real estate, I view Raymond Realty as a special situation opportunity (categorised by Joel Greenblatt/Seth Klarman) - institutional selling + unrelated business spinoff has lead to an extremely low cheap price on the business, presenting an attractive opportunity.

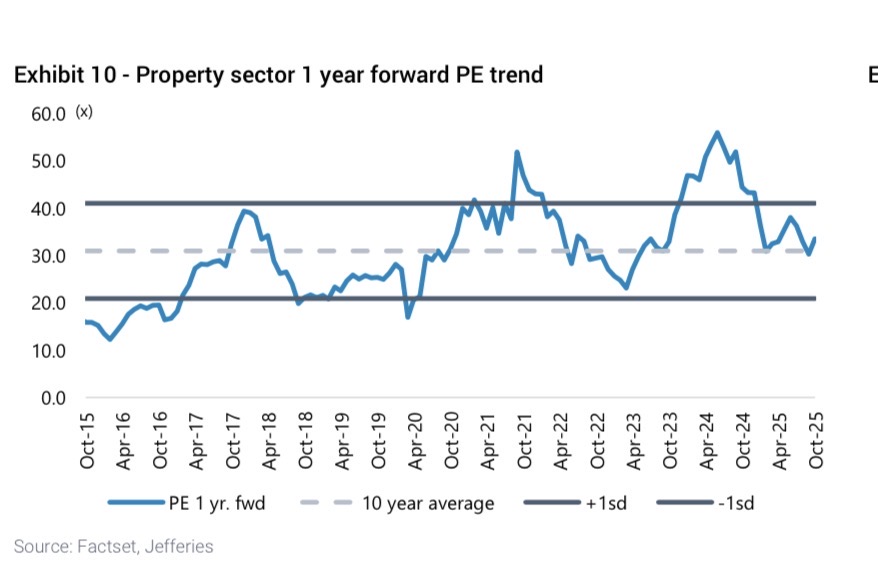

Take for example the real estate valuations across the last 10 years

Real estate developers have traded between 20x and 40x forward earnings, with a 10 year average forward P/E of 30x.

Based on management estimates, the base case earnings for 2026 is INR 50 per share, so even using a discounted 20x multiple yields an implied share price of ~INR 1,000

However, at CMP of 475, the forward P/E is ~9.5x, providing an ample margin of safety for any market or idiosyncratic risk.

If you feel a relative valuation isn’t worth the paper it’s written on, an intrinsic valuation would also point to the discount between price and value - whether you use a liquidation valuation, Discounted Cash Flow or Net Asset Value method.

So in my view, Raymond Realty remains undervalued on both up-cycle and down cycle scenarios. With a margin of safety significant enough to underwrite the investment.

On the macro side, I do think real estate cycle in India is turning upwards than lower. Several leading indicators point to the fact.

- Higher than expected GDP Growth

- Inflation well within targets

- RBI’s dovish stance, lowering interest rates

- Supply and absorption of new constructions in major Indian cities, with the demand often exceeding the supply of units and inventories

However the share price movement is noteworthy, but in my view and in the view of true value investing is the wrong metric to assess business value. Movement in share price is not a measure of risk

Risk shouldn’t be measured with price volatility, rather it should be measured as the probability of a permanent loss of capital

A humorous note on X reminds me of this very idea

This view has been echoed by everyone from Warren Buffet to Seth Klarman.

A permanent loss of capital in Raymond Realty’s situation could occur if the company becomes insolvent. However, the company has a negative net debt position (Cash>Debt) and has good credit ratings and financing in place. So with the exception of fraud, accounting trickery etc I don’t think the business is at risk of failure. Add to the 100 year legacy of Raymond Group, I think this one is here to stay. This thing is priced like the company will fail and implode in the near future at distressed valuations, but a few quarters exhibiting continued execution could potentially change the narrative, and maybe, if we’re lucky, see a rerating in the share price.

8 Likes

Sales executive status boom boom on 2bhk sales good expected q3 numbers I am assuming 1500 upto revenue and PAT 250 to 300 cr.

2 Likes

Can anybody calculate what will be their current inventory of unsold flats project wise or share your ideas ,logic on how to arrive at it approx ?

What is mean by m sales???

I cant get it

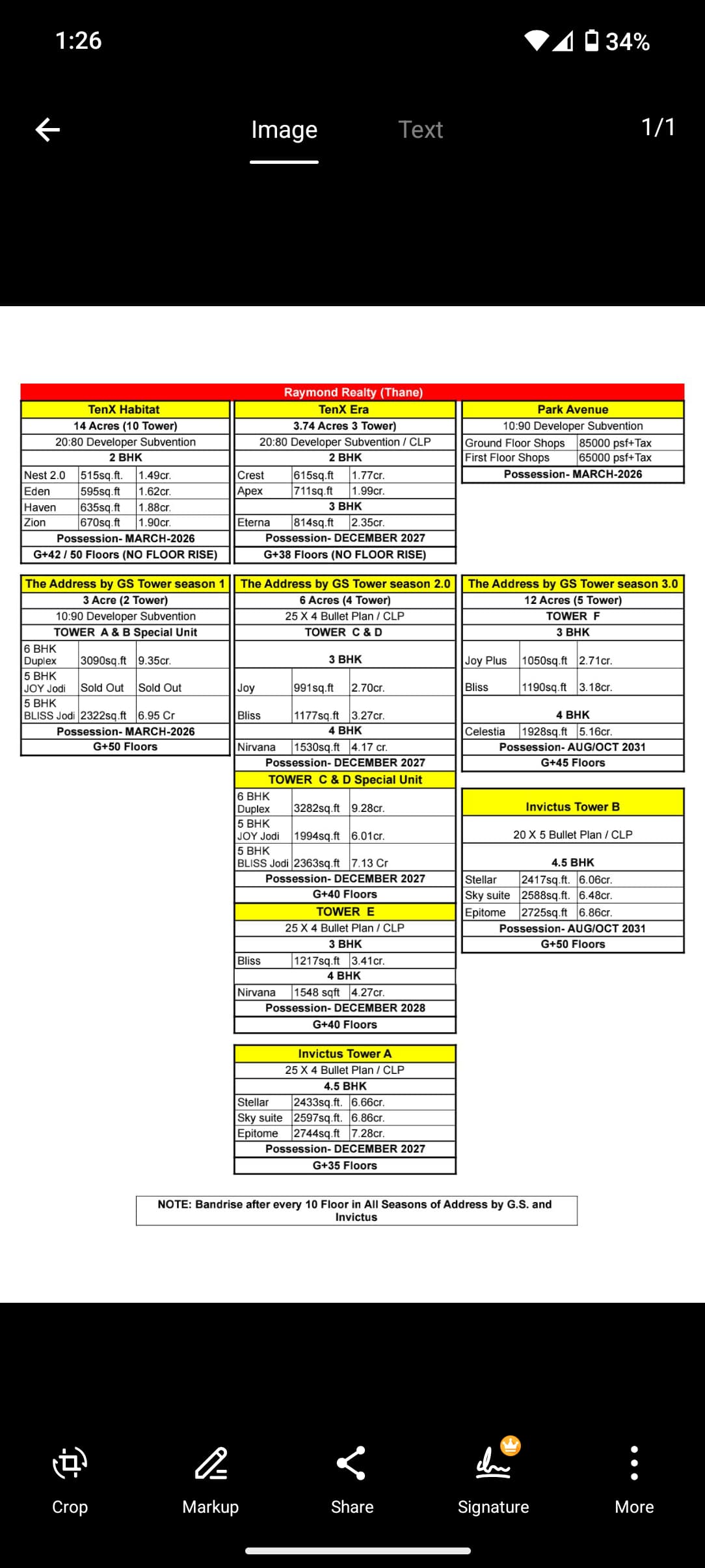

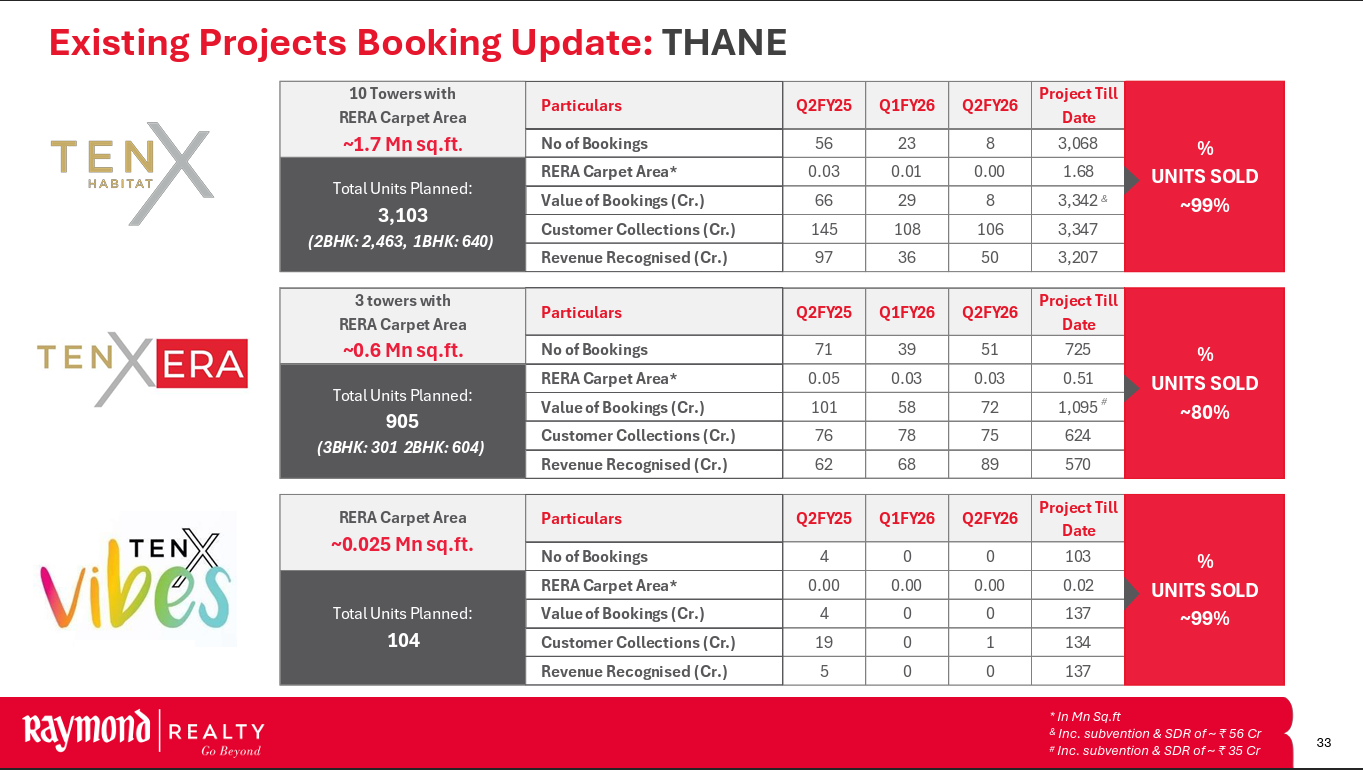

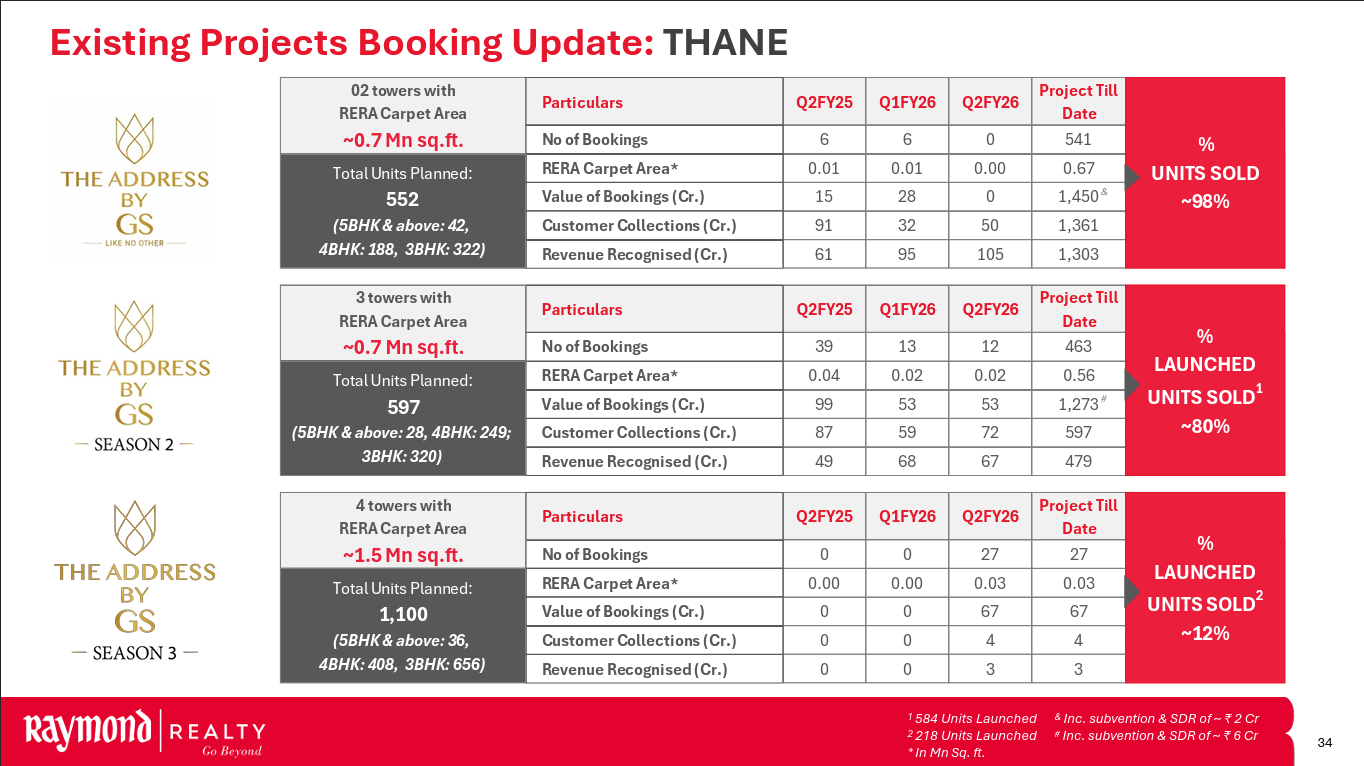

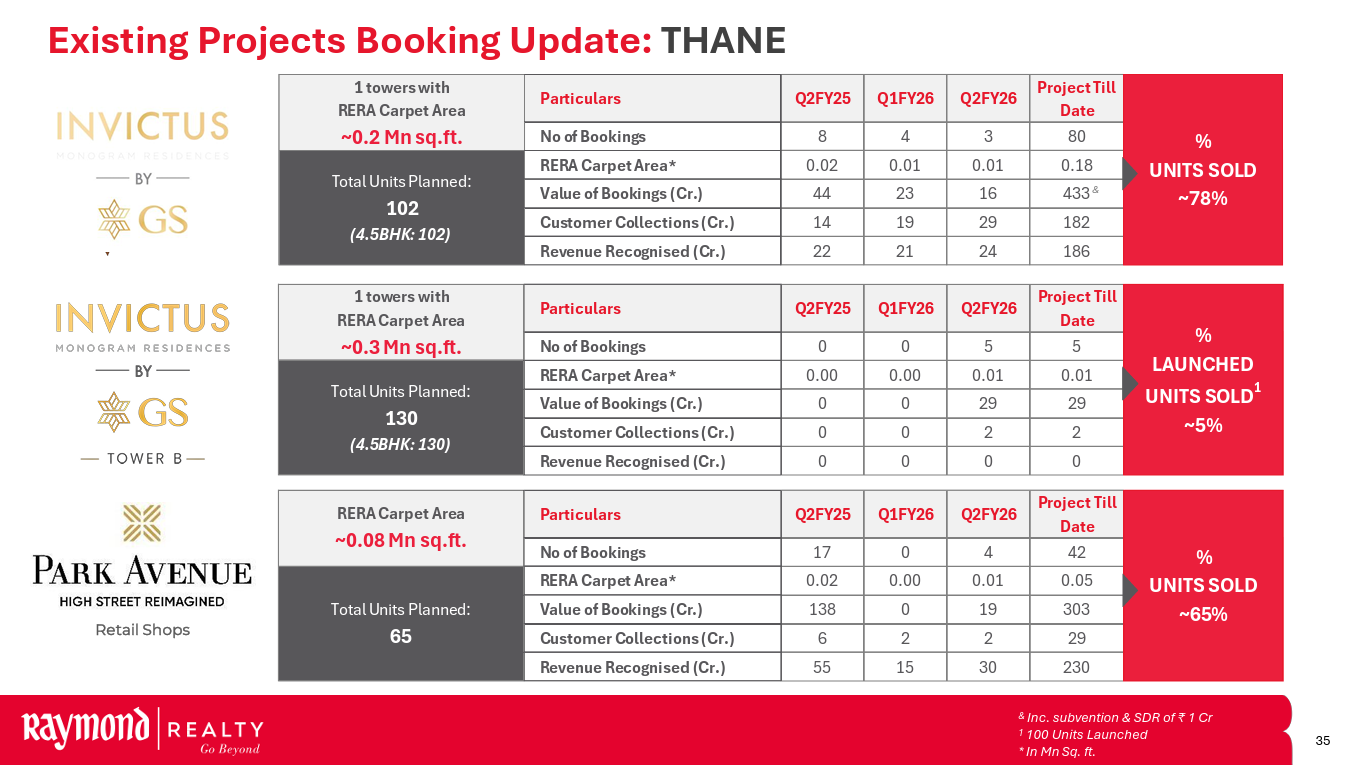

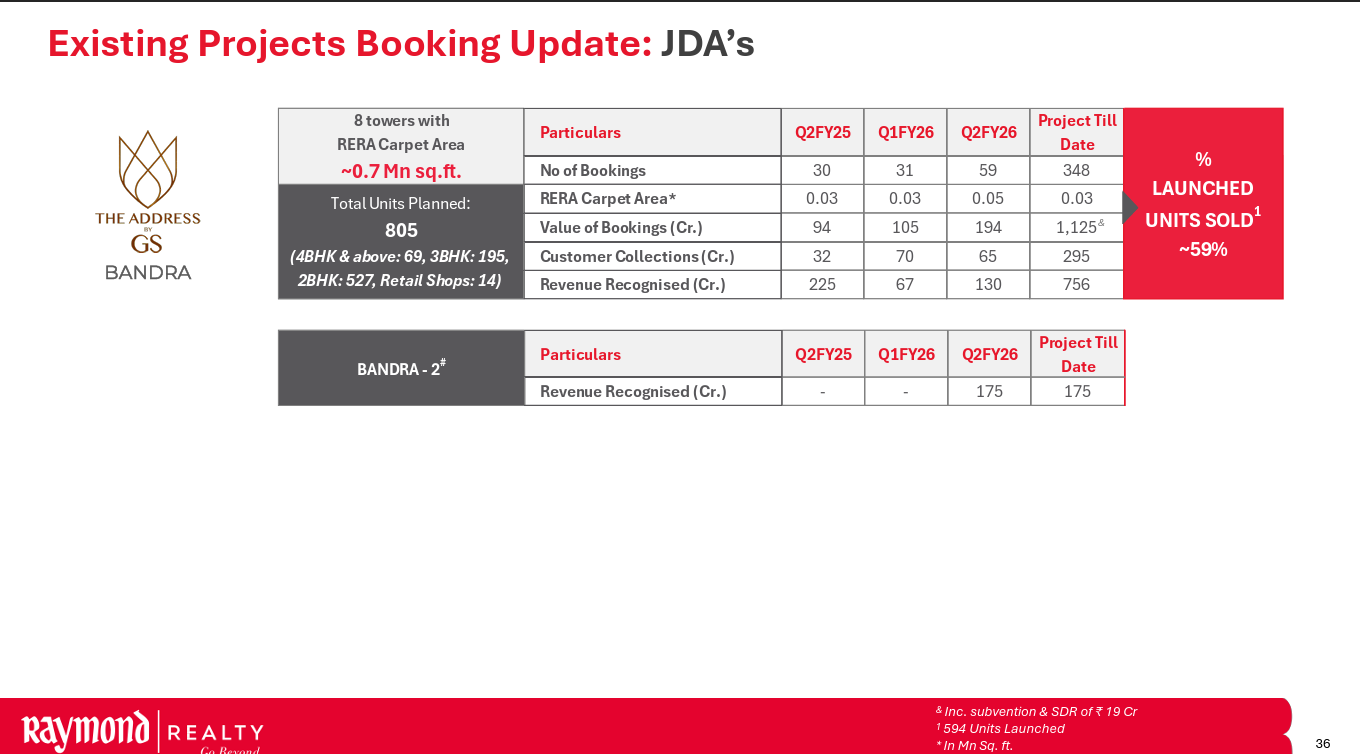

They present these numbers on their investor deck

RRL_28102025181037_Investor_PPT.pdf (4.4 MB)

I have also put it on excel for easy access and calculations

RRL_existing Projects.xlsx (16.7 KB)

2 Likes

What’s the basis for this calculation. And how reliable is the data shared?

I have done some channel checks, quite reliable as the information comes directly from Raymond Realty’s channel partners