As the stock has been excluded from indices, most of these funds have sold out of their position as they are mandated to only hold stocks that belong to the index they track

Gemini response to - Did raymond demerger create any value for the shareholders?

The short answer is yes, the demerger initially created significant value (unlocking a potential ~40-50% upside at the time of listing). However, investors who held on until today (November 2025) have seen much of that value erode due to a sharp correction in the stock prices of all three entities.

To give you the complete picture, we need to look at the “Sum of Parts” before and after the two major splits: Raymond Lifestyle (September 2024) and Raymond Realty (July 2025).

The “Value Unlocking” Calculation

Let’s calculate the value for a shareholder who owned 5 shares of the original Raymond Ltd just before the first demerger (July 2024).

1. The Starting Point (July 2024)

Holding: 5 Shares of Raymond Ltd.

Market Price: ~₹3,200 per share (Peak pre-split price).

Total Portfolio Value:₹16,000.

2. The Peak Value (Post-Listings)

After both demergers, the shareholder would own three distinct sets of shares. At their listing peaks, the value looked like this:

Entity

Quantity

Peak Price (Approx.)

Total Value

Raymond Ltd (Residual/Engineering)

5 Shares

~₹2,000 (Sept '24)

₹10,000

Raymond Lifestyle (4:5 Ratio)

4 Shares

~₹3,000 (Listing High)

₹12,000

Raymond Realty (1:1 Ratio)

5 Shares

~₹1,050 (Listing High)

₹5,250

TOTAL PEAK VALUE

~₹27,250

Verdict: The structural separation was a massive success, theoretically turning a ₹16,000 investment into ₹27,250—a gain of nearly 70% due to the “holding company discount” being removed.

The Current Reality (November 2025)

However, the market has corrected significantly in late 2025. If that same shareholder held all shares until today, the picture is different.

Entity

Quantity

Current Price (Nov '25)*

Current Value

Raymond Ltd (Engineering/Denim)

5 Shares

~₹496

₹2,480

Raymond Lifestyle

4 Shares

~₹1,120

₹4,480

Raymond Realty

5 Shares

~₹487

₹2,435

TOTAL CURRENT VALUE

~₹9,395

*Note: Prices are estimates based on market data from mid-late November 2025.

The Grim Reality: The current portfolio value (~₹9,400) is lower than the pre-demerger investment (~₹16,000).

Why the Discrepancy?

Lifestyle Correction: Raymond Lifestyle listed at a very high premium (₹3,000) but has since corrected by over 60% (to ~₹1,100), likely due to cooling consumption demand or initial overvaluation.

Realty Correction: After a strong debut, the realty stock has also halved from its peak.

Engineering Cyclicality: The residual engineering business is currently trading at a lower valuation multiple compared to the hype it had when it was combined with the other flashy segments.

Conclusion

Did it create value?

Structurally: Yes. The demerger successfully separated three distinct businesses (Lifestyle, Real Estate, Engineering), allowing the market to price them individually. At the time of listing, this unlocked massive wealth.

For Long-Term Holders: No (currently). If you did not book profits during the post-listing euphoria in late 2024 or early 2025, the subsequent market correction has eroded the unlocked gains.

Strategic Takeaway: The Raymond demerger is a classic textbook example of how corporate actions can unlock value, but they cannot sustain value if the underlying sector performance or broader market sentiment turns negative.

What do you think is the reason for the street’s skepticism for the Raymond Group? I am not fully aware of any corporate governance issues for this group

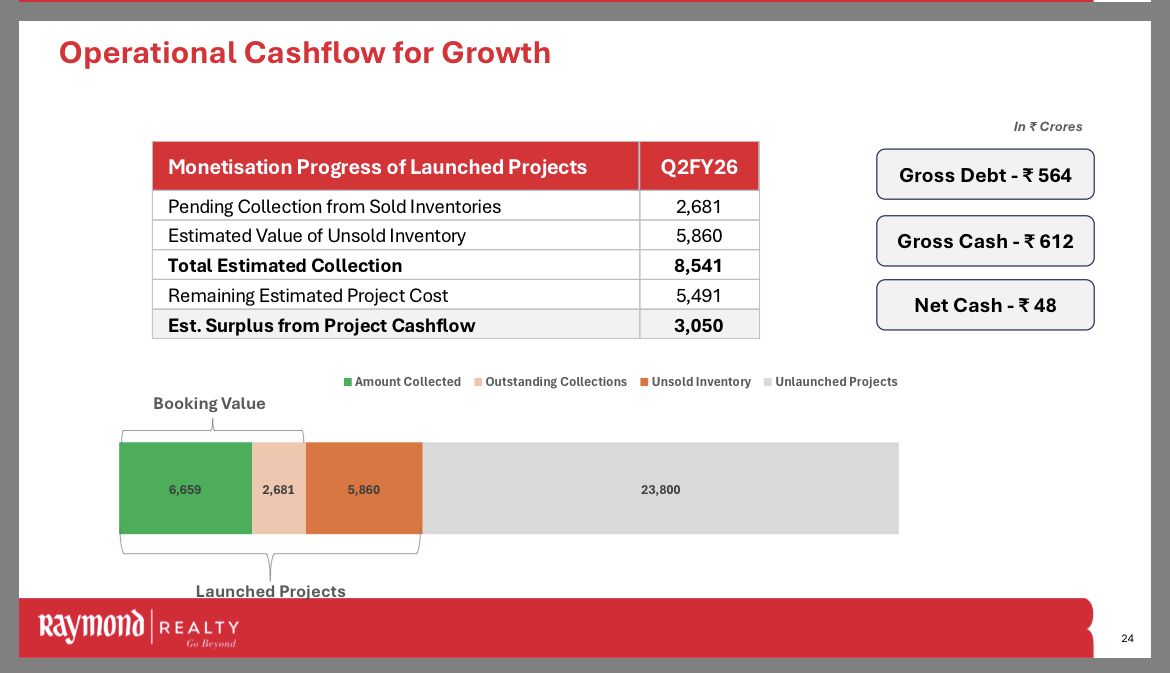

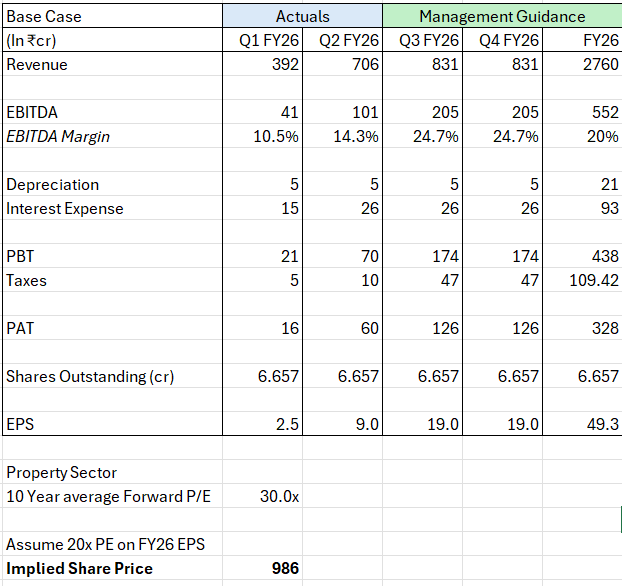

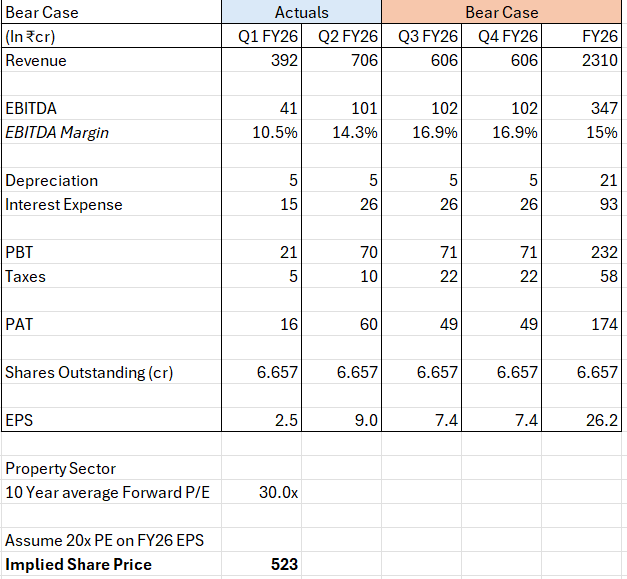

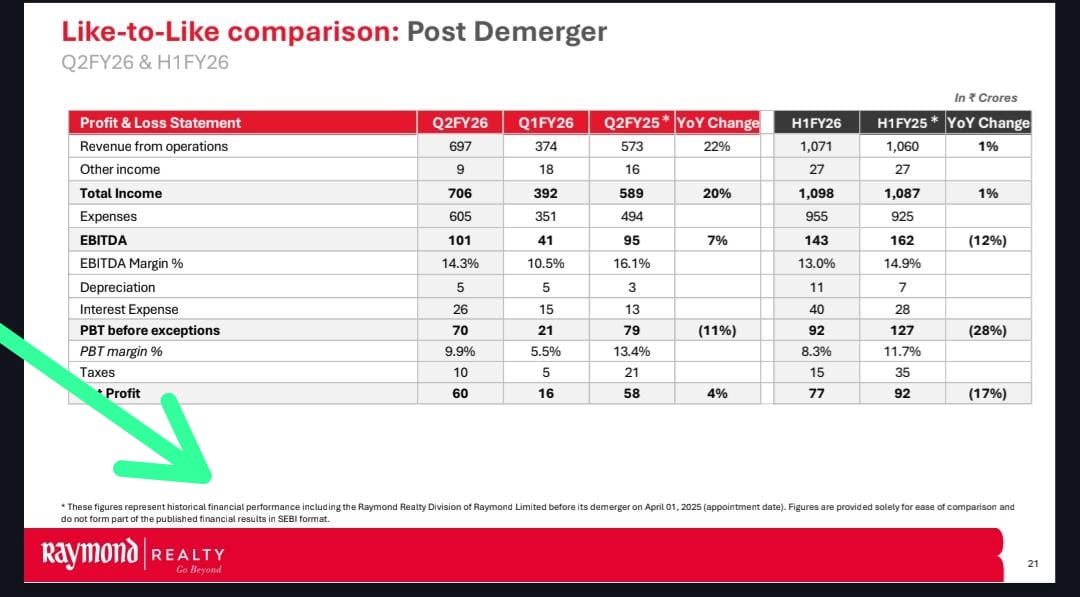

In terms of numbers, in my opinion they have done quite well - meeting or exceeding expectations

in Q1 FY26 they did 392cr revenue on 10% EBITDA margin and cited lack of inventory for the lower sales and dip in operating leverage for the margins, which I felt was a bit hollow but gave them the benefit of the doubt.

They did reiterate their guidance of 20% growth in top-line and 20% EBITDA margin for full year FY 26, despite the weak Q1 FY26 - and explained that most of their launches will come in Q3FY26 and Q4FY26 and can bring some additional inventory for Q2, and also kept expectations low by stating that Q2 is also expected to be in line with Q1

Come Q2, to my surprise - they delivered exactly what they said, if not better - 700cr revenue on ~14% EBITDA Margin, and stated that they are still on track for Full Year FY 26 guidance.

The numbers also seemed to check out

Currently, RRL trades at a Forward P/E of just 9x, which I will say is ridiculously cheap when the 10 year average forward P/E in the property sector is 30x

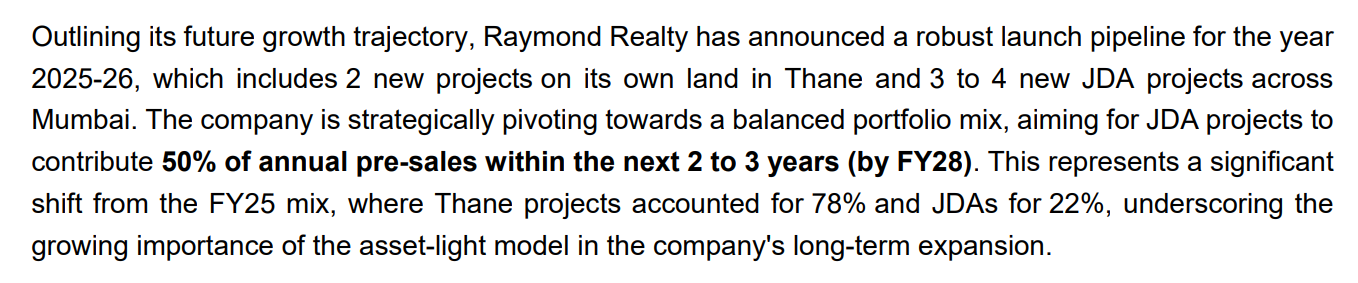

Reports of some mixed development coming up on 7.26 acres of Thane land parcel.

This could be the first foray of Raymond Realty into proper commercial real estate, till now they have only done some small retail units which were attached to residential gated developments.

Realisations and margins could be better in commercial development, need to watch what is the plan whether outright sale or mix of sale and leasing.

Big news for Thane! 🔥

Raymond Realty plans a huge 1.35M+ sq ft commercial complex on 7.26 acres at Pokhran Road.

Features: offices/IT, retail, restaurants, banquets, club & auditorium

Also, multiple posts on social media seems to indicate that a new project branded as Invictus by GS (Bandra 2 JDA, in MIG Colony) is getting launched very soon. Wadala launch is also expected in Q3.

Power is the freedom to shape your own world.

A life where every moment is perfectly held, every choice made with intention.

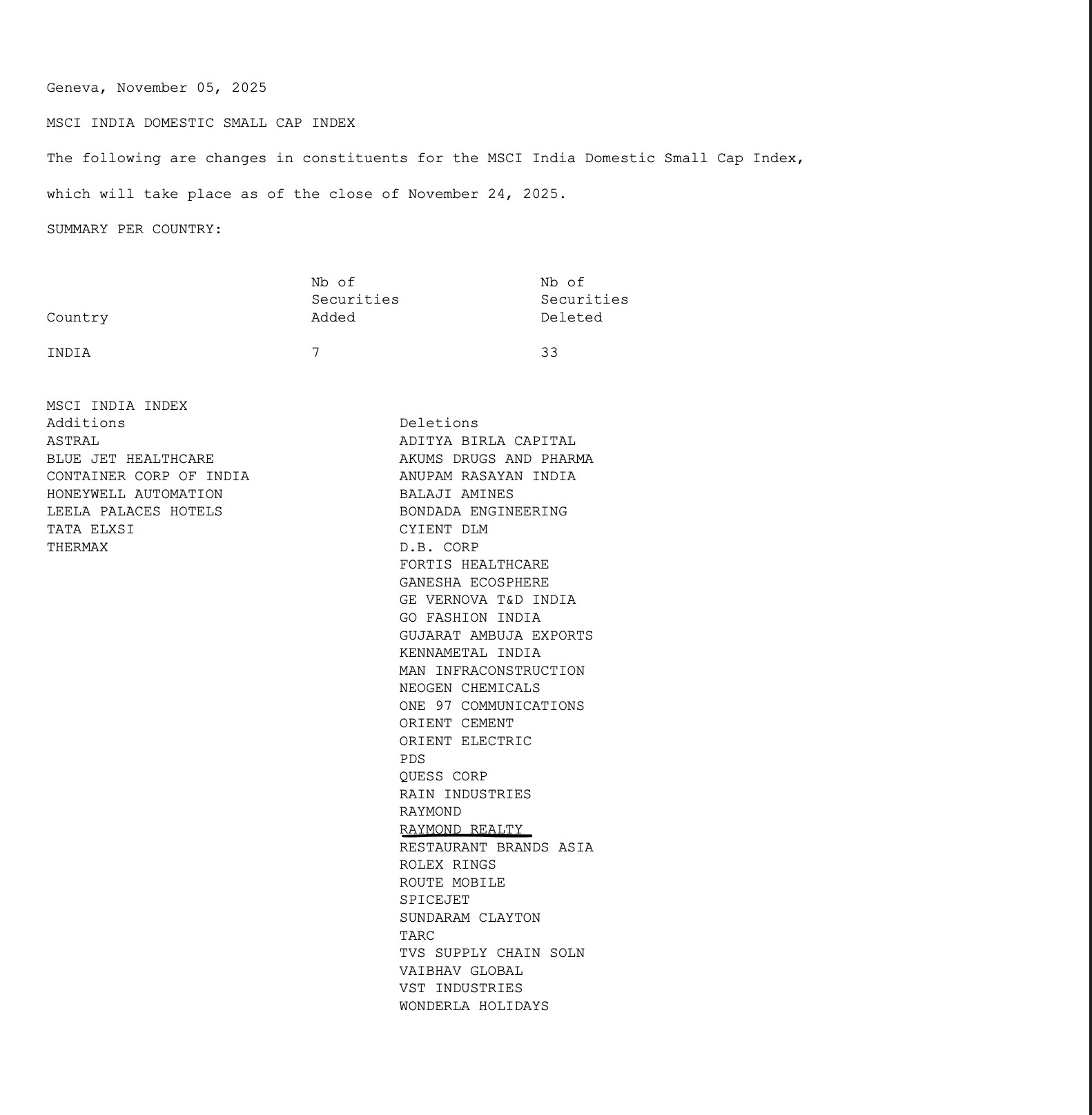

Another point leading to a sharp fall today in the stock was the MSCI rejig in which Raymond Realty was deleted from the MSCI India Index. This lead to sharp sell off from index funds with most of the volume in the last 30 minutes, overall around 72% delivery percentage reported on NSE.

The numbers mentioned in the investor presentation are not relaible

Because it is mentioned in the every page of presentation in very small sized letter

“These figures represent historical financial performance including the Raymond Realty Division of Raymond Limited before its demerger on April 01, 2025 (appointment date). Figures are provided solely for ease of comparison and

do not form part of the published financial results in SEBI format.”

I am trying to ascertain Raymond Realty’s Financials, and I am currently having a hard time putting together the numbers.

I am concerned about which source to rely on to understand the company’s financial performance.

In the Raymond Annual Report for Financial Year 2024-25, the Total Income of the Real Estate Undertaking is provided as INR 2,351 cr for Financial year ended 2024-25 in Note 44 “Analysis of discontinued operations” on page 369

Similar Numbers have been provided in the investor presentation dated June 2025 on page 35

However, on the information memorandum and the Q1FY26 results that were announced, the revenue numbers are different.

In the information memorandum dated June 2025 on page 131 the Total income for the financial year ended 31 March 2025 is stated as INR 567 cr

And on the latest published results for Q1 FY26, the consolidated revenue for year ended FY2024-25 is provided as INR 567 cr

Rate change for 2025-26 (statewide) RR rates in Maharashtra revised effective 1 April 2025.

Increase for Thane district + 7.72% over previous RR rate.

Purpose of RR Rate Used by state govt for stamp duty / registration — defines minimum “official value” for property sale registration.

For FY 2025-26, RR (circle-rate) for Thane has officially increased 7.72%. So any stamp-duty / registration will be calculated on new RR (unless agreement value is higher).

If you buy a flat in Thane now (2025-26), the government cost (stamp-duty + registration) will be higher than last fiscal/year — this will raise the effective cost a bit.

But exact “per-sq ft RR value for your locality” is not publicly available from the recent revision (at least in formats

But there’s no reliable public data giving absolute RR rate (₹/sq ft) for each locality under Thane for FY 2025-26

some of my enquiries with not so reliable real estate people in this area suggested a around Rs70cr per acre around Raymond and Pokharan road , so the remaining land is valued easily more than entire company, big overhang here is Legacy Raymond corporate governance and Realty is relatively new , may need 3-4 more years of execution with credibility.

Plz listen to their concall last Q, I think they briefly mentioned it and clarified how its accounted (CEO mentioned , it no way reflects the current market price of land assets)