This company is in to the manufacturing of steel tubes and pipes. They have two broad segments which are carbon steel and stainless steel tubes.

The current price or valuation metrics are below:-

CMP: 129.25

PE - 4.8

PB - 0.94

BV (pershare) - 139.33

Div Yield: 3%

Market Cap: 610 crore

ROCE is over 18% and ROE is over 20% for the year ending March 2013.

Looking at the number and the valuation ratios it appears attractive but I have a few questions on which I’m looking for more clarity.

So far the business has been good, but how does the business model work and how will it do in future ?

What about the quality of management? Are they focused on enhancing shareholder value?

The management was mentioning oil/gas and power sector as the major triggers for future growth in its annual report (2013). What kind of impact will be seen on the earnings or EPS?

Had read on this co sometime back and had liked it. I felt the quality of mgmt is good. Would be great if we can get some insights on growth prospects going forward.

a. Stainless Steel Tubes: Caters to petrochem refinery and power plant capex. Higher margin segment with EBITDA of 25%. Approved supplier for SABIC ensures mid-east market. They are the #1 player in India in this segment

b. Carbon Steel Tubes: This is LSAW, HSAW and ERW tubes. Some of this is higher margin (20% EBITDA) as they are smaller and can tailor and test products unlike larger players, and the rest is 12%-15% margin business

2). Economic slowdown has impacted their ability to grow especially in the lower margin business. An economic revival is key to robust growth. New refinery capex, power plant capex where Chinese contractors are not turnkey suppliers and city gas distribution are some industry indicators for tracking domestic potential

3). Company has maintained revenues, managed profitability well, and de-leveraged through the cycle. It is a net cash company or close to it. Reflected in decreased interest cost in P&L. So cash flows have been used to deleverage

4). Current capacity allows it to grow at 15% a year for a couple of years with some de-bottlenecking

5). Once growth comes back, he will spend capex (maybe ahead of it) and re-leverage to an optimal cap structure and this will drive both RoE and RoCE

Net-net, they have managed the slowdown extremely well, been innovative in product segments, and look well placed to come out even better in an economic revival. But there fortunes are to a large extent inexplicably linked to oil and gas, power plant and city gas distribution capex, so they need these sectors to start spending again to sustain growth.

For a company with less than a 1000 crore turnover, the promoter takes home a ridiculously high salary! I don’t know if that speaks well about the company!

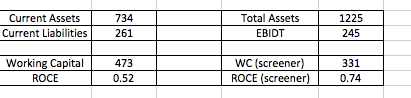

Your RoCE calculation probably has some mistake. FY15 EBITDA was 299 crores and Average Capital Employed (Equity + Net Debt) for FY15 was 792 crores. So pre-tax ROCE works out to 38% and post-tax ROCE works out to 27%.

The important think to note here is that this is a 15%-20% growth story on a medium term trend basis, with some optionality on growth from Euro norm driven capex as well as overall investment cycle pick up. So its possible that growth rates could pick up towards 25%+ as the economic recovery gains steam. Furthermore, in the meanwhile, internal accruals will be sufficient to fund capex and working capital, meaning that the balance sheet is likely to remain very healthy. Hence it probably deserves to trade at a premium to its peers for: current growth and balance sheet strength + well placed to accelerate growth in a recovery.

Talked to company 3 months back. They said 30 to 35 percent of business is oil and gas related. With fall in oil prices some of those orders have dried up. So I decided to sell and get out.

My fears were not unfounded. See 4q results. Numbers should be weak for next 3 quarters at least.

The orders worth 55-56 Crs were not dispatched either due to insufficient financial arrangements (March End, delayed delivery by 15 days etc.)

Customer wanted delivery on a particular time and they don’t want to maintain inventory

Inspection delays etc.

This should reflect in Q1 FY16 results.

EURO standard upgrade

EURO-4 to EURO-5 upgrade is required for all refineries by 2020. This requires to de-sulphurise diesel and petrol. Capex of 80000 Cr is expected for PSU refineries. Additional capex for private refineries.

EURO-4 to Euro - 5 by 2017. 7600 Cr Capex expected. (Both were mentioned , need to check)

~10% of above capex will be spent on tubes and pipes. The requirement would be mainly for stainless steel tubes and pipes.

Projections for FY16

Topline might take a hit because commodity prices have come down (Steel/Oil prices).

Expect reasonable growth of 18-20% tonnage wise and bottomline might be okay.

Maintain 18-20% EBIDTA margin guidance

Exports - Gulf, Malaysia

Order book

~380 Cr Stainless Steel, 450 Cr Carbon (down yoy, due to large orders from Gujarat govt last year),

88 Cr for exports (historically very low).

The order book position is as of May 1, 2015.

Due to falling commodity prices, decisions are being delayed as every delay results in gain.

The Gujrat governments’s SAUNI yojna had requirement of 10,000Cr, out of which 6000 Cr was awarded before. Remaining 4000 Cr is in tender phase.

Export Demand

Two big greenfield refineries and coming up in Kuwait and Malaysia which might provide potential orders worth 200 Cr for Stainless Steel tubes.

90% of the products are made-to-order, 10% stock-and-sell (mainly big sellers in US)

Capex

Need 100-150 Cr cape for next 3-4 years. Capex will be used to add additional capacity of 20000T in Stainless Steel Seamless section. Current capacities are as follows - Stainless Steel (Seamless) - 8000T, Stainless Steel (Welded) - 20000T, Carbon Pipes - 350000T (Not fully utilised due to lower demand)

Capex will be funded by internal accruals and for next 2-3 years we will not be taking any new debt more or less.

Maintenance capex is arounf 10-15 Cr every year and it is used for de-bottlenecking or balancing or facility modification to meet customer requirements.

Have enough capacity to handle EURO transition

US Subsidiary

Setup in June last year, intend to be mainly marketing office for US/Latin America. These markets require a local presence due to issues such as insurance, product liabilities etc.

A lot of opportunities due to shell gas pipe in US, we are exploring. Received 10m$ order from Dow Chemicals

Highlights of the Concall by Capital Mkt

Total income from operations rose 20.9% on a YoY basis in Q1FY’16 to Rs 429.8 crore while EBITDA rose 26.8% to Rs 91.82 crore. Bottomline of the company increased 29.8% to Rs 49.92 crore.On a QoQ basis Total income from operations rose 14.6% and EBITDA 44.8% while bottomline was up 54.6%.

EBITDA margin of the company was 21.4% in Q1FY’16 compared to 20.4% in Q1FY’15 and 16.9% in Q4FY’15PAT margin of the company was 11.6% in Q1FY’16 compared to 10.8% in Q1FY’15 and 8.6% in Q4FY’15.Order book stands at Rs 944 crore, out of which order book for carbon steel is Rs 568 crore and for stainless steel is Rs 376 crore.Company outlook on demand is positive as up gradation of existing refineries for processing euro 5/6 fuels would likely entail huge capex by Indian oil refineries, order inflow has commenced from three new greenfieldrefineries in Kuwait/Malaysia/Nigeria, and order inflow in carbon steel business is expected from Gujarat (SauniYojna Phase2), Madhya Pradesh, Telangana& Rajasthan for water pipes

The company is expanding its stainless steel capacity by 10000 tonnes with a capex of Rs 220 crore which wuld be complete by 2 years from now.100 percent of carbon steel and 90 percent of stainless steel capacity manufacturing is against orders only.Order book position is maintained in the range of Rs 800- Rs 900 crore in last few quarters as new orders are taken at lower price realizations due to fall in steel prices. volume growth in order book is higher than value growth.The company is planning to expand its stainless steel seamless tubes & pipes capacity from current 8,000 MTPA to 28,000 MTPA in next 3-4 years with an outlay of Rs 3,50 crore to meet increased demand.This coupled with routine maintenance capex and debottlenecking & balancing of existing capacities, capex is likely to be around Rs 450 crore in next 3-4 year mainly from internal accruals.The company is is not planning any capacity expansion in carbon steel pipes segment due to sufficient unutilized capacity.

Reading the AR for FY14-15, few questions that came to my mind:

A quick google search revealed a lot of stainless steel manufacturers in India (e.g. Apex, Suraj, Aakar, SLS, JNB).

As per SIMDEX (http://www.simdex.com/resources/tube-manufacturers-map/), there are 31 SS manufacturers and 63 CS manufacturers in India alone. The graph also gives good idea about global manufacturers.

So what is it that Ratnamani is doing so well in this crowded space?

How are the steel biggies and steel tube companies related? e.g. Does TATAs and Mittals of the world provided steel sheets to Ratnamani and then they create pipes/tubes?

What are the various steel tube/pipe products? Are all of them easy to make or some of them are very difficult to make?

I have no experience in steel industry at all. Fellow investors who understand steel industry, kindly help. I will try to pursue these questions as well.

L&T

• New plant in Nagor, Rajasthan to service orders from L&T for ~500cr – for water pipelines – otherwise shifted back to Guj,

• 150cr completed, remaining will go over H1FY17

Order Book

• 831cr (278 SS + 552 CS)

• Short-term visibility low, good long-term visibility

• Up-gradation of refineries is going very slow (EURO3 -> EURO6)

• SAUNI second phase – still no progress

• Petronet LNG Terminal

Anti dumping measures not enough

Few opportunities chased by large number of players, might be margin pressure

Capex

• Going Slow on Capex

• Civil work has started for new facility

• Equipment orders will be made within next 1-2 month