This is an interesting appointment that warranted a press release. It shows the importance the company places on the position( a proxy for future growth?). However, a cursory look at the LinkedIn profile shows instability with constant job hopping, with an approximate tenure of less than two years in the last five jobs.

D: Interested, but not invested.

2 Likes

Management Guidance

Rategain:

-

Double REV by FY27 (26 % CAGR)

-

Margins Expansion 150-200 bps

-

Holds over 1000 Cr in B/S

1 Like

I think this stock was treated and priced as a 80% n 40% growth company earlier n since the growth started coming down to 20% last qrtr n 18% this qrtr probably mkt not liking lower growth n higher valuation !! Been brutal! Any views on what company’s target growth rates are?

Maybe it’s due to resignation of company secretary

4 Likes

I am following the stock.

Stock correction in price due to these reasons

1.Loss of business with one Major client

2.Decrease in revenue growth projection for H2FY25 from 20%to 10-12%.

3.Normalisation of travel trend after COVID boom

4.Monitoring agency CRISIL objection about QIP .

And correction is mainly due to valuation.

However management is known for conservative in nature.

Management guided that it won a big deal but can not disclose as deal is not signed yet .

It will work towards increasing revenue

I totally like the leadership under Mr Bhanu

I hold the stock… and may be biased.

12 Likes

Just to add, 70% of the impact has already been seen in Q2 acc to management. I think management is being conservative here. Also given operating leverage, 15% growth would still mean highest PAT growth. I feel 700-750 levels are great entry points

2 Likes

PC_-RateGain_Q2FY25_Results-_Nov_2024_20241111221651.pdf|attachment (681.6 KB)

Philip capital analysis and upgrade

3 Likes

Up and down are part journey of business, how top management is behaviing is important. As DP of Zomato said in one interview - he has to remove some leader as they got too comfortable after ipo.

RG results are bad since last 2 quarters and due to that, instead of possible headwind (trump and possibly revision of hotel ind of USA), management had to cut guidance. Believe 1-2 Q may be challanging but nice to know that management is aware and taking steps.

Disc: Invested and views are biased.

4 Likes

Interesting update:

1 Like

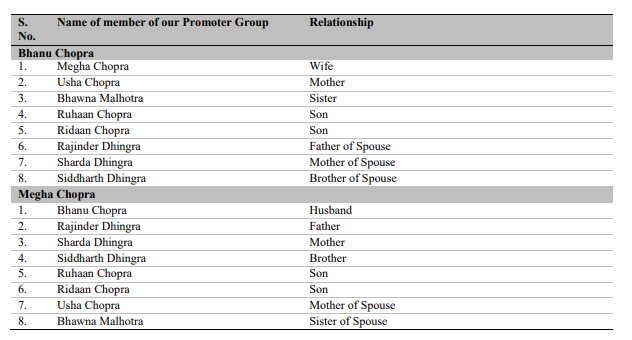

Ruhaan Chopra is Bhanu Chopra’s son and his educational credentials impressive. Hopefully he will bring in some fresh ideas.

6 Likes

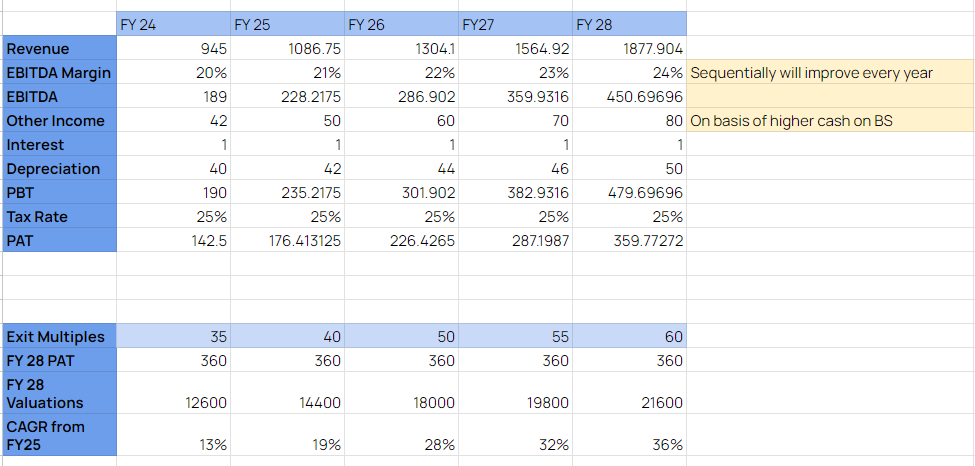

Did some number crunching on Rategain.

I’ve assumed a 15% growth this year and 20% growth for FY26, FY27 before coming down to 15% again without any acquisitions. On a three year time frame, this story will all be about the exit multiple it will be able to get.

You can get access to the valuations sheet here: Rategain Valuations - Google Sheets

4 Likes

Assuming growth rates factored in isn’t the exit multiples considered pretty high?

Assuming they grow at those rates Mr Market will adjust the PE to lower multiples ( <=30) accordingly which will still be a PEG of close to 2 assuming 15% growth

Important takeaway: In past management under guided and over achieved.

Disc: Invested

9 Likes

So I think there are two ways of looking at this.

1. From the Growth vantage: If growth does slow down it might affect the exit multiple, bringing it to the levels you expected.

2. From Business Model vantage: This company is a SaaS based company with large recurring revenues and leading SaaS metrics on LTV/CAC and GRR and NRR.

My understanding is that growth will return in the next 2-3 years, it will go beyond the 15% that they have been talking about. When this does happen, I think the companies will be looked at from the business model vantage and a better valuation could be achieved.

However this is just my view and understanding. It might turn out completely differently.

7 Likes

Wonderful podcast with Bhanu Chopra Founder of RateGain to understand about himself and future ahead for RateGain.

Important point :

- TAM of about $8 billion globally in that they are only able to penetrate around $140-150 million (it’s a peanut

)

) - In future wanted to address the whole ecosystem of Travel Tech spend which is around $90 billion.

- Currently they are focused on the front office softwares eventually they will move to mid office and back office as well(by more & more acquisitions I guess), which will get them to huge TAM of $90 billion.

16 Likes

Significant growth slowdown is a concern.

- Revised Revenue Guidance: Due to delays in closing some large deals, the revenue growth guidance for FY25 has been revised downwards to 12-13% from the previous 15% and initial 20%. This suggests single-digit growth for Q4.

Margins are expected to remain soft next year as per management, FY26 is expected to be an investment year, especially in sales and marketing infrastructure to capitalize on the multi-product offerings and market opportunities.

Equity dilution when they themselves were not clear about Acquisition is turning out to be a bad move. Should have just passed resolution instead of raising the funds and delaying the said cause.

Now the management is saying that higher competition in the travel tech space, with new entrants willing to pay higher valuations is making attractive deals harder to find.

7 Likes

Like a lot of great and worthy Indian tech companies it should have a good history …But these sort of pe multiples are just too high for these uncertain times…

2 Likes

Does anyone know thier unit economics?

Ofcourse lowering guidance and plainly stating that they need “buy” sales by hiring a larger sales team. Co. Stated that they underestimated the number of sales staff required.

Worries me that they come off as desperate by keep hiring sales/ marketing team and just hoping that will solve the problem.

They are not a big company but they sound off as if elections in 70 countries impacting them, etc. This is the reason i was womdering about unit economics? Do they actually have a super bog customer base with little revenue per customer or why would they not abke to grow hotel industry itself is growing?

Any inputs welcome. Invested 1% of my PF and exploring to invest more.

1 Like