Not sure if Rategain will benefit from this trend. They have almost no exposure to the Indian hotel industry. If I recall correctly, India only contributes around 1% of their revenue. Most of their business comes from USA and Europe.

1 Like

Business from Marriott Inter-Continental or a Hyatt, group business in India they have exposure.

Pure Indian hotels use service from STAAH technology.

3 Likes

From Q3Fy24 Concall

What I read from the concall & looking at the STAASH Tech website.

It seems, RateGain is also first trying to penetrate the Indian Hotel segment through the Distribution segment where they will be competing with STAAH tech. It will be great if they are able to gain some market share coz from there, they can slowly bundle other value added services from DaaS & Martech.

1 Like

I hope they are able to crack the India market with distribution, which has been their only segment that has shown signs of slowdown. However it wont be easy with the incumbents. I feel TBO TEK is a better bet if one has to play the India hotel distribution theme, but the valuations are insane at the moment and there is no headroom left for generating alpha.

5 Likes

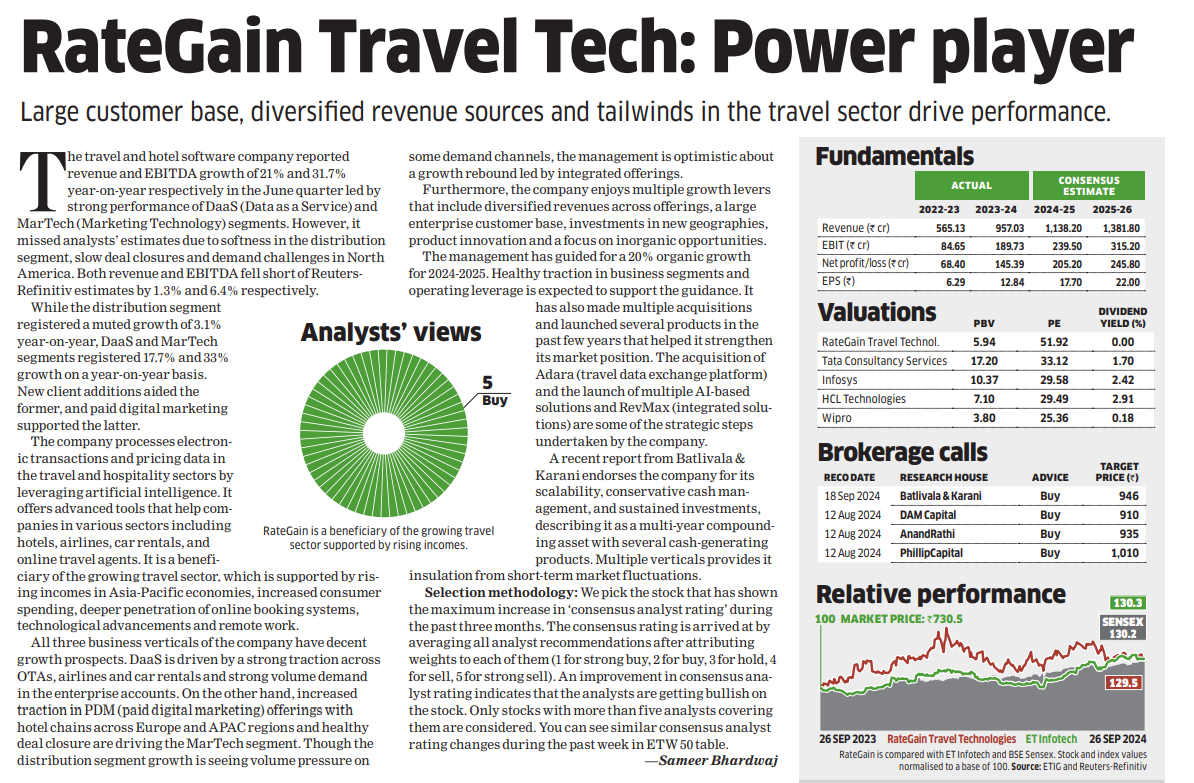

Excellent numbers posted by the company again. Here are a few key points to focus on:

- 40% YoY Revenue Growth

- 69% YoY EBITDA Growth

- 48% YoY PAT Growth

- 60.7% of the revenue is subscrption based

- Strong CFO and Net Cash position

- Net Revenue Retention (% of incremental revenue from same clients compared to previous fiscal) - 113.2%

- 337 new customers added in FY24 (now at 3279 customers in total)

- 11.2% Attrition (down from 21.1% in FY23)

- 285Cr of Order wins (2.2x of FY23)

- 486Cr of Order Pipeline

- 22.3% increase in Revenue per employee

- Contribution from top 10 customers: 28.3% of total revenue in FY24, down from 32.2% in the previous year

- Margins have expanded further (EBITDA margin for Q4FY24 at 21.2% and at 19.8% for FY24)

- Sustainable LTV to CAC range is 12-16

- Long-term cash generation is expected to be 70-80% of EBITDA

- Exits of travel tech players in the hospitality industry globally have benefitted RateGain

- Expect organic revenue growth of 20%

- Growth could be higher if there are any acquisitions

- Adara has a seasonally weak Q4, but Q1 is generally very strong

- Q1FY25 is expected to be higher than Q4FY24

- Working on a new hotel pricing product called navigator

Segmental Revenue:

- 94% YoY Growth in DaaS

- 106.1% YoY Growth in Martech

- Distribution grew at 9%

- Similar trend expected with DaaS and Martech leading the growth

Disc: Invested

5 Likes

what I really like about Rategain is its world leader and innovative quality…in my honest opinion most LISTED indian IT companies are just doing bread and butter stuff(nothing particularly exciting) and mainly they just service the west because they can do things cheaper than in the west…Also most of rhese are very vulnerable with the advent of AI

But with Rategain there is not a lot of competion and they are very innovative

Who knows whether it is cheap or expensive though but its a company that India inc should be wholly proud of.

6 Likes

Here’s the interview of Bhanu Chopra about the Guidance, M&A and the road ahead.

5 Likes

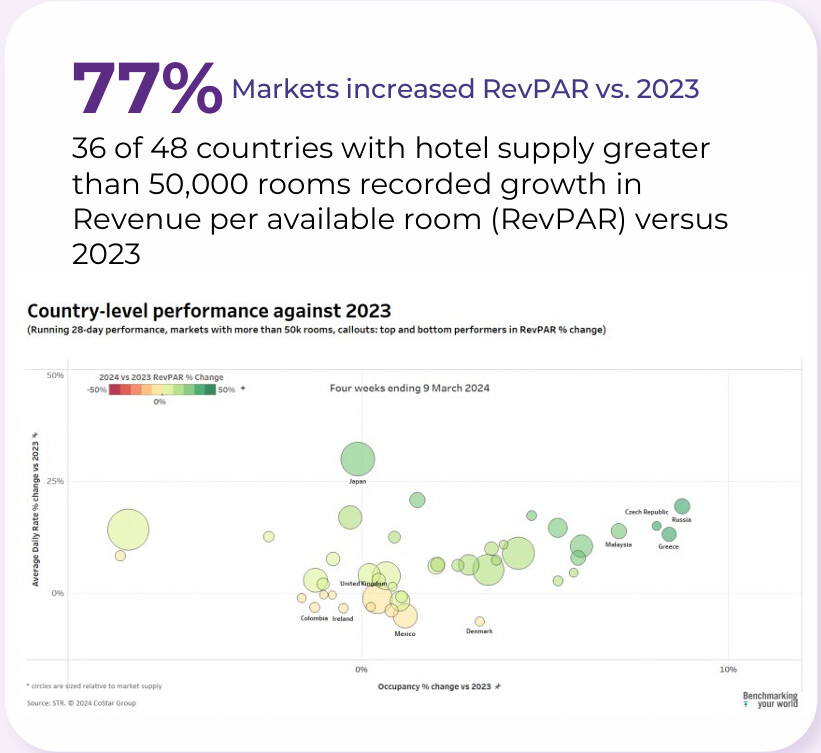

Hotel industry insight from RateGain PPT.

Not just India, but 77% of the world is experiencing surge in hotel prices.

7 Likes

I stopped tracking this since I sold it in Jan 2024, as i needed cash (it was a doubler for me). However, I wanted to revisit this again so went through its results and investor presentation today. Still looks like a solid business! It continues to be an innovation mindset based firm. Some of the key reasons that got me interested in this were opportunity for small to mid cap expansion, less competition, high margins, using money well for revenue accretive acquisitions (ex: Adara), TAM is huge (recently entered airlines also), asset light model, competent management which has been delivering good results. Price action wise also it seems like it underwent decent consolidation for almost 10 months with good support at 650 levels. Looks interesting ! Thoughts?

Results for the quarter ended 30 June 2024: Revenue grew 21% YOY and PAT 82% YOY

https://www.bseindia.com/xml-data/corpfiling/AttachHis/bb7235ea-fd05-4808-a515-6004603cef0a.pdf

The audio recording of the earnings conference call:

Investor presentation

https://www.bseindia.com/xml-data/corpfiling/AttachHis/8fa0fa0e-38cc-4755-8072-92f2bb46fcae.pdf

7 Likes

I heard somewhere on youtube that rategain is doing more acquisition led growth as compared to organic growth. I am not really sure as I am yet to analyze this stock, but if yes then how sustainable is it in longer term?

1 Like

Careful - the PBT was a big beat mainly due to high other income. I’m not sure if core business is growing fast for the valuations to sustain

thanks for the headsup, will look into it soon.

1 Like

This was mentioned by Ishmohit on SOIC channel recently that he did video on Decoding PE

1 Like

One thing I would like to point out that, Mgmt had guided for 20% rev growth in Q4fy24 and did achieve that guidance, despite some issued faced by the mgmt.

^ One of the Expedia partner sites is getting consolidated & it was a big volume generator for us. And so, as a result of that strategic direction, we are seeing those volumes get reduced on one of these OTA sites.

^ One customer, renegotiate the pricing , because of the larger volumes we had to discount. We usually do not entertain, volume discounts. This was a one-off case where it was a, very large customer & the footprint that we have with them is quite significant. We had this one contract from DISHCO acquisition, where we were charging significantly & given the importance of this large customer, we had to entertain lowering the price. I don’t see this as a systematic trend.

^ On Martech, we had like a big large chain that bought like a mid-sized chain, which was a customer for us on the Martech side. So, we’ve seen some bumps.

Had these issues not been there, I think they would have achieved higher revenue growth.

Disc: Invested & Biased.

8 Likes

Note from AGM:

Outlook: The goal is to double the revenue from FY 24, in the next three years by FY 27. So We’re on track. As you have seen, the growth in Q1 has been pretty healthy at 21% and organically and inorganically combined to get to the goal of doubling our revenues entails about 26% CAGR and we’re confident that we should be able to achieve that over the next three years.

Margin expansion: what we have guided for in previous quarterly earnings is about 150 basis points to 200 basis points expansion. So we’ve been at about 20%. So, we should see that kind of expansion in our EBITA margins over the course of this fiscal year.

Microenvironment: global travel industry continues to hold steady in the face of the evolving situations in some pockets and, the SCIFT travel index that we follow continues to hold steady at 104 in June. With key geographies within Europe witnessing a strong summer season and Asia Pacific still witnessing some healthy tailwinds being one of the last geographies to open up. The hotel industry growth continues over 2023 levels buoyed by improved occupancy. Recent surveys conducted by leading global consultancy firms have highlighted that recreation and leisure travels continue to be at the top of the list for discretionary spend for consumers demanding a higher share of wallet and kind of reaffirming the outlook for the travel sector in terms of the next few years that there are some healthy tailwinds for growth within this space. So overall things are holding quite steady and within that, customers continue to drive investments into the industry. It opens new opportunities for RateGain to be able to further consolidate its position over there.

Other was on M&A.

10 Likes

why is the company not giving dividend?

1 Like

Probably…because their receivable are rising that too when no increase in debt level.

May be waiting for opportunity to buy some small companies for expansion.

1 Like

I could not correlate