Some really bullish commentary from the management !!!

Some really bullish commentary from the management !!!

Disc: Portfolio update

Started buying- Aarti Industries and HDFC AMC today.

Reason- Both have had short term negetive events.

Termination of a long term contract in case of Aarti and de-growing SIP flows in Apr, May in case of HDFC AMC.

Long term, I think these challenges are completely manageable.

These events have also resulted in some pressure on stock prices ( not that they are cheap, but are not as expensive as they were some time back )

So…took up small tracking positions.

Current portfolio holdings ( portfolio wt in decreasing order ) -

HUL

Britannia

Dabur

Nestle

Colgate Palmolive

Alkem Labratories

RIL

Divis Labs

Alembic Pharma

Aarti Drugs

Ajanta Pharma

GCPL

Marico

GAVL

Sun Pharma

Lupin

Aarti Industries

HDFC AMC

Some hits- Timely entry into - entry Aarti Drugs, Alembic Pharma and RIL

Some misses- Reduction in portfolio wt of GCPL, Marico ( both have been on a tear post reduction )

Regards,

Ranvir Dehal

Hi Ranvir, when and why did you exit GCPL? My reading is since the change of guard at Godrej, there would be lot of senior management trying to prove their mettle and hence the performance can be better in the coming quarters… Product portfolio wise Godrej has and keeps adding new products while we dont see that from Colgate… Its just toothpaste mainly and dont see any large increases… If both are available at similar valuations why do you have more allocation to Colgate? Colgate can be more stable but you dont seem to be the buy and hold investor, seeing how quickly you got out of financials before the actual meltdown…

What is your strategy on pharma - Are you playing it as a momentum pick, the sector in demand to ride the tide or is it a long term conviction pick for next 5-7 years? Also, no MNC pharma - focus seems on export oriented players? There are many pharma names in your portfolio. I remember you mentioned each FMCG company is unique and I resonated with that - I mean the trajectory of biscuits, coconut oil and fairness cream cannot be same and so for the company…Do you feel it is same in pharma and is that why you chose the ones you choose? Can you give some details on your rationale for each pharma pick? Thanks!

Hi…

I did not exit GCPL, Marico. I just reduced their portfolio weight…which in hindsight has turned out to be a mistake.

I did so…because I wanted to keep some cash in hand…as the news flows these days is kind of scary. Also, among the FMCG pack…I wrongly assumed Marico and GCPL to be less resilient vs say HUL, Dabur , Britannia etc.

I never kept cash right from 2014 to March 2020. However…these days, I am tempted to keep some.

Dont know if its the correct thing to do or I am playing the prediction game. But…it is giving me peace these days…I must admit.

Next…

I always believed that I was a buy and hold investor.

But the lockdown situation made me panic on Financials…I must concede.

I did not sell FMCG, infact only added them…so thats some solace.

On Colgate…

I bought it at around 1150 -1200 range. Now I am tempted to not sell it as I expect the business to be largely stable.

Regards,

Ranvir Dehal

Hi…

Since I had sold all my financials just before the lockdown, I wanted a sector to deploy the cash…so zeroed in on Pharma.

But I was late to act…I must confess.

I am no Pharma expert…I must admit. So, I decided to not make concentrated bets, unlike in FMCG.

Amongst the Pharma names, I did not buy MNCs just because they command higher valuations.

I am most comfortable with the API manufacturers like Divis Labs, Aarti Drugs.

Also read a lot about the generic players like- Alembic, Alkem, Ajanta, Sun , Lupin etc. What I could decipher was the following-

The pricing pressures in the US mkts are not as fierce as they were a few years ago.

Indian companies over a period of time have become far more compliant with the regulatory requirements. The ‘CHALTA HAI’ attitude which invited a lot of USFDA led trouble- is hopefully a thing of the past.

USFDA has become a little more accomodative specially after the China Virus episode.

I expect India - US ties to be resonably good going forward as the US-CHINA trade war is only heading towards a Cold war. ( Thats only an assesment. I am a Defence Officer…so thats an informed opinion. But…its an opinion nevertheless)

If there is one sector where India has all the front end requirements to be a global leader, its Pharma. We are already a Generic powerhouse. So if there is one Industry that should shift out of China and India already has all the Front end requirements…its the API manufacturing industry and that would complete the entire value chain. This is again an informed opinion…nothing more.

Alkem, Alembic and Ajanta- are amonst the ones that have had lesser USFDA troubles in the past. Alembic and Ajanta are also widely discussed on this forum. So…this nudged me.

Theory behind SUN, LUPIN - The next wave of drugs going off- patent in the US are complex generics, Injectables and Bio similars. Sun and Lupin have already spent a lot of R&D dollars in complex generics and injectables. Plus, making them is actually R&D heavy which most Mid Cap pharma companies may find difficult to manage. So…I thought it would be wise to buy some large caps as well.

So thats the broad rationale…as u can make out- its a broad brush kind of approach.

Regards,

Ranvir Dehal

Thanks for the update @ranvir

You always seem to be a very intuitive kind of investor who in interested in the story of a company. And if convinced by the story then hold the company for long term. Usually you seem to invest in the safe compounder bets for long term.

My question is how much do you dig into the financials of a company to understand to the intricate details and value a company?

Similarly I too liked ajanta, alembic and dr reddy on same note .

Hi…

I do read up on the financials…thats important and thats the starting point.

But I dont dissect them. Or… I dont go to forensic levels. At times, I am too lazy to do so. Sometimes its simply beyond my competence. Thats also one reason that I generally dont buy into small caps. To be sucessfull there, one has to go far deeper.

A lot of seniors at Valuepickr do that regularly and I admire them. Sometimes I try and follow them.

But…on my own, I stick to large, bigger Midcaps where I am comfortable with the Corporate governance so that this limitation of mine doesnt remain a limitation ( in most cases that is … )

)

Regards,

Ranvir Dehal

I agree to almost all your points, specifically on ease of doing business for these export oriented pharma companies with better approvals expected goin ahead. When you talk about complex generics, injectables etc. Where do you see or compare a cipla and dr Reddy ( bigger midcaps) with lupin and sun ( large caps)?

Also, the MNCs with excellent domestic portfolios of medicines, OTC, good balance sheets and vaccine portfolios for some of them, which will become more relevant…don’t you think their premium is justified just like that of a HUL/Nestle in FMCG?

Lastly, I am not sure about this point…do these mnc pharmas launch their global portfolio for India or they keep them seperate? I mean do these have an edge to launch new products by leveraging the r&d strengths of their parents…and also just like captive IT of mnc corporates in india…what stops these MNCs to make their captive indian subsidiaries as their generic source which will be win win for these and US would get a pie of generics business as well through these subsidiaries… Thanks

Hi…

Thanks for the feedback.

I am, kind of interested in MNC pharma stocks like Abbott India, Sanofi India…however I have not yet developed an understanding deep enough to pay for the premium valuations.

For eg- In domestic mkt, some of the prescription and OTC brands of Sun, Cipla, Alkem etc are as good as those of Sanofi, Abbott.

If Sun, Cipla, Lupin, Alkem and other domestic pharma companies were to list their domestic and intl business separately, I would guess they may see similar multiples as MNC pharma on their domestic businesses.

That said…the Indian domestic Pharma business is actually very close to being an FMCG business provided there are no major regulatory shocks going forward.

The only thing that needs a deeper dive is the extent of integration in the operations of MNCs and weather they bring in their blockbuster drugs to India through their listed subsidaries. ( as brought out by you )

Frankly, I am myself in the process of finding these things out.

If anybody can throw some light here, it would be really helpful.

Another thing that I am yet to fully ascertain is the extent of Backward integration ( API manufacturing capability ) that each of these companies ( Indian Pharma I mean ) have. The more the better…I would say, due to the ongoing issues with China.

On Cipla…I guess, its in the same boat as Sun or Lupin with one major advantage and disadvantage.

Advantage- Better regulatory compliance track record, far better India portfolio…next only to Sun, amongst all Indian Pharma.

Disdavantage- Never been a growth hungry company…thats an impression

Dr Reddy, Aurobindo- Not studied much…so wont be able to comment except that both are largely export oriented and have much smaller Indian portfolios.

Regards,

Ranvir Dehal

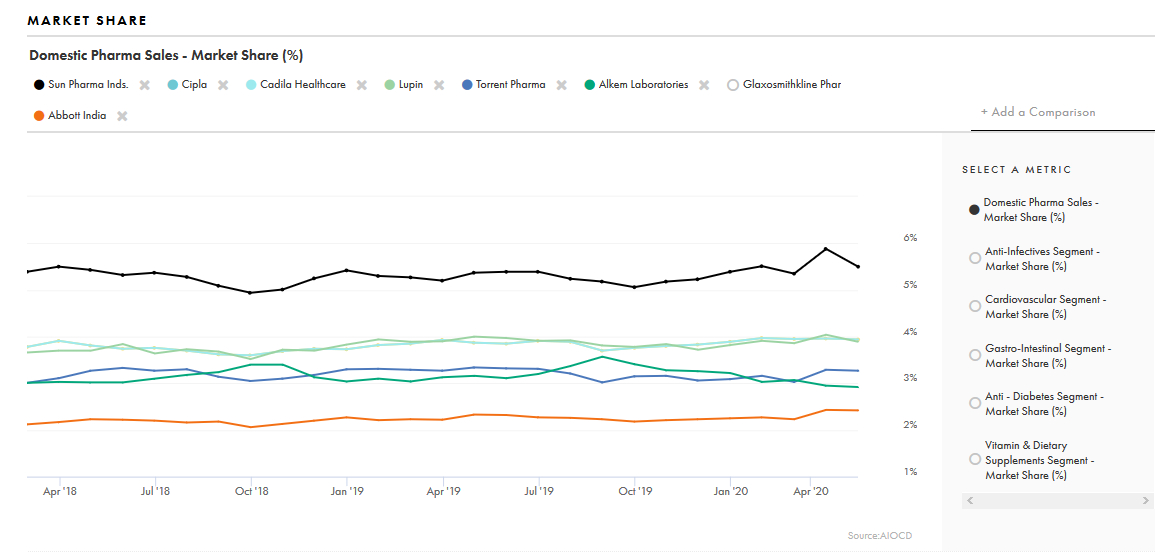

Global ranking of Generic pharma companies by sales ( in decreasing order ) -

MYLAN

TEVA

NOVARTIS

SUN PHARMA + TARO

PFIZER

FRESENIUS

AUROBINDO

LUPIN

ASPEN

AMNEAL

SANOFI

APOTEX

DR REDDY

STADA

SAWAI

ZYDUS CADILA

Indian Pharma rankings in Domestic market ( in decreasing order ) -

SUN PHARMA

ABBOTT + ABBOTT HC + NOVO

CIPLA

ZYDUS CADILA + BIOCHEM

LUPIN

MANKIND

ALKEM + CACHET + INDCHEMIE

TORRENT

INTAS

GSK

SOURCE- Sun Pharma’s investor presentaion.

Disc : invested in Sun Pharma, Lupin and Alkem ( amongst these ).

Sharing, just for info. No recommendations.

Data from AIOCD Pharmasofttech AWACS Pvt. Ltd. doesn’t match with it. The graphics is from Tijori Finance.

Update: Sun Pharma IR shows “Abbott + Abbott HC + Novo” as number 2, not the listed Abbott only.

Yep…ammended the previous post now !!!

Disc: have been reading about Laurus labs for the past few days…both the company reports and the VP thread.

Have initiated a tracking position.

Disc: have initiated a tracking position in Syngene International. ( I know, I am late here. However, I intend to add more if price corrects from here )

Also- added Godrej Agrovet, Aarti Industries and Vinati Organics.

Godrej Agrovet-

Liberalisation in the agri sector should further allow GAVL to really dominate the Palm oil space . But…thats a long term thing.

Steep recovery in the broiler prices and steep fall in corn prices should aid the animal feed margins.

Astec life, their subsidiary seems to be doing well.

The share of value added processed milk products is continiously growing in their dairy business.

Their Bangladesh business was always doing well.

I am hopeful about improvement in the company’s fundamentals going forward.

Aarti Industries and Vinati Organics -

Speciality chemicals is a fancied space and Aarti, Vinati are two prominent players.

The recent termination of Rs 4000 cr contract is a near term set back for Aarti Industries ( however they are being compensated for it ).

This short term negetive is hopefully a good entry opportunity in a quality company like Aarti Industries.

Subdued near term demand for ATBS, one of Vinati’s main product is keeping the stock price capped. Again, I think near term challenges can be used as opportunity to accumulate.

This is not a buy/ sell recommendation.

Just a Disclosure !!!

I had invested in this stock couple years back as a core holding but sold off just before the crash. I see diversification as an issue with this. Over time I have also realized to invest only in focused players. I must not invest in a diversified play if I like Palm oil or crop protection part of their business as every Q, one of them used to do well while other performed very badly so there was 0 growth. I gave it a pass in the crash also and instead added more of GCPL among the Godrej.

Pls note above are my thoughts and I may be wrong in my assessment, just thought to share…

Hi…

Same here. I also used to own it but had sold it in 2018 after making some minor gains. Reasons for selling were the same as u just brought out.

Reasons for re-entry -

Price correction…although it is still not in the bargain zone.

Familiarity with the business.

Confidence in the Management integrity.

Bullishness on Astec Life…their subsidiary.

The central govt has been taking some bold measures as far as the Agri space is concerned. The ammendments in the Essential commodities act can be a game changer for companies with rural focus- as it may open up some really big opportunities.

However, I intend to keep its portfolio wt on the lighter side as I need to see the performance flow though, before the allocation can be increased.

Regards,

Ranvir Dehal

agree, but what makes you feel that it would perform better than a GCPL (comparing only Godrej group) bought at equally bargain prices in crash. Rural play will push GCPL insecticides sales, low price SKUs etc etc. so why not increase allocation to a much more sure winner in our good old FMCG than say an agri/chemical diversified play? Agree Astec would have been great pick in crash as a focussed play, if only had that conviction and in active watchlist then…

I agree with you as far as GCPL is concerned.

The thing is that post the Nifty rally to 9000 levels ( up from 7600 levels ), I had trimmed some of my portfolio…and decided to keep 30 pc cash ( for the first time in my life )

Those were confusing days.

In retrospect -

Selling out of financials before the big downturn was a good move. But converting 30 pc of stocks into cash, anticipating another down leg after the rally back to 9000 on the Nifty was …kind of dumb.

Now, I am slowly deploying that cash in the second best companies ( in my perception ) that I may find.

FMCG is my first love and my greatest conviction. However, I am not a buyer in FMCG at current levels.