I recently joined this wonderful forum as a member. Prior to that, as a guest, I was going through the plethora of information present here from so many knowledgeable persons. Kudos to the moderators and nice folks who have made the forum so robust and full of information.

I started investing into direct equities from 2017. My investment objective is to have a moderate 10-12% of CAGR with my portfolio which I’ve failed to achieve. Although I’ve learnt some valuable lessons within this short stint of time. One major lesson will be - “Concentration creates wealth, while diversification protects wealth”. I’ve always noticed in hindsight that if I would have allocated more to certain stocks, I’d have been more profitable. Also I’m yet to figure out an exit strategy for my stocks.

I am interested in adding few sectoral tailwinds(e.g. pharma, specialty chemical) to the folio to take advantage of the current situation. At the same time, I’m fearful of a cluttered folio. I want to keep the no. of stocks in my portfolio in the range of 10-12 with a bias to low beta.

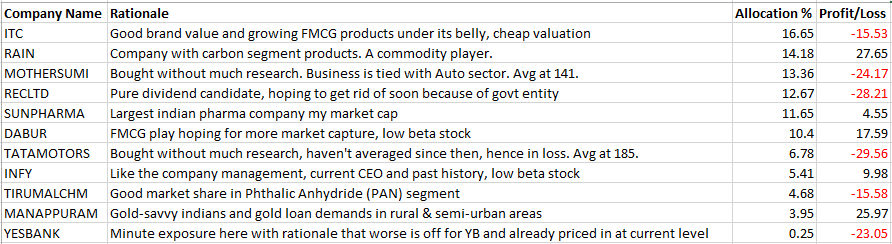

Below is a snapshot of my current holdings. Open to any suggestions, criticism or inputs from senior folks and fellow members.

As your return objective is moderate at 10-12%, I think you can easily get that by investing in 10-12 leading companies of secular growth sectors. You can invest in “coffee can” type of stocks instead of stocks like Rain, Motherson, REC and Tata Motors. Some of the stocks that come easily to my mind are HDFC Bank, Kotak Bank, HDFC AMC, Nestle, Britannia, Marico, ITC, Abbott, Titan, Asian Paints, Pidilite etc.

Disc: Please note that I am not a registered investment advisor and the above list is not a recommendation. Please do your own research before investing in any of them.

I hold HDFC Bank, Abbott, ITC and Britannia in my portfolio.

Thanks @anirband87 for chiming in. Appreciate your input. I agree with your point of “coffee can” style of investing. However, I’m already large cap heavy on mutual fund side of my portfolio. I’m also invested majorly in Nifty 50 Index fund which captures all the top heavy-weights I believe.

On a second note, what should be my exit strategy on stocks like Rain, Motherson, REC and Tata Motors. I’ve been eyeing on these to exit but have not been able to devise an exit strategy here. As shown in the portfolio snapshot, these stocks are in losses. So should averaging down into further be my next step. These stocks are said to have a cyclical element to them.

I will share my personal take which I hope will help you form your own exit strategy.

In most cases when I enter into any stock, I already have a pre-defined stop loss. Also, I never put all my planned investment in one go. eg: If I plan to invest Rs. 100 in a stock, I will probably buy Rs. 50 in first leg and have a predefined stop loss. If stop loss is hit, I will get out. Else, I will gradually add more on the way up. This helps me sleep well and help continue to hold on to a stock for a longer time when its in green. I almost never average down losing stocks. I have few exceptions, but I follow this 80% of the time.

What works for me may not work for you. So, you will have to form your own strategy.

I am curious to know that when Tata Motors hit 60 odd levels in Mar-Apr this year then what stopped you to make additional purchase. You could have made 100%+ return on laggards like Tata Motors. IMO you need to keep flexibility and keep on fine tuning your strategy for better returns and control risks on overall PF. The advice of anirband87 is apt and to the point at the moment for you.

I don’t think you should device an exit strategy based on portfolio gain or loss. What you are calling loss is a 30% correction which can happen to any volatile stock. Check annual volatility of your stocks in tickertape screener to confirm.

You are right about some of your stocks being cyclical. Best time to sell a cyclical is when everything looks good. Earnings increase leading to low pe. Best time to buy is when earnings decrease with high or negative pe.

Regarding Tata motors, they have announced plan to become debt free. Rakesh Jhunjhunwala has recently entered the stock betting on debt free story.

Do individual analysis of the stocks and ask one simple question. Will I be comfortable buying this stock after it has fallen 50%? If the answer is yes then buy or hold, if no, then sell or ignore and move to next pick.

Just one addition…some of these coffe can mid/largecaps named above can disappoint in being within 10-12% CAGR range as they might surprise you on the upside they can offer, so be prepared. Thanks

Thanks @Vijay_Kiran for the input. In Mar-Apr lows of Tata Motors, I went pessimistic on it considering that auto sector will be the last one to recover the covid pandemic situation, that too for a company with lots of debts at the moment. Hence I got hesitant to average it out and skipped altogether. Looking at hindsight now, yes, I could’ve made some returns had I done that. I’ll take it as a lesson and as you said, will work on the flexibility and fine tuning of strategy.

Those are some nice feedbacks @akash_das. Thank you for chiming in. I’m currently studying on cyclical industries(VP thread), trying to figure out how they play out for investors. Do you have any recommendations or resources to understand the cyclical plays? Would love to check out.

Regarding Tata Motors, since the announcement of plan to become debt free, the conviction is to hold it for now and average it out. Hoping for the best.

Thanks for the pointer @Investor_No_1 here. When you say these type of stocks can disappoint, do you mean they would be in slow and steady return range? I think I’m missing context here in between words. Would you mind to elaborate. Thanks.

I don’t invest in cyclical stocks due to my buy and hold style of investing. Some insider edge is also required like sales volume, inventory reduction to time entry and exit in cyclicals. If you are involved in cyclical business you might have an edge. There are thread for cyclicals in vp. Links below. For detailed analysis of a cyclical check the rain industry analysis.

What I meant is that whenever any investor targets a modest, reasonable and inflation beating 10-12% CAGR returns, I have seen many direct them to steady compounders like HDFC Bank, Asian paints, Pidilite, Marico etc. Here, the one targeting and suggesting should be ready to be disappointed as for most, chances are returns would not be in expected range and can surprise on upsides. The disappointment is educational and not literal here.

All these have been highly valued (high PE) companies since long time. Now if you do simple maths and do a CAGR calculation for last decade (Oct 2010 to Oct 2020, not even considering the buy in dips strategy for then I would have taken CAGR from lows of 2008-09) and see the CAGR for these otherwise thought as slow growers and meant for those who do not know to analyze stocks and who target 10% returns -

HDFC Bank (18%),

Asian Paints (24%),

Pidilite (27%),

Marico (17%).

And imagine the CAGR if the person would have bought quality businesses at dips of 2008-09. Imagine the div yield today for that invested sum and consistent growth even for a risky Financials business which is out of flavor today.

Disc: Hold stocks mentioned above, not a buy/sell recommendation. Past history is no sign of future returns. Post is only for educational purpose and my own understanding of long term returns.

This is much clearer. Thank you for taking time to elaborate on the context. Would take some time to allocate my capitals towards these type of companies for steady growths.

On a different note, do you have any advice on stocks like REC (Rural Electrification Corp Ltd) which is a PSU company. From whatever I’ve read till now, it has been the conclusion that Govt entities have been wealth destroyer year by year. Again REC is an NBFC entity. The original conviction here was to hold it for pure dividend gains with a moderate growth story.

ONGC had been one of my first picks when I started investing. I still remember ONGC, RIL used to be neck to neck on market cap, TCS a third slot and there used to be headlines whenever one crossed the other in mcap…Fast forward a decade, RIL is almost 14 lac crore, TCS is 10 Lac crore and ONGC is 81 thousand crore. A beautiful business destroyed immense wealth. Dividend yields are almost everytime value traps. My recent mistake is ITC (not that I did not want to buy it but that I wrongly bought it for the yield and I should have waited to get in at a better price. The div yield trapped me at a higher price than I should have bought it). I think, as much as possible, we should look at dividend history and dividend growth of a company only to see how it shares profits and never base investment decision on the yield. If you need income today, dont put that money in stocks and depend on their yield…a good business would give you a better yield few years down the line. Personally I refrain from PSUs, was lucky to get out of ONGC at right time, not intentionally but I needed some money then…since then I have never looked back at PSUs no matter how attractive they look. There will be a time when they are actually valuable but which ones and when, I don’t know and its not worth the efforts and risk when I can see such other good businesses around…

Hi Ranjan - I have been in direct equities from long time and my single biggest learning for someone with a full time job is to just regularly SIP into index fund. There is something called return on time invested - if someone can better invest that time in professional career growth, family, health – nothing like that. Most important capital is time. Since you are looking for realistic 10-12% of CAGR, index funds fit in well. I myself have been shedding my direct stock portfolio from April onwards and looking to invest lump sum into Nifty, Nifty Next 50 and select coffee can type largecap companies once the overall valuations cool down. Am willing to be patient and wait out a few years in worse case scenario.

I would get rid of Mothersumi since they seem to just pile on debt with their m&a activities, not sure if there is any corporate governance issue there. Also would get rid of Yes Bank. Rain at least you are in profit, lot of people entered because of Mohnish Pabrai’s position. I would just concentrate on largecap stocks if my target is moderate returns with low drawdowns.

Thanks for the inputs @bhaskarjain. Couldn’t agree more on your statement-

Most important capital is time

I’ve observed this with my portfolio with these 4 stocks losing time value of money- TaMo, Motherson Sumi, REC and YB (at one time, I had 80 shares of YB@Rs.300, was lucky to get out of it before the debacle). Looking at hindsight, I think it would have been much better if money just left in coffee can style stocks.

I would get rid of Mothersumi since they seem to just pile on debt with their m&a activities

I’m of the same opinion here as the debt part is really dragging the company along with ongoing m&a activities. I believe it would take a while for the company to get things in order.

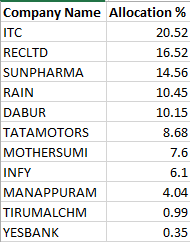

Reduced allocation in Mothersumi, Rain, Thirumal Chemical at recent peaks. Waiting to complete de-allocate Tata Motors and REC. Current portfolio gains stands at +17%.

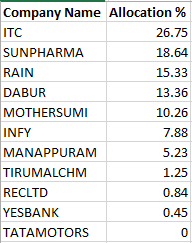

Sold all of Tata Motors stocks and reduced allocation of REC significantly. Now the goal is to add some market leaders/large caps(with lower beta), few sectoral tail-winders(pharma,specialty chemical) and keep adding the existing stable stocks in portfolio. Waiting for some good entry points. Current portfolio gains stands at +33%.

I would suggest please add below few stocks in your core compounding portfolio for next 5 -10 years-

HDFC AMC: Mutual fund penetration in US is almost 30% or more but in India still at nascent stage. So this AMC will be a value creator going forward. I’m investing in this in SIT Mode.

HDFC LIFE: Same thing here too. Slowly people will understand the value of term/life insurance going forward for all kinds of income level.

Thanks @anindya001 for your inputs. Appreciate it. HDFC life is in my watchlist to enter and I resonate with your rationale on this. I need to study the other two, hdfc amc and akzo nobel, to understand their businesses. I’m fairly new to direct equities, hence gradually building my portfolio.

My current watchlist: Hdfc life, Asian paints, Tata consumer, Reliance, Kotak bank, Dmart.