Q4FY23 NOTES:

• First in the Industry in India to manufacture Rigid Barrier Packaging Products with completely integrated facility under one roof using state-of-the-art European Machinery.

• Received 4 design and process Patents. (In Tube laminates segment)

• 33% Volume growth Q4 yoy.

• Ebitda per kg for fy23 – 30.5

• 45+ products added. 200+ no. of customers added in fy23

• Capacity expansion – Thermoforming – 8770 to 9770 MT – 3cr investment – to be added by dec23

• The sales mix on the product category as compared to the previous year:

- Rigid sheets is Rs. 56.7 Crores as compared to Rs. 56.7 Crores in the last year.

- Packaging product has increased from Rs. 126.8 Crores to Rs. 167.47 Crores.

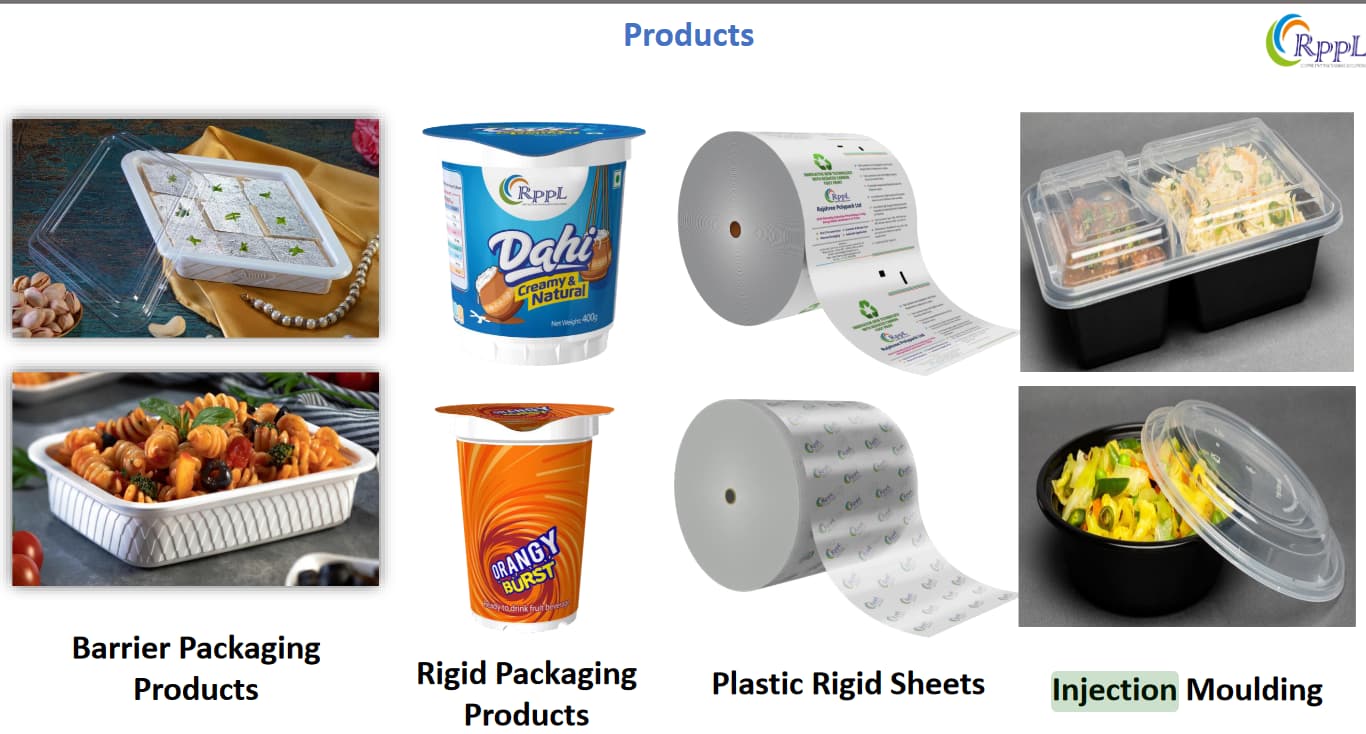

- Barrier packaging has increased from Rs. 6.34 Crores to Rs. 23.85 Crores

- Injection molding, started in this year, has achieved sales of Rs. 4.5 Crores.

• “Growth in manufacturing business require consistent investment in capacity enhancement and we are not the exception”

• 15% to 20% revenue growth possible from the existing capacity. FY24 Guidance: On the revenue side, we are looking at somewhere around 15% to 20%. That is what is available from existing set up. So that’s what we are looking to achieve in this particular year.

• 180 to Rs. 200 Crores sales capacity from Olive Ecopack – 1.5-2 years needed to ramp up – Commercial production by Nov 23 – 20-25cr sales his FY

• 15% is stable/Sustainable Gross Ebitda margins for Rajshree. 13-15% for Olive

• Electricity cost has gone up across which has increased our manufacturing cost. That is probably one of the reasons for also increasing to the manufacturing cost and little reduction in the margins. So that’s a major factor I would say that has contributed.

• Capex Guidance for FY24 – 4-5cr in RPPL, 10cr in Olive Ecopack

• Barrier Packaging: We have done around Rs. 20 Crores to Rs. 23 Crores of sales in FY23 and we look to do around Rs. 32 Crores to 35 Crores in 2023- 2024.

• Olive ecopack customer acquisition details: “Yes, I would say that the product is new, but the customer are common for this particular segment, for few of the customers which are in QSR segment and also for our partner who are in this segment. So we are already in touch with the customers both at the domestic level and at the overseas customer. And so we don’t need to hunt for the customers, I will say. So we know the customer, we have identified the customers, and in fact, the product range is being developed in consultation with the customers. So we are optimistic on achieving the numbers for this category as we come up with the production.”

• Debt reduction: “As I mentioned, like Rs. 11 Crores is what we have to invest, out of which Rs. 4 Crores we are going to invest from the money which has come from preferential issues of shares. So balance Rs. 7 Crores and Rs. 5 Crores, Rs. 12 Crores is what we look at the total CapEx in this particular financial year. And so whatever other cash flows we’ll generate in this year, we’ll be able to definitely bring down our short term and long term debt at least by one third at the end of this financial year.”

• Customer stickiness: “I will say this is a primary packaging material which has to be used onto their filling lines. So the products are designed as per their filling lines. So generally, the customers don’t change or switch to the new vendors unless we do go for unless our prices are way beyond the market standards. So we have seen that our customers are with us, stick to us for a long period of time.”

“Once you acquire a customer and then they ramp up whatever business with us, then that remains generally steady, right? - Yes”

• “I would say like it’s a chicken and egg situation where whether we keep on investing because we have already done a lot of Capex in last two years, so ideally, we would like to consolidate for a year or so at least in this particular segment and then we look for further Capex.”

• As we add up more barrier packaging sales to our overall revenue, we can definitely see the consolidated EBITDA numbers to go up in near future.

• Generally, the Asset turnover is we are looking at 2.5x. and we operating roughly at 15% EBITDA, so that’s equation with the industry we are working in right.

• Barrier packaging film is basically for the sweet industry, right? It’s basically for food industry wherein to increase the shelf life of the food

• Barrier Packaging Industry India: What is the current potential there in India? - The overall market at the moment is roughly at around Rs. 100 Crores - Rs. 125 Crores will say, which was almost negligible five years ago. So this is a new technology and segment which has come up and with the more and more food processing plants coming up and addition of the new processing technologies with the sweet manufacturer and the food processing unit, we will definitely see a growth in this particular segment.