I believe it is my ethical duty to inform that I have exited my investment in the company. When I first wrote about this company in Jun, valuations were very comfortable and hence it was a good investment case.

Stock price has since doubled and while there is nothing wrong fundamentally with the company, I believe the current price does not offer enough margin of safety and current valuation may be unsustainable.

The company is now in my watchlist.

Admin: Please delete this post if its not required

All I can say is that a proxy FMCG business which should grow to 230-250cr topline with full utilization of current capacity in 12-18 months at 15-16% EBITDA margins is available at 1.2x sales or 7.5x EBITDA multiple even after today’s big upmove.

Valuation is subjective, for some this offers no margin of safety - to me this is close to a bargain.

Hi, when you say valuations are unsustainable what parameters do you consider? Can you please elaborate? It will help new understand how your valuation parameters differ from @sahil_vi .

Everyone has their own valuation parameters. I entered the stock at around Rs 80 and built considerable allocation around the time of writing this post on VP, it delivered ~3x for me in a relatively short period of time.

Happy with my returns and find better opportunities so moved the allocation there.

For me earnings triggers are a key criteria, they need to raise their capacity utilisation significantly to make incremental returns. I do not foresee that happening within next year, whereas existing companies in my PF have incremental earnings triggers for next year.

Like I said, there is nothing fundamentally wrong, it is a good proxy bet on FMCG sector. I just am satisfied with my returns.

So the flat revenues we see for last 3-4 years are majorly due to less capacity right? Because they took ipo funding for capex and that wasn’t possible in 2019 and then in 2020 covid arrived and their plans delayed. because if we check 2020 capacity utilisation, we can observe that they are running at full capacity and actually can’t meet the demand and hence now as they finally doing capex i.e. utilising the ipo Money, we can see revenues going up substantially!

Correct me if my understanding is wrong

• Operational Ebidta per kg = up 25% YOY, 36.2% QOQ – 37.58rs vs 30rs vs 27.59rs

• Volume growth = 23.57% YOY, 24.5% QOQ - 2804 vs 2269 vs 2253

• Likely to maintain or improve current qtr. ebidta margins

• Will show robust volume growth YOY for full year.

• Q1 is always the strongest quarter. Next quarter may see 5-7% sales drop.

CAPACITY ADDITIONS:

• Enhanced printing capacity by 60 Mn per annum by adding 1 printing machine.

• Placed orders for 2 new printing machines with installed capacity of 200 Mn pcs per annum. (9400 vs 7400 lac) Expected to commence by Feb 23

• Extrusion machine with installed capacity of 3,500 MTPA under installation at Umbergaon unit. (18,200 vs 14,700 in MT)

• Thermoforming machines in process of delivery/installation with installed capacity of 900 MTPA. (8,920 vs 8020 in MT) Expected to Commence by Sep 22

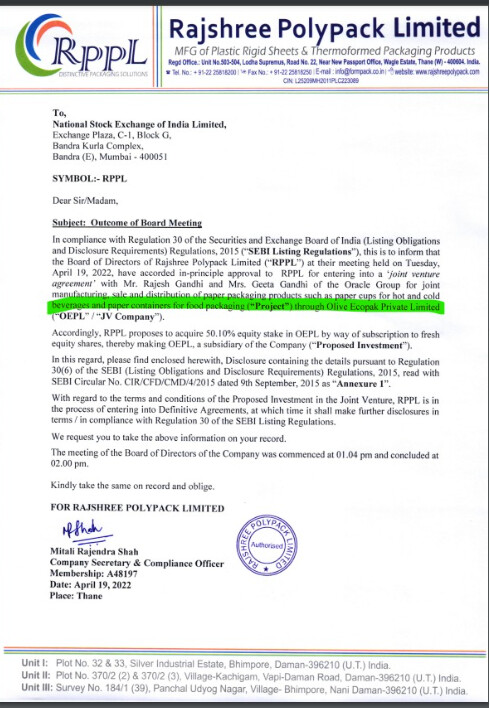

• Olive Ecopak Private Limited - Construction of Factory to commence in Sep 2022. Production likely to start from Oct/Nov 23

• INJECTION MOULDING: Entered into exclusive Toll Manufacturing Agreement for manufacture of food packaging containers using Injection Molding with capacity of 1,000 MTPA. Production to start from 1st week of September.

Why injection Moulding: Looking to increase wallet share in existing clients as they have requirements of IM Packaging Products

Intend to expand in this segment depending on future demand scenario

• Top Clients: Ferrero Rocher, HUL, AMUL, Tata Global beverages

• Thermoforming/Rigid Packaging Market: It is a niche segment with a few no. of players. Overall Market size around 1000cr and it is growing at a good pace as it is a new segment with new applications.

In certain products for customers, we are monopolistic supplier.

Current Plastic ban has no relation to company products.

All in all, the Rajshree Story is going on very well

INCREASING CAPACITIES WITH SUBSEQUENT SALES AND PROFIT GROWTH

STRONG RELATIONS WITH BIG FMCG PLAYERS

CONTINUOUS INTRODUCTION OF VALUE ADDED PRODUCTS (barrier packaging, tube laminates etc)

NEW VERTICALS - PAPER PACKAGING, INJECTION MOLDING

SECULAR NATURE OF LONG TERM END USER DEMAND

Q2FY23 Notes:

• Extrusion machines with 3,500 MTPA Capacity installation completed; production commenced. • Ramping up the production from newly installed machines. Total Capacity in Extrusion stands at 18200MT vs 14800MT (A growth of 23.6%)

• 12 new products added in Bakery segment. Total product basket stands at over 180 products

• Olive Ecopak Private Limited (Paper Packaging Project): Construction related activities commenced.

• Injection Moulding machines installation completed; production commenced• Thermoforming: 2 old machines to be replaced by 1 new machine in Jan 23

• 0.9cr of one-time expenses dented Ebitda margins.

• Guidance: 260cr Revenue – 15% (+/- 1%) Ebitda margins – 11000MT volume (5500MT in H1) – 16-17% Sustainable long term ebitda margins.

• Injection Moulding – Food delivery products are currently made.

• 10% of revenue from barrier packaging products with 43-45rs per kg ebitda margins (33rs per kg overall ebitda margins for h1)

• Tube laminates: Machines currently being upgraded to begin commercial production – will take 4-6 weeks

• Q2-Q3 are seasonally week quarters due to reduced offtake of certain foods and beverages. Q4-Q1 are the strongest