Screener may not show correct data pls check balance sheet. It is question of conviction and I have full conviction here. People can remain skeptic , it is their choice I am not and I was not even last year when they hardly showed any revenue as they have been honest with me. There is much to improve but I trust the fully

Never heard of their products or seen it. Looks and feels dicey to me !

Below is my understanding for Sonalis,

I believe majority of the sales are coming from selling of agricultural grains (like pulses, jowar, sunflower etc.,) and not from FMCG segment ( I.e. there product like granola bars etc.)

I belong to farming community and have observed trading and sales of farming goods from close.

Growing sales is not a major issues in these type of businesses.

Basically, if you have 1 cr working capital in bank then can easily do 40-50 cr sales as most of the things are on credit.

Also would always have receivables and payables due to business being on credit.

Employees also are not permanent as only unorganized labor would be needed .

Margins would be less and timing is needed to make profit i.e. hold for some time and sell when the time is right.

Now let’s talk about some of major risks .

In case of major accidents , defaults, issues in storages , etc. the whole business could be disrupted as it’s highly leverage business .

Very depended on people managing the whole things. In case of any mishap to key person major loss to business could happen.

Very easy to increase sales or/and manipulate books for sales. Hence mainly we should look at profits here and not sales.

Very easy to do frauds if some key employee want to and it would go unnoticed for long because many things would be unorganised in these cases.

Prone to many external factors like govt rules , climate, theft, fire, vehicle accidents , govt bribes etc.

Disclaimer: Not invested

I may be severely wrong if the major sales are not coming from sales of grains , pulses etc .

5 Likes

Yes and will stay invested for mid term surely , it is already 2 years and future looks brighter than ever before.. Investing is matter of conviction and I have full conviction here and numbers followed later.

1 Like

Hello sir @ Rajesh Singh - are you holding srivari spices yet?

hello, i’m visiting the mgt of mercury evtech. I have podcast shoot with their promotor Jayash Thakkar. Do let me know if you’d like me to ask any questions on your behalf. Thanks

Thanks, please update us about your takeaways after the interview!

1 Like

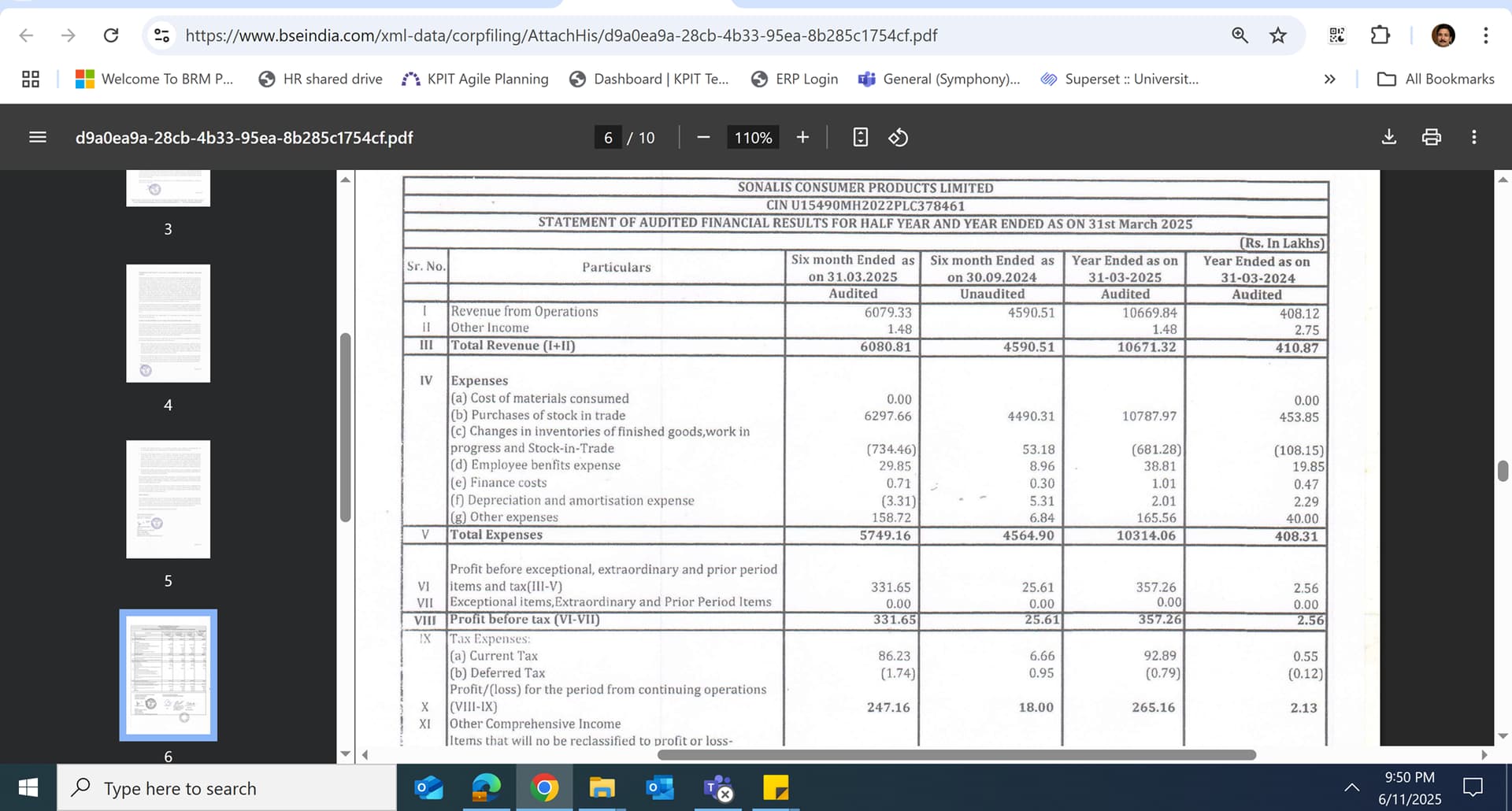

Half yearly update post results

It’s me, hi. I’m the problem, it’s me." Taylor Swift’s song “Anti-Hero” reflects the singer admitting to her own insecurities and flaws, acknowledging that her mindset and actions are the source of her troubles.

“The best stock picks cannot save you from yourself.” – Chris Mayer. This is true if you sell early based on price and lack the foresight to look ahead for value.

Do your own diligence (this is for reading and reflections)

Exits – SPML after multibagger returns as entry was at 22 and average price was 45 sold at 280 plus as earning guidance is for 30% growth. There are better opportunities available, like Sonalis, K2 and Veer health. I also exited Ganesh Green as Insolation is one of the best choices given vertical integration ahead. Solar at some time will follow chinese market with oversupply however given 500 GW goal by 2030 much steam is left. Ganesh Green, Alplex solar and a few others will do well too.

Trimmed Cellecor and it may come back to all time high by next year too. I also trimmed AVP infracon as dilution of EPS is a risk which I have started putting focus more. It can do well too ahead.

Entry and increased position – K2 infra is one the biggest positions now and am confident after management interaction that it will do well. Veer health reentered as it may pull of 10x increase in earning given India focus. Tracking position is in Asston Pharmaceuticals and will build more once have conviction in management.

There are 4 in portfolio on track to 10 to 20x EPS from buy period in 4 years Bondada, Insolation, Sonalis consumer, Kore digital and hopefully a few more can be 10x in EPS also in a few years. Given hammering in price, many stocks’ PE is down much despite great performance and equally great future so have removed PE column. With liquidity, favourable enviroment, a few can reach even 100 PE in a few years but wont anytime look at price or PE as it is beyond control. Since the last year, Max has moved permanent hold as it is only trend which I don’t see changing anytime in future. With digital offerings and asset light model, it can create enormous value in decades ahead.

| Name | EPS CAGR since entry | Entry | Avg price | EPS buy year | EPS FY 25 | EPS H1 25 vs H1 24 | EPS FY 26 | EPS FY 27 |

|---|---|---|---|---|---|---|---|---|

| Sonalis Consumer | 150% plus | Aug 23 | 57 | 1 | 5 | 1280% | 8 | 15 |

| Bondada | 100% plus | Aug 23 | 59 | 3 | 10.1 | 139% | 22 | 36 |

| Cosmic CRF | 65% plus | Sep 23 | 384 | 19 | 31 | 25% | 55 | 100 |

| Insolation energy | 100% plus | July 23 | 31 | 1 | 5.7 | 16% | 10 | 21 |

| Kore digital | 100% plus | July 23 | 202 | 9 | 26.5 | 9.2% | 50 | 110 |

| K2 Infra | 20% plus | June 24 | 83 | 9 | 9 | 67% | ||

| Srivari Spices | 30% plus | Mar 24 | 220 | 8 | 11 | 45% | ||

| Veer Health | Turnaround | Oct 25 | 18 | 0.2 | 1.0 | 2.5 | ||

| Kiri Industries | Turnaround | Nov 24 | 568 | |||||

| Max India | Feb 23 | 175 | FY 28 PAT +ve |

A few things to learn from history from three narratives of legends which again remind that what we learn from history that we don’t learn from history. Crashes happen and may last for years before one can see the bottom and if you are leveraged or don’t have enough liquidity to wait and survive then it can be catastrophic.

"There is no better teacher than history in determining the future.There are answers worth billions of dollars in a $30 history book: - Charlie Munger

Newton - One of the finest brains of all time, Newton lost most of his wealth in South Sea Bubble crash and said -"I can calculate the motions of the heavenly bodies, but not the madness of the people

Benjamin Graham and bull market brains

In 1930, thinking the worst was over, Graham went all in and then some. He used margin to leverage what he thought would be terrific returns. But the worst was not over, and when the Dow collapsed, Graham had his worst year ever, losing 50%. “He personally was wiped out in the crash. Having ducked the 1929 cataclysm, he was enticed back into the market before the final bottom. By 1932, the $2.5 million had dwindled to just $375k. In his memoir Graham wrote about how his early successes impacted his mentality before the calamity:

At thirty-one I was convinced that I knew it all–or at least I knew all I needed to know about making money in stocks and bonds–that I had Wall Street by the tail, that my future was as unlimited as my ambitions, that I was destined to enjoy great wealth and all the material pleasures that wealth could buy. I thought of owning a large yacht, a villa at Newport, racehorses. I was too young to realize that I had caught a bad case of hubris.”

Buffer third partner Rick loses his fortune in 70s crash

Rick was just as smart as us, but he was in a hurry. And so actually what happened – some of this is public – was that in the '73, '74 downturn, Rick was levered with margin loans. And the stock market went down almost 70% in those two years, and so he got margin calls out the yin-yang, and he sold his Berkshire stock to Warren. Warren actually said, I bought Rick’s Berkshire stock at under $40 a piece, and so Rick was forced to sell shares at … $40 apiece because he was levered. And then Warren went a step further. He said that if you’re even a slightly above-average investor who spends less than they earn, over a lifetime, you cannot help but get rich if you are patient.

Summarizing again key learnings

- Focus on Business, Not Stock Price: Invest based on the inherent strength and future earnings potential of a business, not short-term price movements. “Watch the business, not the stock price.” – Peter Lynch

- Patience is Key: Successful investing requires a long-term horizon (5 years to decades) and the temperament to withstand 50%+ drawdowns with conviction. Agility is vital also now to move capital away where value destruction will be huge too.

- Seek Scalable Opportunities: Identify small- to nano-cap companies with capital-efficient, scalable business models and significant growth runways.

- Temperament Over Skill: Basic arithmetic and common sense can outperform Wall Street professionals, as shared by legendary Peter Lynch when he said that class seven students beat wall street experts year after year with framework. Paying the right price covers a multitude of mistakes so buying cheap is vital too. “For investing, there is no substitute for paying the right price.” – Arnold Van Den Berg.

- AI and Robotics as Game-Changers: Align investments with transformative technologies like AI, which Demis Hassabis predicts will have a 10x greater impact than the Industrial Revolution in a shorter time. Avoid sectors facing value destruction – very few in IT services and BPO will survive this onslaught.

- Portfolio Concentration: A few winners can drive exceptional returns. Like life where a few relations, a few friends can make life great, investing rewards those who seek “pearls” (strong businesses) rather than chasing noise.

- Learn from Stalwarts: Draw inspiration from investors like Buffett, Munger, Lynch, Jhunjhunwala, Madhusudan kela and others. Their podcasts and writings offer timeless wisdom on allocation, patience, and temperament. I stay informed through newsletters (e.g., Peter Diamandis blog on megatrend, Brian Feroldi, Alpha Ideas, McKinsey, BCG and a dozen sources on weekly basis) and three newspapers daily.

- Reinvent and Start Anytime: It’s never too late to begin investing with discipline and learning. “Too late is an internal fantasy, not an external reality.” As Guru of all gurus Warren Buffet said in his last letter a few days back that we don’t understand the role luck plays in our success, being born at the right time with the right ecosystem plays much bigger role. In fact being born itself is a miracle if we come to think of it given trillions of genes over life time and we are that lucky one which won this lottery of life. Let us think and act with wisdom.

Good luck everyone!

18 Likes

Hi Rajesh Sir,

Requesting a quick summary of your interaction with K2 Management/Promoter — how it went, main takeaways any key insights or strategy points.

K2 is road making company. Untrustworthy promoters. Dont go for cheap valuation trap.

1 Like

Rajesh ji, how is your thesis on Sonalis now. They are talking so big on everything, want to acquire solar company, acquire IT company, warehousing, Consumer goods and what not. Acquired a milk unit and it will take 6 months to start. May be too many boats they wants to put leg before starting in one.

1 Like

I want to discuss about a potential value trap company which had been discussed in the past conversations, i had dig down some facts and the outcomes of the same, the name of the company is AVP INFRACON.

i would like to start with the fundamentals of the business , its promotors, its inception. okay then let’s start.

AVP INFRACON is a Tamil Nadu based EPC contractor working primarily with NHAI, PWD and other government infrastructure bodies. their areas of work mainly includes roads, highways , expressways, Bridges, flyovers, commercial construction and a Newly addition vertical Solar EPC.

Coming to the promotor’s background, D Prasanna (CMD & CEO), Vasanth D(Whole Time Director). the key thing to note here is Neither the CMD (Computer Science engineer) nor the WTD (salesman background) has formal civil engineering credentials. This is not disqualifying many successful SME infrastructure promoters are generalists who master execution through experience. However, at Rs. 500 to 800 Cr revenue scale with complex NHAI projects, technical depth in leadership becomes increasingly important. The 15 year track record of growing from zero to Rs. 272 Cr is the strongest counter argument. Combined promoter holding of 62.4% post IPO signals strong alignment with shareholders.

Let’s go on the Revenue model of the company:

AVP Infracon operates through two primary execution methods-

(1) Bill of Quantities (BOQ) i.e fixed rate per unit of work contracted, providing revenue predictability and

(2) Engineering, Procurement and Construction (EPC) full project delivery including design, material sourcing, and construction. EPC contracts command higher margins but carry execution risk. The company has been progressively shifting toward higher margin EPC as it builds equipment ownership and technical capabilities.

“it’s just a normal EPC company, what is new in the company?”

Let’s check Moat i.e competitive Business Advantage of the company,

AVP’s competitive advantage is narrow but real-

(1) NHAI prequalification for large contracts requires track record that acts as an entry barrier.

(2) Owned equipment fleet of 124 units reduces cost vs assetlight competitors.

(3) Vertical integration via RMC plants and crusher unit protects margins. The moat is Execution based, not IP or brand based making it replicable by larger well funded competitors if they choose to enter Tamil Nadu at this scale.

(4) However, Though AVP is a small company but huge in Tamil Nadu, marking a geographic concentration. ( someone may argue to be a disadvantage as long as it will be replaced by another one in Tamil Nadu, but it is not happening now)

When i go to past concalls and annual reports, they had repeatedly mention to acheive certain objectives and expectation , let’s see what it is and whether they had actually delivered or not?

- They repeatedly told about expanding in another region apart from Tamil Nadu i.e to achieve 25%-30% from other than Tamil Nadu but sill they have NOT achieved.

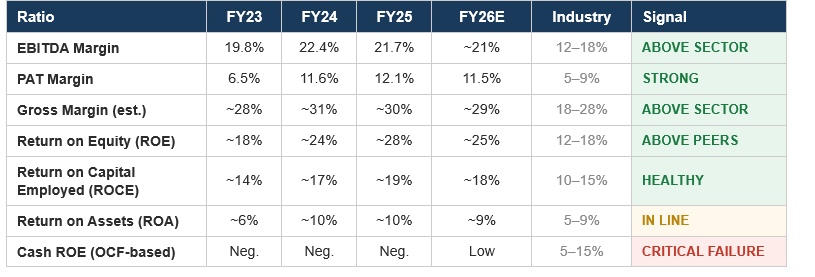

Stock is hammered by the market majorly due to NEGATIVE Operating Cash Flow, while Net debt has been pushing on upwards side ( please see the screen shot to get the clear picture)

As you can see, Operating profit is increasing yearly with Healthy Margins but the same is not converted into cash , the worst part is OCF is turning negative , meaning thereby, either there is Aggressive Revenue recognition, Receivables are increasing or it can be investment in subsidiaries in the form of loans and advances ( loans and advances are given to subsidiaries, in the books it seems good but you may never know.)

Someone may argue on profitability ratio, but what is the use i will present some ratio, but when you see the above cashflow number it fails,

The Ratios seems Fantastic but when the times are uncertain Cash is the only thing a company need.

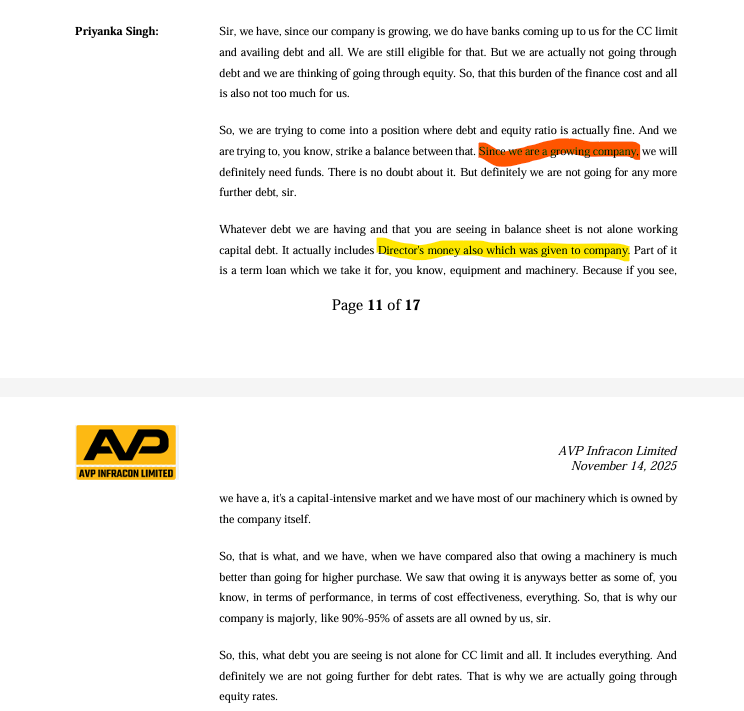

I want to present a concall highlight when asked about Piling up of Debt the management responded with -

Management told since we are a growing company we need funds and to justify they also added it includes director’s money also. As per my understanding , even though it is a growing company if you cannot fund through internal accruals at a certain point then the company is in a vicious circle ( Readers may note that i am not being too harsh by criticizing, but they clearly destroy values of shareholders by piling up of debt.)

Operating cycle is still elevated around 150-170 days , meaning you complete the work today and you will receive the money in 6 months and for that you won’t receive interest but for the Additional funding you have to rely on debt and pay interest ( in short - Neither here nor there.)

The best part is the orders are coming at huge scale, if the company FIX this problem tables will turn from Massive Trap to Highly Undervalued.

Happy Reading.

Disclaimer - I am Not a financial Advisor, this is purely for Educational purpose.

4 Likes

Do your own due diligence Opinion comes easily, wisdom is rare in investing. I won’t do anything for any stock in portfolio and if market conditions remain like this and PE doesn’t increase high then next year also wont do anything. Next blog also will come next year.

Many stocks have delivered excellent results (Sonalis consumer, Bondada, Insolation, veer health) and remaining like Kore digital, K2 Infragen, cosmic, Srivari, Kiri future is promising. Portfolio went up by 6 times from Feb 23 to Aug 24 then down by 50% to Jan 26 then another 30% drop so nearly two thirds drop at the peak of pessimism. I have to remain focused on future earning potential and inherent strength of business. What is happening now in stock market is recurring pattern every decade almost so those who are panicking need to read history of equities.

Investing is an act of wisdom if one builds a mental model and remains agile as it provides the best things in the world - reading, interacting with best minds, reflection , autonomy, mastery and creating meaningful impact and is simple though not easy.

Compounding is P (1+r) n so unless one is lucky inheritor, higher r (return) and higher duration (n) is needed. r is a function of current EPS expected EPS and PE. PE can swing wildly as we have seen in SMEs with 100 plus to now less than 10 in many even those who have delivered 100% CAGR with trustworthy management.

I removed all pure knowledge based stocks in by Q3 FY 24 and all export related also in view of US presidential election and still portfolio went down by two third at bottom. This is normal nature of market ( 92 scam, dot com bust of 2000, 2008 financial crisis, 2018 small cap meltdown, 2020 covid, 2024 Trump tantrum and so on) , if one wants high return then one has to be prepared for volatility and mindset to look at portfolio real value at 50%. The reasons may vary but stocks keep tanking by 50% or more at regular interval of 5 years and yet equities have created huge wealth

Anyone can become investor with common sense , class 4 level arithmetic and mental model to look at earning and potential earning with reasonable valuation and trustworthy promoter

A few links which I have enjoyed

https://youtu.be/e8OKBc7ZOkE?si=2bQuF6YCXM2GuKUj

https://behaviouralinvestment.com/2026/04/14/what-are-your-investment-beliefs-2/

https://youtu.be/Ws5It8duxLU?si=ZR1ovMT4Ur2IY96Y

https://91capital.substack.com/p/fundamentals-dont-re-rate-small-micro

The wrong question is: “Why is this 20% growth company trading at 10x PE?”

The right question is: “What has to change for liquidity to arrive here and when is that likely to happen?”

“MASTERCLASS on Value Investing with Prof. Sanjay Bakshi” [00:00] (http://www.youtube.com/watch?v=K7Y5iwBe3E0).

https://www.kingswell.io/p/five-things-i-learned-from-chris

Even the best stock picks or savviest money managers cannot save you from yourself. If you chase every rally or panic at every bump in the road, there’s not a whole lot that can be done to rescue your returns.

I think the reason why we got into such idiocy in investment management is best illustrated by a story that I tell about the guy who sold fishing tackle. I asked him, ‘My God, they’re purple and green. Do fish really take these lures?’ And he said, ‘Mister, I don’t sell to fish.’ Munger - so much about professional fund managers and influencers..

No one saves us but ourselves. No one can and no one may. We ourselves must walk the path".

Mindset and temperament

-

Prioritize time wisely: Allocate your limited time to activities that align with your natural inclination and strength. We need a few winners and they are always around, one needs conviction and differentiated view from crowd to buy and hold as long as potential is there.

-

Focus on business, not price: “Watch the business not the stock price.” Constantly checking price or shuffling the portfolio without a material change in the business’s inherent strength leads to mediocre returns.

-

Live beyond the portfolio: Structure your life so that a portfolio value fall of 50% or more for years won’t have any material impact on your life.

-

Investing is a search for pearls: “It is same ocean, what is that one is looking for salt, fish or pearls.” Investing success requires finding a few “pearls” in the form of quality stocks and holding them. I have continued to build positions on Sonalis consumer, K2 infra and KDL. Kiri industries and Veer Health will remain in SIP mode as they execute 3 year vision. Bondada and Insolation already created huge wealth from IPO despite being down from top.

-

Simplicity is key: “Anyone with class four level arithmetic and common sense can become investor,” Peter Lynch’

-

Seek scalability: Focus on businesses that are scalable, capital-efficient, and have a large, long runway ahead.

-

Avoid complex risks: Intentionally stay away from cyclicals, overvalued, hyped, and stressed assets, as navigating them requires a level of market timing that is too difficult to get right. When I was learning I was part of many groups and found rarely any wisdom, investing is solitary journey in many ways.

-

Patience is real edge: Enter a stock after thorough research, then sit tight unless something material happens to alter the original decision.

-

Ignore the Pontificators: Nobody knows what the market is going to do tomorrow, next week, next month," he added. “But they spend all their time talking about it, because it’s easy to talk about. But it has no value.” Buffet

In the Bible, it says that love covers a multitude of sins. Well, in the investing field, price covers a multitude of mistakes. For human beings, there is no substitute for love. For investing, there is no substitute for paying the right price - absolutely none."

– Arnold Van Den Berg, Outstanding Investor Digest, April 2004

It is not about money but the best I can make of myself when I listen to the thoughts of great investors podcasts, their thinking. If I look at my life when I have been happiest then it is in investing process and it is never ending joy.

I am reminded of Machiavelli’s letter to his friend “When evening has come, I return to my house and go into my study. I enter the ancient courts of ancient men, where, received by them lovingly, I feed on the food that alone is mine , I ask them the reason for their actions; and they in their humanity reply to me. And for the space I feel no boredom, I forget every pain, I do not fear poverty, death does not frighten me.”

It’s never too late. You can wake up and choose to see things differently. You can change. You can completely reinvent your life. “Too late” is an internal fantasy, not an external reality. I started at 45 and portfolio went up by 6 times in 14 months from Feb 23 to Aug 24 and now it is down and it is ok. This is still beginning for me despite huge risk of terminal value in most business in view of AI and robotics onsluaght.

Good luck everyone

5 Likes