I have observed that you have made an entry in Veer health care during May, May I ask for your thesis behind it? Is it because of its order acquisition from Apollo Pharmacy and other export orders from US?

The hypothesis was their presentation in Bharat connect however I have reviewed my portfolio to derisk and Veer is going out from portfolio. One risk I didnt factor was US FDA and challenges , it can do well in three years given ambition of management however I will exit it.

Build investment mindset - Watch the business not the stock price, enter after research then sit tight for years unless something really material happens to alter the decision. Where are we spending time, in this era of weekly and monthly screenshots if one is glued to screen for the price and not looking at business mediocre returns will follow.

If stock is going to be 100x with business growth say Insolation has 1-Billion-dollar goal in three years with 10% PAT, then valuation at 100 PE will be 10 billion USD and after that also it will grow at furious pace as Solar is decadal megatrend then it doesn’t matter where it is 20 % or even 50% down. Here is sample projection of Insolation without equity dilution , split or bonus , 500 plus bagger from my average buy price in 7 years and anyone who got IPO at 38 Rs it is already 100 bagger in just two years…

Year

23

24

25

26

27

28

29

30

Earning growth

510%

115%

100%

100%

100%

100%

80%

EPS

5

26

55

110

219

439

877

1579

PE

10

150

140

130

120

110

100

100

Share price

311

3825

7676

14255

26316

48246

87720

157896

I rarely come across people in my network who are not glued to price and doesn’t panic when price goes down as they rarely look at business future. Large allocation in the early phase when high conviction in management, value, patience to let the winners run. Never interrupt compounding like you never lose great relations- a few can be 1000x also if one hold for many decades with foresight to see megatrends and competent management - not in a quarter or year and ignore all the noise be it macro factors or fluctuations.

Stock

PAT CAGR for years

PE 5 years

Entry price

Avg now

Return by FY 26

FY 30 or longer

Insolation

100% plus

100+

140

311

40X

500x hold longer

Bondada

100% plus

100+

30

59

40X

Kore digital

100% plus

50+

220

485

40X

100X

Sonalis Consumer

100% plus

50+

60

60

40X

50X

Max India

20% plus

80+

80

147

5X

Permanent

Cosmic CRF

100% plus

50+

220

384

20X

100X

K2 Infra

80% plus

50+

156

156

5X

50X

Eco recycling

100% plus

100+

140

314

20X

100x

Tejas

50% plus

60+

70

253

10X

TBD

SPML Infra

Turnaround

50+

20

45

20X

TBD

Cellecor

100% plus

50+

25

29

10X

TBD

Vmarc

100% plus

30+

200

249

5X

Exit

AVP Infracon

80% plus

30+

150

160

5X

50X

Srivari Spices

100% plus

50+

220

220

5X

50X

Investing requires very little action so if one is itching for action then pick any sport and if your adrenaline is high then pick some something adventurous here more action will lead to average to below average result.

I have proven wrong in the last six months to market will keep humbling.

Exits- Veer health- US FDA risk I had ignored and generally I have stayed out of pharma for this reason. It can do well but not worth the risk

Tech know green- Management keeps talking big of 8 billion USD market and hardly any growth , neither orders so have lost faith in them. I also exited Kamat hotels which was a trading bet as management looks like floundering on walking the talk.

Entry Srivari spices 100% CAGR, AVP infracon projection of 10x earning in next 3 to 4 years

Wise Charlie Munger who died this year said before his death “I could have done a lot better if I had been a little smarter, a little quicker … I might have had multiple trillions instead of multiple billions." “How do you get a great spouse; you deserve a great spouse.” What it means that for anything in life if you want great say great returns in investing then your perspective and actions have to deserving else mere aspiring will take you nowhere.

Ignore noise - Almost all have opinions and very less have depth and temperament needed for high returns. Many superstars and HNIs will learn basics of valuation that share price is function of earning and corporate governance. Blue chips and many large companies have posted disastrous results year after year, and many will vanish too. Many of them come and convey pompously about SMEs that something is wrong while many stocks in their portfolio like Tata Elxsi, LTTS, Asian Paints have given negative return in the last three years. Again, reminds of Buddha - Be your own light! One has to keep laser sharp focus on business growth and its potential, rest all is noise. Social media , and media in general is noise so be careful whom you listen to as very few have depth. We are lucky to be part of this time when it is century of India 4 to 40 US trillion then beyond in fact there is talk by K Subramanyam that it can be 55 trillion USD also by 2047 https://youtu.be/I_zJKxft4rw?si=y-5XSiIcIB2NWNgT

I listen to many YouTube videos and talks almost hundreds in a year while traveling, commuting, or walking. Invariably I go through management interview, guidance of all companies. Without guidance have stopped investing almost now. Let them be wrong but be bold and transparent enough to say

I follow many on twitter and most of them keep posting and at times I reply too but I don’t feel the need to be active there. Out of all of them I admire @chiragdashj most. I will continue zero base budgeting in investing and if any stock at that time doesn’t look great enough then will exit however this will happen yearly. It is not about money but quality of life as one of the wisest Charlie used to share - I wanted independence I overshot and got rich.

Risk management is very difficult as Howard Marks says “what we don’t know say covid, 9 /11 great recession of 2007 and so on…

He shared once “I tell my father’s story of the gambler who one day hears about a race with only one horse in it, so he bet the rent money. Halfway around the track the horse jumped over the fence and ran away”

They had investor call on this Sunday wherevtgey shared update. I ude screnner as tool to read about companies yiu can see its latest annual report, half yearly result but itd about future which is going to be very different

Thanks Sir for your great guidance.

Even I have been skeptical about K2 Infra looking at the H1 results but Pankaj’s words give a positive vibe. But your words gave me clear peace of mind and perspective to look at long term.

Posting this here since I couldnt find a thread for cellecor

Their Financial Result has been postponed for ‘want of quorum’ plus the stock had a steep fall today

Anyone here tracking this story?

Primafacie any such decision is not sign of good corporate governance, however it is an emerging key player in a fast growing segment so will stay invested as their execution has been excellent so far, invested since lower levels and will stay invested as long as hyper growth is there for next 3-4 years

Late big bull Rakesh J said so wisely Markets can be learnt not taught (his interview with Ramesh Damani on 60th birthday – one of the best of all time)

Any asset we buy for investment be it Gold, land, house, Bank deposits we don’t check price frequently but in equities this is very common which is not investing mindset. Almost all renowned investors say that minimum time horizon for investing is 3 years and more importantly alpha comes in decades and only a few stocks are needed.

Portfolio update -

Wonderful result by Sonalis (13 x earning growth H2 vs H1 and top line growth by more than 26X) but more importantly bold goals ahead of 1000 crore topline and 63 crore PAT in 3 years which is 24x from here.

Bondada (150% plus PAT growth, 10000 crore topline target by 2030 with similar margin and can achieve this earlier too

Insolation and Cosmic both H2 was disappointing but future looks very promising for next 4 years

AVP infracon 80% earnings growth and guidance of 1000 crore topline by FY 28

Ganesh Green, Kiri Industries (topline guidance double next year and 40x in 4 to 5 years) Srivari, K2 Infragen both failed to deliver which shows how difficult it is to walk the talk by management but will give them some time as commentary shows still hope.

Kore digital - excellent result 136% increase in EPS. Price has been hammered; the company went to declare quarterly results when it was not even needed then suddenly delayed the result this quarter but will give the company time as highly undervalued and potential is there.

Exits- Eco recycling exit as promoter’s conduct did not inspire any confidence. In good times, he was all gung-ho , one poor quarter and he forgets investor calls, no response to mails too but more importantly it looks that business has no inherent differentiation still it has been multibagger for me. In life as well as in investing people can be the biggest source of joy and headache both and have to reduce tolerance for anyone not with the right mindset or behaviour as more than the proceeds one wants to enjoy the process. Exited Tejas also as it has sharp fluctuations in topline and bottom-line with no guidance means mgt can’t be held accountable. Both of these have multibagger. V marc was trading bet and exited too.

Stocks have to keep performing as per guidance else will keep removing them.

Name

PAT CAGR since entry for the next 5 years

PE 5 years

Avg price

Price by May 26

Return by May 27

FY 30 or longer

Insolation energy

100% plus

70+

31

700

40X

Can be 10x more

Bondada

100% plus

70+

59

1000

40X

Kore digital

100% plus

50+

205

800

10X

Review

Sonalis Consumer

200% plus

40+

57

200

10X

Review

Max India

20% plus

60+

147

250

3X

Permanent

Cosmic CRF

100% plus

50+

384

2000

15X

Can be 10x more

K2 Infra

0%

30+

156

Review 26

Review

SPML Infra

Turnaround

50+

45

250

15X

Review

Cellecor

80% plus

50+

25

100

10X

Review

Srivari Spices

0%

30+

220

Review 26

Ganesh Green

80% plus

70+

462

700

5X

Can be 10x more

AVP infra

80% plus

40+

164

300

5X

Kiri Industries

Turnaround

30+

668

800

10x potential, review 27

I can hold stocks without return for mid-term too if I have confidence in mgt for huge value creation ahead like Sonalis. When Bondada and Insolation tanked by more than 50% in a few months last year it didn’t unnerve me at all as business remains robust and price will come but damaged business very difficult to come back.

Classic investing has been about compounding at 20 percent over decades meaning doubling every three year 100x in 20 years then every three-year doubling so 1000 times by 30 years so every decade one zero gets added. Now if we take 100% CAGR the same can happen in a decade too. Again we don’t have to get 1000 baggers three 10 baggers in sequence also can make (10x 10x 10x)

One need to find never ending trend and competent mgt hence the permanent holding is Max India

Many of the companies I am invested in are raising capital at a furious pace diluting EPS. Ideally growth has to come from internal accruals and the company shouldn’t be raising capital much.

One of the greatest investments of all time - Sees candies and it is in that rare group with pricing power and differentiation.

Another mega trend, most knowledge in five year can be done by AI and most things that are moved by Robots then the entire economy itself , business models will be different. It may have very few winners however have to remain focused not to get caught in vortex of AI and robotics in years ahead. US and Europe both are going to decline hence focus is on India and any company which is focused much outside is a no too.

“Market can remain irrational longer than you can remain insolvent” Keynes said, so I am going to take leverage which I can afford. But at the same time won’t hesitate for a big swing when the opportunity comes as Charlie Munger said before his death that his regret was not taking a bit of leverage or taking risk else he could have done much better.

If you want better returns then take a hard look at the person in the mirror. “You will sell winners too soon. You will hold losers too long. You will buy stocks you shouldn’t. Just don’t blame others. When you blame others, it proves you didn’t do the work you were supposed to do. Fully own your investment mistakes so you learn, grow, and move forward” - Ian cassel

Charlie Munger till his death shared his wisdom - the power of concentration and regretted also not taking bolder moves.

"The main trick that Berkshire shows is the power of what I call the Wooden effect. Wooden was the most famous basketball coach of the whole era. He concentrated about 90% of the playing time in seven players. That turned out to be a great system for winning at basketball; you learn by playing in a way you can never learn just by shooting practice baskets

Regrets - I’m not all that pleased. I basically screwed up. I could have done a lot better if I had been a little smarter, a little quicker. I might have had multiple trillions instead of multiple billions. I do think about what I missed by being just not quite smart enough or hard working enough. Berkshire could easily be worth twice what it is now. And the extra risk we would’ve taken would’ve been practically nothing. All we had to do is just a little more leverage that was easily available".

I keep reading and listening to many wise investors - Manish Chokhani, Madhusudan Kela, Gunavanth Vaid, Ian Cassel, Peter lynch, Rakesh J, Charlie Munger, Buffet and many more as our perspectives become better by their wisdom. Manish chokhani’s interview is very insightful

Markets can go down for various reasons and remain down for years too so horizon has to be mid term at least as all renowned investors convey however this is India’s time and am bullish for mid term.

Most have a mindset fixated on price and are unnerved by noise around when only two things matter - earnings and corporate governance. Patience is very difficult and it is rare to see a mindset of long term or focused on business. Price cracks and conviction evaporates for the most and so does the potential to have better returns also.

Be wary of influencers, media , even institutions (most of them come when a significant runway has already happened). With some basics anyone can avoid obvious mistakes. Imagine investing in Paytm (Berkshire erred too pre-IPO - where there was moat, cashflow or even differentiation), Tata Technologies, Ola electric and many others IPOs came at frothy valuation and many institutional investors took entry and they may never ever close to their IPO price. Almost the entire IT sector is in doldrums because of tremendous headwinds- geopolitical uncertainties , AI , automation , long term structural decline of Europe and US - how many will survive this churn is anyone’s guess as the new era will require deep expertise which many claim and a few have!

We need good luck too as great returns need great liquidity and a stable ecosystem. India is in a sweet spot despite many challenges. Good luck everyone.

PS- I would like to dedicate this edition of yearly blog to Late Surbhi Jain, Joint Secretary, Deptt of Economic Affairs, a dear colleague who was part of our foundation course in LBSNAA Mussoorie and later in NIFM Faridabad. She passed away a few days back and her family donated all vital organs also. My condolences are to all in her family.

Very informative post as always. There is a lot to learn from your detail post and the reference article, interview video link etc. Thanks for sharing.

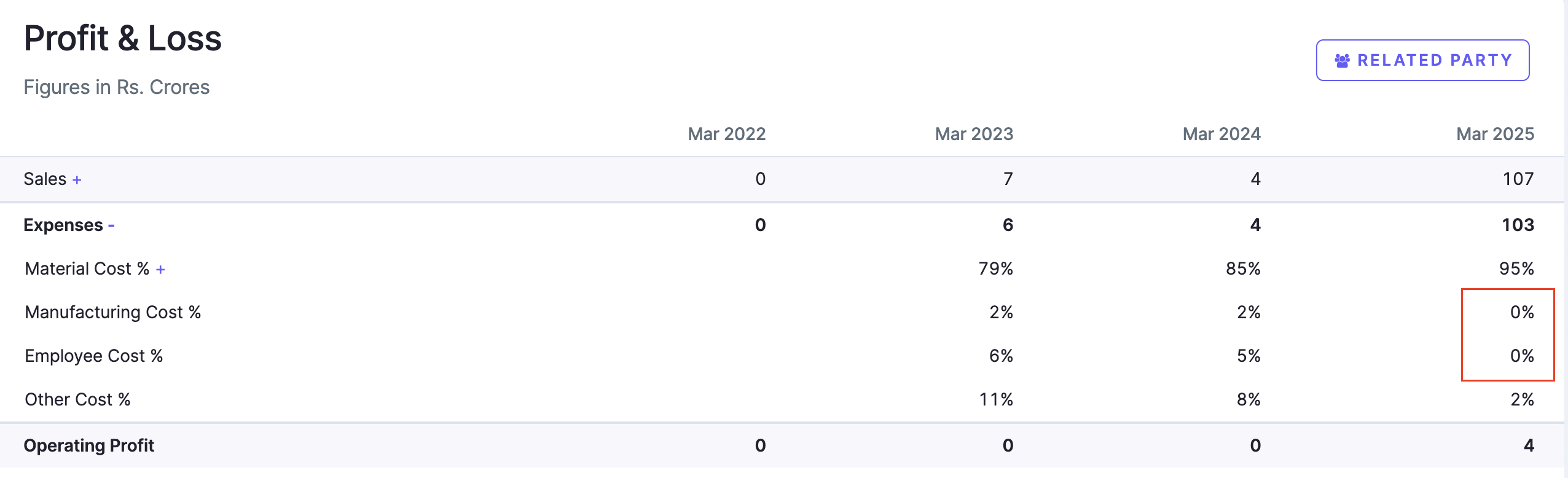

Regarding Sonalis, I am curious how their topline grew from ₹4 cr to ₹107 cr in just 1 year. What are the key factors or strategies that drive 25x growth? Interestingly, the PAT grew by only 30%, and there doesn’t seem to be much in the cashflow statement either. Would you like to share some insights?

Would you happen to have the recording by any chance? Otherwise, if you can please share some of the key points from the call that would be very helpful. Thanks.

It’s not a EMS play, it is a semi-conductor play. Their parent company in the US already have the technology for compound semi-conductors(SiC), RIR will be leveraging that to manufacture the same here in India. They had a 3 pronged plan, if I remember right the actual semi-conductor part comes at the end. Management came across as very honest, watching this older AGM should give a good perspective:

Thanks so much for sharing the video for Sonalis Consumer Products Ltd. It really changed whatever little perception I had about the company.

The commentary is vague. Audio is not present for most part.

They plan on earning 6Cr revenue per month from a warehouse built over 13 acres. Rental income of that magnitude is possible, but they haven’t given more information about the warehouse, total cost of construction etc. There is only a picture of a labour shed.

Their USP is to stock the agri-produce and sell it off-season to make better margins. Not an ingenious strategy.

Their employee expense is 1 lakh outside of the board but with commissions, consultancy fees they are managing a team of veterans and they also have a R&D team.

The main person behind the company is absent from the call.

I am sorry but a lot of it doesn’t sound convincing. Is this what they call pump and dump?