Why shares fell upto 10% in two days ? Any news regarding this sel off.

I assume it is happening because of latest supreme court’s order to Govt. to standardize hospital charges.

Link- SC directs Centre to standardise healthcare procedure rate: How will it impact hospitals?

Rainbow enjoys over 35% OPM. That’s a big number for a hospital.

If Govt. intervenes here, the OPM is likely to go lower.

If that happens then why should market pay 50+ PE for Rainbow.

Hence the selling.

My thoughts only.

Disc: not invested

6 Likes

View on Corporate Governance

It’s encouraging to note that 4 out of 7 directors are independent, which is a positive sign for corporate governance. The BOD’s diversification and experience contribute to a well-rounded perspective. Members of the board bring diverse expertise to the table which helps to take informed decisions. Direct connection in the board, between Dr. Adarsh Kancharla (Non-executive director) is son of Dr. Ramesh Kancharla (Chairman and Managing Director). While Dr. Adarsh lacks prior experience in business & management, his inclusion in the experienced BOD raises questions about the criteria for selection. We assume that Dr. Anil Dhawan, an independent director, having an indirect association with functional directors. This could impact their independence. Overall, the BOD appears promising, but the indirect association with functional directors warrants second thought. The Board of Directors are considered experienced but on the other hand the management is new to the company due to the recent change in CFO & Group COO, with Vikas Maheshwari taking over from R. Gowrishankar, & Sanjeev Sukumaran taking over from Dr. Rohit Manipal Bhojaraj is also noteworthy. Other than this the management have all of its policies right on point. Please put some light on it if somebody has better understanding into the governance.

Discl :- Above points are my observation I might be wrong. Not an investor, looking for opportunities.

3 Likes

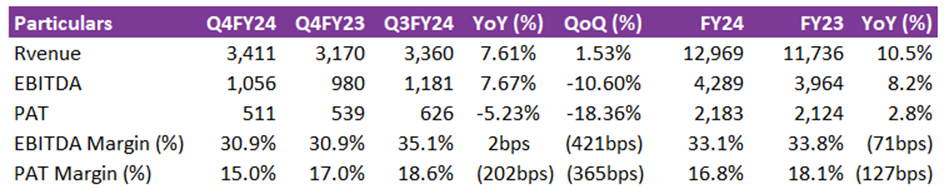

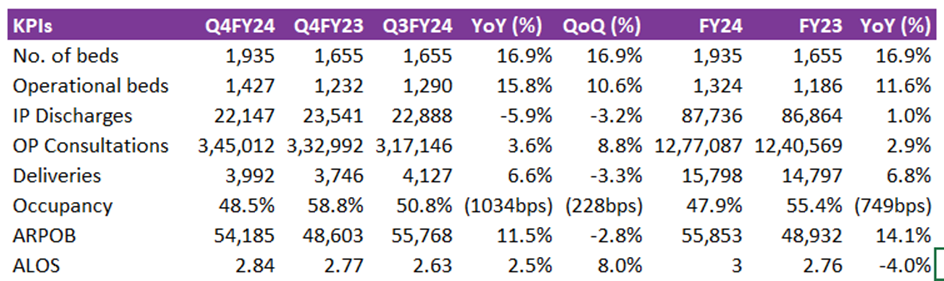

Another disappointing quarter by Rainbow. FY24 has been the year of headwinds, Lower seasonal illness admissions, seasonal imbalance, delayed mansoon, cyclone affect in Chennai which effected the business. Managment has given guidance of ~15-18% for topline growth. management is working on to improve its brand recall in Chennai and Bangalore in coming future these clusters will be growing near to same as the Hyderabad cluster. Balance sheet to remain robust, capex will be funded by internal accruals. Announced a capex of ~50cr.

The main disappointment is around the growth in the matured hospitals. They had good amount of expansion and that was mainly in the new hospitals which is reflected in the bed count and occupancy and this is understandable as the cost is front ended in hospitals. But despite a good growth in ARPOB and some expanded capacity, the occupancy for matured hospitals dropped for various reasons.

EBITDA growth compared to revenue growth haven’t fallen off significantly and it is PAT growth that has dropped so no concern on the core business. This is mainly coming from additional depreciation due to front ended costs. A 15-18% topline growth is lower than the recent past (Last 3 years - 26%) so this signals a period of consolidation in the immediate coming quarters…?

Disc: Invested and biased. 3% of portfolio.

1 Like

Agreed, whats your future outlook on this? Considering other players in this sector are doing decent

1 Like

They have a lot of new hospitals and beds brought online in the last 2-3 quarters. The front ended costs are (potentially) hitting balance sheet and as a result bottomline looks slow growing. More greenfield expansion would result in higher front ended costs suppressing the numbers.

I would track the ARPOB and occupancy metrics for matured vs new and check the trend. I am invested and continue to stay so as I don’t see a threat to the core business of childcare as there is not much direct competition. In any case, the concall should give better subjective insights on management’s view.

Disc: Invested

3 Likes

Excerpts from Q1FY25 concall:

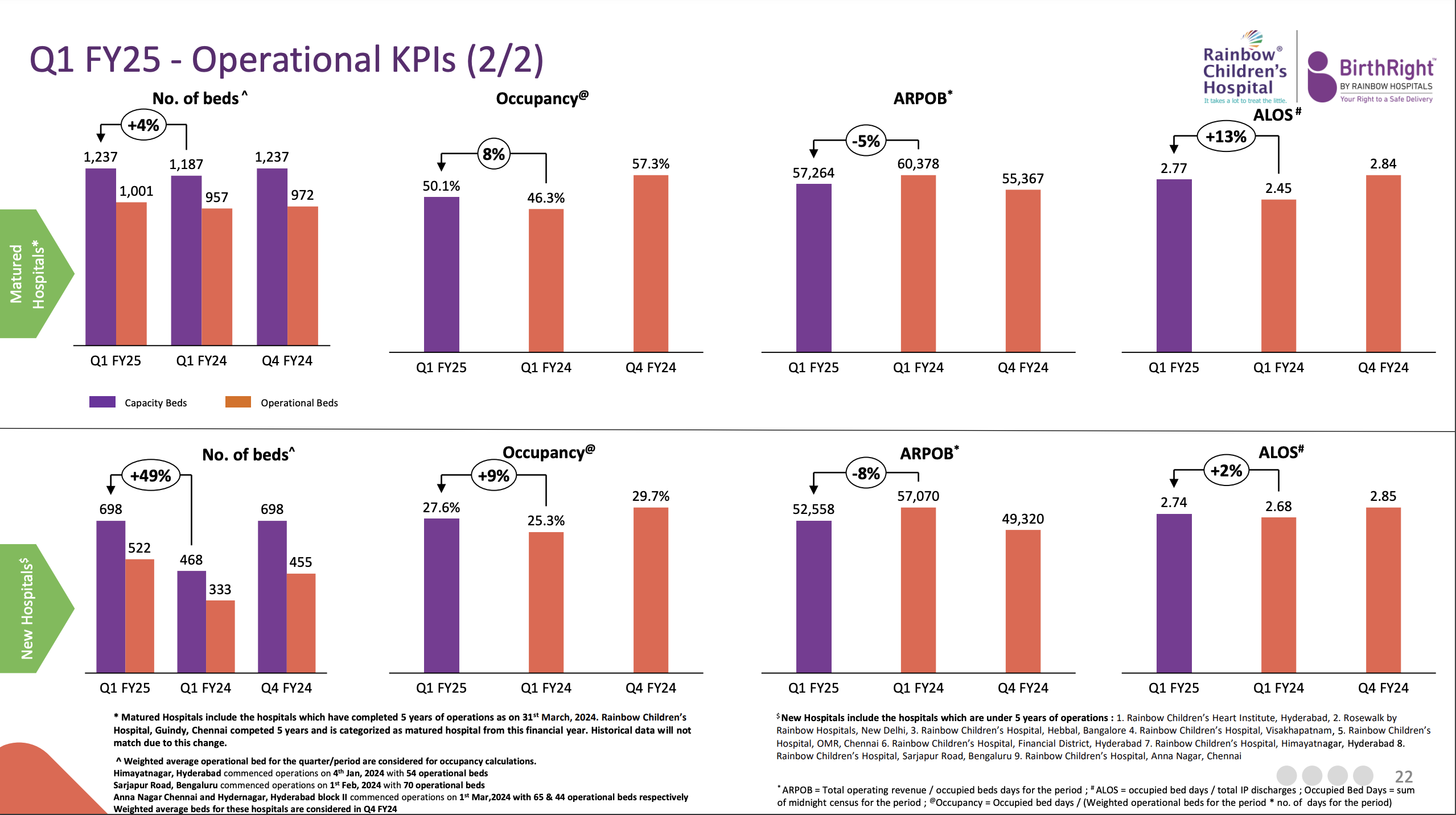

New hospitals take between 1 year (HYD) to 2 years (BLR, MAA). And occupancy in the newer hospitals is ~27%, way below the breakeven of 35%. This is definitely a drag on the margins which should improve in coming quarters.

And more beds coming in HYD and BLR in FY25 so expect subdued margins for FY25.

Disc: Invested

3 Likes

Rainbow Children’s Hospital

Q2 FY 25 results and concall highlights -

Company’s portfolio of hospitals -

Hyderabad - 8 hospitals, 1 clinic

Bengaluru - 4 hospitals, 1 clinic

Chennai - 3 hospitals

Vijaywada - 1 hospital, 1 clinic

Vishakhapatnam - 1 hospital, 1 clinic

Delhi - 2 hospitals

Total - 19 Hospitals, 4 clinics

Doctors team @ 835 full time doctors

Bed Capacity @ 1935 beds

Q2 financial outcomes -

Revenues - 415 vs 332 cr, up 25 pc

EBIDTA - 147 vs 117 cr, up 25 pc ( margins stable @ 35.2 pc )

PAT - 79 vs 63 cr, up 25 pc

Mature Hospitals ( > 5 yrs of operations ) -

No of beds @ 1237 beds, up 4 pc YoY

Occupancy @ 68.6 vs 57.9 pc, up 18 pc YoY ( a massive jump )

ARPOB @ 51.4k vs 55.2 k, down 7 pc YoY

Newer Hospitals ( < 5 yrs of operations ) -

No of Beds @ 698 vs 468 beds , up 49 pc YoY

Occupancy @ 43.2 vs 32.9 pc, up 31 pc ( a massive jump )

ARPOB @ 44.7 vs 50.9 k, down 12 pc

Payor Mix - Cash : Insurance @ 47:53

New capacity addition pipeline -

Rajahmundry ( AP ) - 100 beds - current FY

Bengaluru ( 2 locations ) - 60 +90 beds - next FY

Coimbatore - 130 beds - next FY

Gurugram - 100 beds - FY 27

Gurugram - 300 beds - FY 28

Company’s IVF segment has attained significant growth momentum. Company expects the same to continue going forward

Company launched ‘Butterfly Essentials’ brand of products for Mothers and New Borns early in CY 24. Products like - Wet Wipes, Soft toys, Body oils, Lotions, Aloe Vera gels etc. Initially, company shall only sell these products via stores inside their existing hospitals

Company’s Rajahmundry hospital is slated to open in Mar 25

The two new hospitals in Bengaluru should go live in Q2 and Q3 FY 26

International patients currently constitute 2 pc of company’s total business

Company’s financial position remains strong with cash on books @ 580 cr as on 30 Sep. Should be able to complete all the above mentioned capex from the cash in hand and internal accruals

Company is coming up with a new Child development center at Hyderabad, spread across 8k Sq Ft. Should go live in Nov 24. Will be addressing issues like ADHD, Autism Spectrum disorders and other early childhood psychological issues. These issues have become quite common these days, hence the need of specialised care

Q1 is generally their weakest Qtr and Q2 is generally their strongest Qtr of the year. Avg EBITDA margin for H1 was 31 pc. Company believes, the can sustain such margins for the foreseeable future ( within +/- 1 pc band )

In paediatric field, customers are generally more loyal to the Hospital brand and eco-system vs in other specialities where star doctors generally call the shots. This is an inherent advantage with the company

For their new hospital to break even ( in paediatrics space ), it takes about 30-35 pc occupancy

Company’s broad business split between Gynae + Obstetrics : Paediatrics stands @ 30 : 70

Disc: initiated a tracking position, biased, not a buy/sell recommendation, not SEBI registered

6 Likes

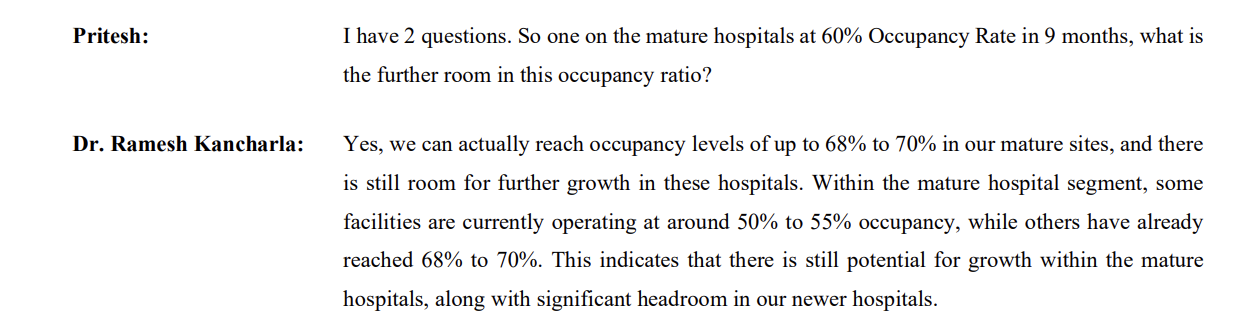

I was trying to understand why do they have occupancy rates only around 50%

i do know they have kept 30% of beds for NICU (complex cases)

but this 30% should have some backing & reasoning right, i mean if mgt has kept 30% beds aside they might be expecting these cases

but inspite of that the occupancy is only around 50%

so if we only have such occupancy, why can’t they tweak this 30% of the beds and make it more flexible for other normal usage as well

so in this way the occupancy can shoot up, while still catering well to NICU market.

1 Like

and also apart from that, they have entered the NCR region which is a proper greenfield expansion…180crs of Land and other 400crs of expenses for 400beds so the capex/bed for this will be around 14-15mn (all the other beds of rainbow is around 5-6mn/bed)

So did they mention anything regarding the expecting ARPOB from these 400 beds because that will help to us to understand how well they can utilize these beds to keep the ROCE intact in coming years because historically they always had superior return profile

1 Like

From the Q3FY25 concall. The Delhi-NCR hospital is planned to be positioned at a higher level with more international patients hence the higher capex / bed. So, expect stable state ARPOB to be higher.

Importantly this is a greenfield expansion so return ratios for this hospital would be depressed for a good 2 years or so due to front-ended costs.

2 Likes

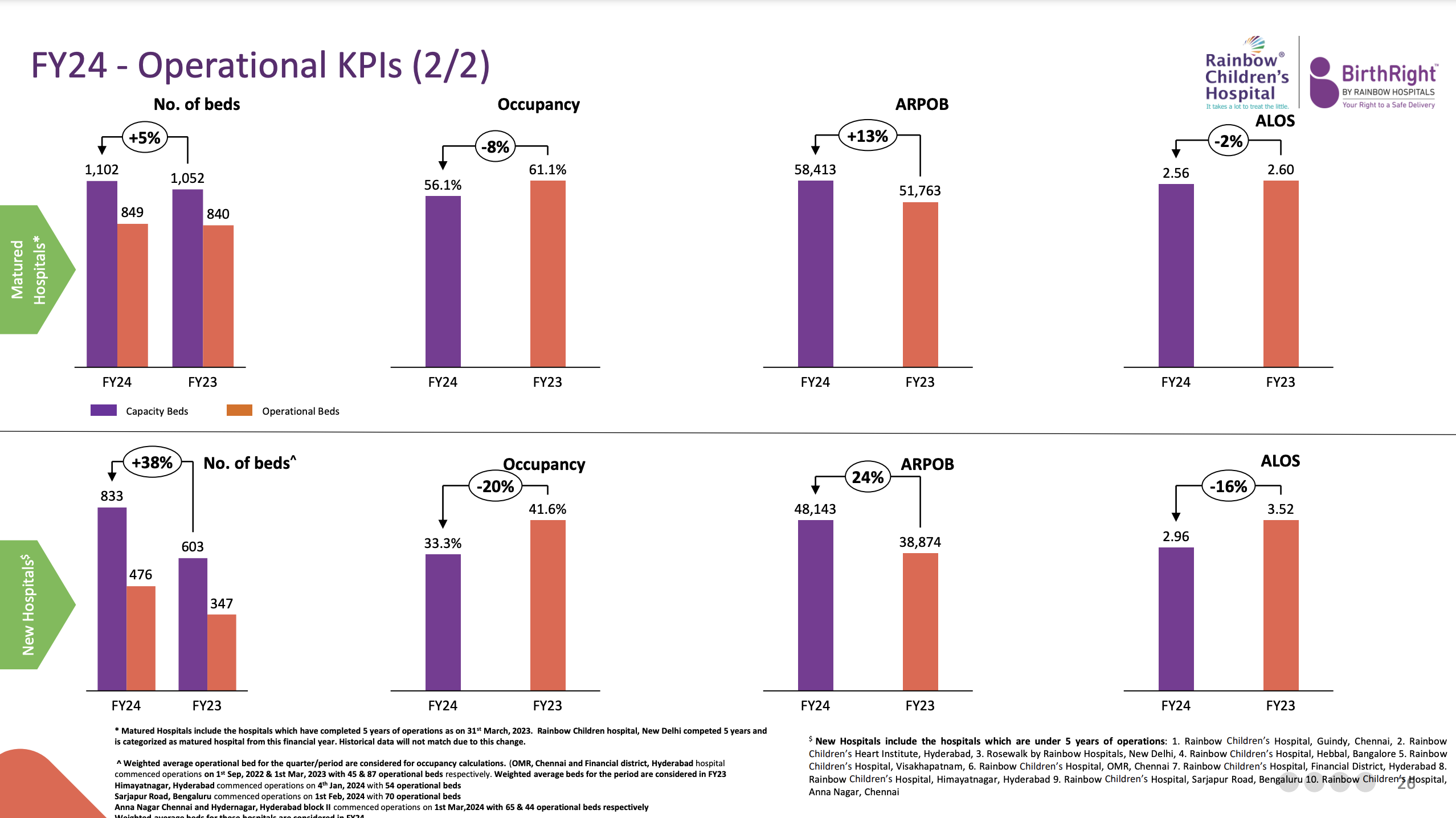

That is overall occupancy level. Mature hospitals have higher (~70%) with newer ones significantly lower (~35%) thus dragging the average down.

Mature hospitals:

Newer hospitals:

2 Likes

Rainbow Children’s Medicare -

Q4 and FY 25 results and concall highlights -

Company’s current footprint of hospitals -

Hyderabad - 8 hospitals + 2 Clinics

Bengaluru - 4 hospitals + 1 Clinic

Chennai - 3 hospitals

Vijaywada - 1 hospital + 1 Clinic

Vishakhapatnam - 1 hospital + 1 Clinic

Delhi - 2 hospitals

Combined bed capacity @ 1935 beds ( mature hospital beds @ 1237, new hospital beds @ 698 beds )

No of serving doctors @ 910

Q4 outcomes -

Revenues - 370 vs 341 cr, up 9 pc

EBITDA - 115 vs 105 cr, up 9 pc

PAT - 57 vs 51 cr, up 11 pc

Occupancy @ 46.5 vs 48.5 ( mature hospitals occupancy @ 52 pc, new hospitals occupancy @ 35 pc )

ARPOB @ 58.1 k vs 54.2 k

ALOS @ 2.77 vs 2.84 days

FY 25 outcomes -

Revenues - 1515 vs 1296 cr, up 17 pc

EBITDA - 490 vs 428 cr, up 14 pc

PAT - 244 vs 218 cr, up 12 pc

Avg growth in expenses like Depreciation, Employee costs, professional fees to doctors, finance expenses were @ 19 pc vs a 17 pc growth in topline

FY 25 occupancy @ 50.5 vs 47.9 pc

FY 25 ARPOB @ 53.9 k vs 55.8 k

FY 25 ALOS @ 2.85 vs 2.65

Payor profile for FY 25 -

Cash @ 48 vs 49 pc

Insurance @ 52 vs 51 pc

Region wise breakup of bed capacity -

Hyderabad - 940

Bengaluru - 442 ( another 150 beds are likely to come up in FY 26 )

TN - 270 ( another 130 beds are likely to come up in FY 27 @ Coimbatore )

NCR - 24 ( another 400 beds are expected to come up in FY 28 @ Gurugram )

AP - 259 ( another 100 beds are expected to come up in FY 26 @ Rajahmundry )

- Beds @ Malviyanagar are only managed by the company

Q4 was unusually weak ( vs a strong Q2 and Q3 )

Cash on books @ 700 cr. All the planned capex ( as mentioned above shall be funded via cash on books + internal cash generation )

Capex for FY 25 stood @ 145 cr

2 Hospitals / 124 Beds shall move from new to mature category by end of FY 26. New 250 beds @ Bengaluru and Rajamundry shall be added to new bed capacity within FY 26

Company’s IVF business grew strongly @ 70 pc YoY. They have started offering IVF facilities across 13 of their hospitals. IVF revenues in FY 25 stood @ 45 cr

Q4 saw unusual dip in revenue from paediatric division. Mothercare divisions performed as per expectations

Expecting the ARPP ( avg revenue per patient ) to grow @ mid - high single digits in FY 26. ARPP grew by 5.6 pc in FY 25 vs a 3.4 pc decline in ARPOB. ARPP is a better matrix to look at, since ALOS is beyond the Hospital’s control

Broad breakup of business @ 30 pc from mother care ( including IVF ), 70 pc from Paediatrics

Company incurred an EBITDA loss of 12-13 cr for FY 25 from the new hospitals it commissioned in FY 24. These hospitals should turn EBITDA positive in FY 26

Expecting FY 26 margins be similar to FY 25 margins

Aiming for mid - high teens revenue growth for FY 26

Since paediatrics is their mainstay ( and likely to remain like that forever ), some element of seasonality shall always be there in company’s Qtly results

Disc: holding, added more recently, not SEBI registered, not a buy/sell recommendation, posted for educational purposes only

5 Likes

Hi,

Can anyone help me understand the following points

a) Life Time Value of Child and Mother at the hospital: This includes from the 1st Trimester to the delivery and then follow ups and vaccination.

b) % of kids borne pre-mature resulting in better realization for the hospital

c) C - sec vs normal deliveries

d) % kids born with difficulties

e) are they into fertility treatment as well

g) are they planning to enter into management contract like hotels where asset cost is completely on the asset owner.

2 Likes

Rainbow Children’s Medicare -

Q1 FY 26 results and concall highlights -

Current portfolio of Hospitals + Clinics -

Hyderabad - 8 hospitals + 2 clinics

Bengaluru - 4 hospitals + 1 clinic

Chennai - 3 hospitals

Vijaywada - 1 hospital + 1 clinic

Warangal - 1 hospital

Vishakhapatnam - 1 hospital + 1 clinic

Delhi - 2 hospitals

Q1 outcomes -

Revenues - 352 vs 330 cr, up 7 pc

EBITDA - 103 vs 93 cr, up 11 pc

PAT - 54 vs 40 cr, up 35 pc ( due steep jump in other income on account of MTM gains on company’s debt fund investments )

Cash on books @ 735 cr

Q1 outcomes in mature hospitals ( > 5 yrs old ) -

No of Beds - 1371

Occupancy - 44 vs 49 pc

APPOB - 66 k vs 58 k

ALOS - 2.67 vs 2.80

Q1 outcomes in newer hospitals ( < 5 yrs old ) -

No of beds - 564

Occupancy - 31 vs 26 pc

ARPOB - 53k vs 49k

ALOS - 2.61 vs 2.58

Current bed capacity @ 2035 beds

Upcoming facilities in next 3 yrs -

FY 26 -

Bengaluru - 2 hospitals - 60 beds + 90 beds

Rajahmundry - 1 hospital - 100 beds

FY 27 -

Coimbatore - 1 hospital - 130 beds

FY 28 -

Gurugram ( Sec 44 and 56 ) - 2 hospitals - 325 beds + 125 beds

By end of FY 28, total bed capacity should reach 2865 beds. All these capex requirements should be met with internal cash generation by the company + the healthy cash balances that they have

Q1 is a seasonally weak Qtr for the company. Q2 and Q3 are the strongest Qtrs

Company’s acquired majority stake ( 76 pc ) in a hospital in Warangal to take its hospital count to 20 in Q1. Its a 100 bedded hospital

In advanced stages of finalising a new Greenfield hospital @ Pune. This Pune hospital should commence operations in about 30 months time

As the hospitals mature, the company migrates its Doctors to revenue share model. Its a win win for both the company and the doctors

Still confident of growing company’s topline in mid - high teens in FY 26 ( as 100 acquired beds have just gone live + 250 organic bed additions are lined up for this FY @ Bengaluru and Rajamundhry )

Once Pune Hospital is ready ( it shall act as a Hub hospital ) , company shall look to add more hospitals in nearby areas ( as spoke hospitals )

Also scouting for in-organic opportunities in NE mkts as well

Contribution to total revenues from IVF business now stands @ 3.2 pc

Warangal hospital’s ( recently acquired ) numbers shall be added to company’s consolidated results wef Q2. The current occupancy @ Warangal is around 30-35 pc

Drop in occupancy in Q1 in company’s mature hospitals was due to a weak paediatric season. However their tertiary and quaternary care business continued to do well - and hence the ARPOB and total revenue were higher despite a weak paediatric season. Seeing a descent pickup in paediatric season in Q2. The low ticket paediatric business is what brings in volumes but is a lower value business

Insurance : Cash mix @ 52 : 48

Disc: holding, biased, added recently, not a buy/sell recommendation, posted for educational purposes

6 Likes

Q2 results are out. Look good to me given their current expansion plans. Firstly, though occupancy in matured hospitals dropped by 16%, their ARPOB increased by 17%, meaning fewer beds generated more income ! maybe higher-value services? There is a very slight fall in margins but given their ramp up in capacity expansion, it doesn’t look bad. What’s more interesting is the metrics of the new hospitals. Major bed additions done without ARPOB dilution or fall in occupancy rates. Requesting other members to post their views please.

3 Likes

Rainbow Children’s Medicare -

Q2 FY 26 results and concall highlights -

Company’s current footprint of hospitals ( total - 22 hospitals + 6 clinics ) -

Hyderabad - 8 hospitals + 2 Clinics

Bengaluru - 4 hospitals + 2 Clinic

Chennai - 3 hospitals

Vijaywada - 1 hospital + 1 Clinic

Vishakhapatnam - 1 hospital + 1 Clinic

Delhi - 2 hospitals

Guwahati - 1 hospital ( acquired in Sep 25 )

Rajamundhry - 1 hospital ( went live H1 )

Warangal - 1 hospital ( acquired in Jun 25 )

Total bed capacity @ 2285 vs 1935, up 18 pc YoY

Q2 performance indicators -

Revenues - 445 vs 417 cr, up 7 pc

EBITDA - 149 vs 147 cr, up 1 pc ( margins @ 33.5 vs 35.2 pc )

PAT - 75 vs 79 cr, down 4 pc

No of deliveries - 4753 vs 4451, up 7 pc

Occupancy - 52 vs 59 pc, down 13 pc

ARPOB - Rs 57.4 k vs Rs 49.7 k, up 15 pc

ALOS - 2.73 vs 2.93 days, down 7 pc

Mature hospitals( > 5 yrs old ) -

Occupancies - 55 vs 66 pc, down 16 pc

ARPOB - Rs 61 k vs Rs 52 k, up 17 pc

ALOS - 2.76 vs 2.98, down 7 pc

New Hospitals( < 5 yrs old ) -

Occupancy - 44 vs 44 pc, flat YoY

ARPOB - Rs 48.5 k vs Rs 41.6 k

ALOS - 2.66 vs 2.81, down 5 pc

Payor profile - Cash : Insurance @ 47 : 53

H1 outcomes -

Revenues - 797 vs 747 cr, up 7 pc

EBITDA - 252 vs 240 cr, up 5 pc

PAT - 129 vs 118 cr, up 9 pc

Have acquired 2 hospitals in H1 - Warangal ( 100 beds ) and Guwahati ( 150 beds )

Capex pipeline -

150 new bed additions shall happen in H2 @ Bengaluru @ Hennur ( 60 beds ) and Electronic City ( 90 beds )

130 bed hospital is expected to come up in Coimbatore towards the end of FY 27

2 Hospitals are slated to open @ Gurugram in Sec 44 ( 325 beds ) and Sec 56 ( 125 beds ) in FY 28

150 bed Pune hospital shall come up in FY 29

As the hospitals mature, the company migrates its Doctors to revenue share model. Its a win win for both the company and the doctors

Low incidence of seasonal illnesses in Q2 led to a soft Qtr - both wrt profitability and revenues

Both Warangal and Guwahati have now been fully integrated with Rainbow hospitals

The Electronic City Bengaluru hospital is ready and waiting for Govt’s approval to commence operations

International business is clocking 3 cr kind of monthly revenue

Cash on books @ 556 cr. Should be able to finance all the a/m capex from the cash on books + internal accruals

AP, Telangana, Karnataka - mkts behave in a similar fashion wrt seasonality. Chennai is slightly different. NCR and NE are completely different ( wrt peak infection / illness seasons )

Company’s IVF business grew 40 pc QoQ ( although the current base is low )

If seasonal infections are high - a lot of children pick up disease like Pneumonia which require intensive care. If the seasonal infections are low, naturally the loss of business is commensurate

Q2 revenues from IVF segment were about 13 cr. Should be able to clock 40 cr kind of revenues from IVF business in FY 26 ( this segment should keep growing at a brisk pace )

Guiding for a 20 pc revenue CAGR for FY 27 and FY 28

Since company is cash rich, they ll continue to look @ M&A opportunities to keep driving higher growth rates

Company’s 30 pc of business comes from Tertiary + Quaternary procedures ( like Paediatric Onco, Paediatric transplants etc ). Most of this business happens @ their Hub hospitals ( & not at spoke hospitals )

Company aspires for International patient’s business should contribute to 10 pc of their topline in next 5 yrs

Pricing @ Tier-2,3 cities are 20-30 pc lower than their Tier-1 hospitals. But overall margins are similar because the cost structures are also lower

Disc: holding, biased, not SEBI recommended, not a buy/sell recommendation, posted only for educational purposes

6 Likes

Hi all, I have been tracking the business operations & performance of Rainbow Children’s Medicare Limited for some months now. I have prepared a detailed research report regarding the same. Would love for the community to have a look at it! Any feedback or error detection is welcome. Thanks!

Rainbow Children’s Medicare Limited - Valuation.pdf (4.3 MB)

Disc: Not holding any position/ not a recommendation to buy/sell, posting it solely out of interest and educational purposes.

9 Likes