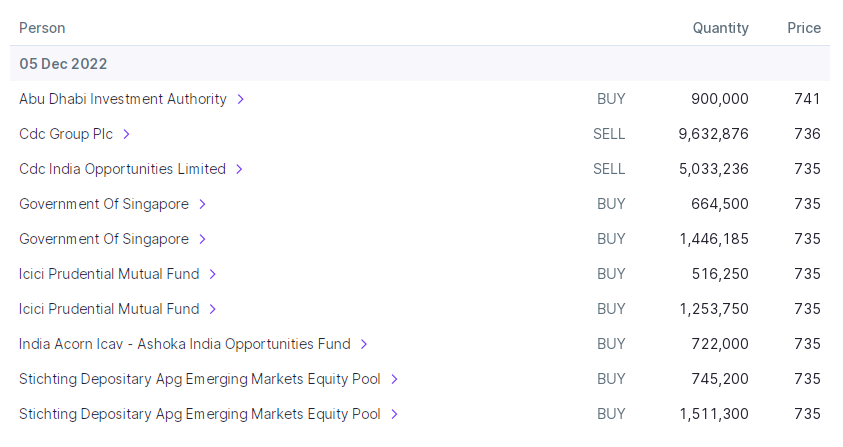

CDC , PE Investor is selling and other FII and DII is buying.

8 Likes

Thanks Gourab for your valuable inputs. Rainbow is coming out a spoke in HSR with 50 beds in Bangalore in FY 24.

2 Likes

Because British Intl Inv PLC group (9.49%) has been moved to public. otherwise 0.81% increase in DII holding and 2.41% increase in FII Holding…

3 Likes

Anecdotal experience:

Rainbow Hospital is go-to hospital for kids in my case in Hyderabad. Most in my neighbourhood also prefer it for their kids. As a matter of fact, during early days, our primary doctor used to be Dr kancharla. Despite good quality and first hand experience, I missed to follow the golden rule of investing in companies and products that one likes/consumes. (I just did today).

Coming back, I am not sure how it is in Bangalore/Chennai but my observation in Hyderabad is that the area where Rainbows operates is basically IT hub. Young parents want quality healthcare for their kids and aren’t too concern about the money as such. Also most are insured. That doesn’t mean Rainbow is brutally expensive but just wanted to share the kind of demography they are serving here. Is it part of their strategy? I don’t know.

9 Likes

Same view, The main hospital in Bangalore is near the Baghmane Tech park. This area is filled with people working in Google / Amazon / Visa etc.

Cost wise, they don’t seem to extract money. In fact I found the doctor quite empathetic. In the last 5-6 months they have also hired some of the well known gynae, pediatrician etc .

5 Likes

If you see Rainbow hospital Balance sheet Building cost in asset is aprox : 822 Cr & land is 4 Cr.

if i compare with other listed hospitals also its too high.

how they can construct 4 Cr land 822 Cr building.

Are taking land for lease to contract buildings ?

Please some one try to explain me .

I holding this stock.

Hi 9916673623,

The numbers that you see under fixed assets, so first let’s understand what is fixed assets. Fixed assets are long-term assets. This means the assets have a useful life of more than one year. Fixed assets include property, plant, and equipment (PP&E) and are recorded on the balance sheet with that classification.

So in your question, you see 822 Cr. is for Building that is already built and they have land that has a market value of 4 Cr which can be used as a brownfield expansion in the future if it is in the same city.

2 Likes

3 Likes

5 Likes

Marcellus seems to have built in large position in Rainbow

2 Likes

Hello friends,

Wanted to highlight below points on Rainbow Children’s Medicare -

-

Initially started in Hyderabad and achieved phenomenal success. Management was able to replicate their proven model in other cities - Bangalore and Chennai. Now, even Delhi is tracking well and that gave them the confidence to plan hub in Gurugram (Hub - 400 beds - 450cr greenfield capex)

-

Rainbow’s hidden moat is their doctor engagement model, children-friendly environment and robust tertiary level services. No competition w.r.t these factors and it is not easy for new entrant as children’s healthcare needs to be built very organically.

-

Any city with a 40-50 lakh population definitely requires min. 200 beds hospital to cater to critical care and specialties. Opportunity is huge, but it takes time to build it as children’s healthcare is organic.(In a way entry barrier)

-

Rainbow’s target base is critically ill children or complex problems where there is miniscule competition. Small children’s hospitals won’t be their competition. In fact they will refer to rainbow for complex cases.

-

None of these mother and child hospitals can actually build pediatric intensive care because this model is lot more complex and intensive care takes time to build. Rainbow has a very different play in this space.

-

Breakeven in children’s multispecialty at 30% occupancy (This is much better compared to general multispecialty).

-

Q2 and Q3 are generally peak season for pediatric business.

-

TAM to double at 14% cagr to 1,78,400cr by 2026

-

I believe Rainbow has best in class metrics compared to listed hospitals (capex per bed, ARPOB, ALOS etc). Eventually market might reward it with premium EV/EBITDA multiple.

Disclosure: Invested, and Not a Reco.

13 Likes

this transcript detail is of which month ?

Hello,

It is not a single earnings transcript. I went through all the available quarterly transcripts and saved the snippets.

Thanks

3 Likes

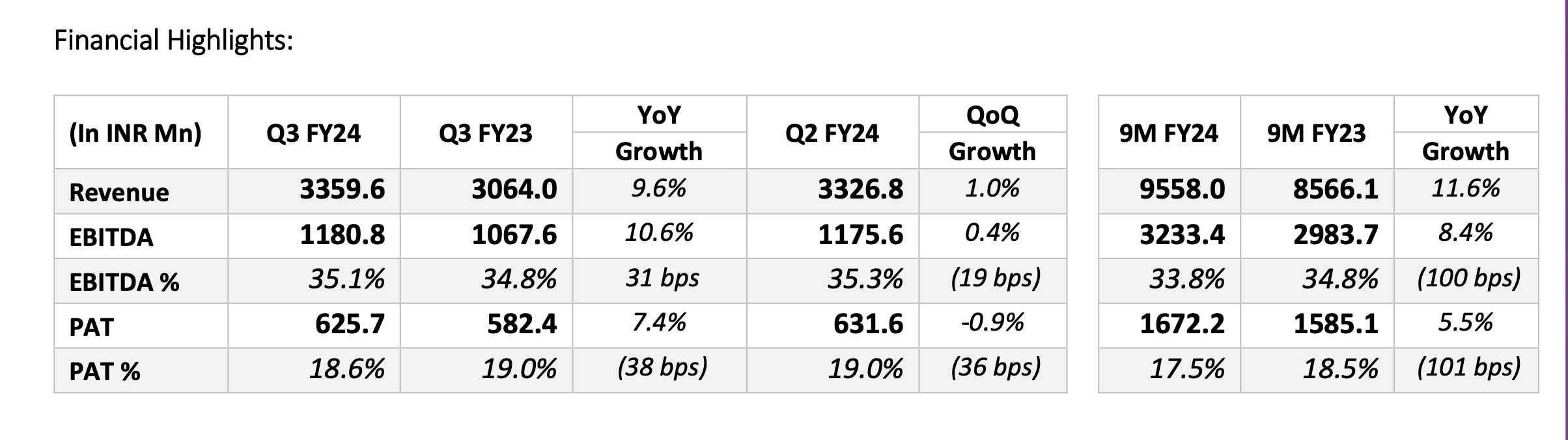

PAT grows 2.7% YoY

Results are very bad. Q2 and Q3 are the best quarters. Chance of multiple de-rating

Market expecting straight line profit growth?

Yes planning to exit on fundamental triggers:

- Topline growth guidance shift from 18-20% to mid-teens

- Slight decline expected in EBITDA Margins (new hospitals will take time to break-even)

- High Depreciation due to significant capex plans

7 Likes

In the recent concall, Dr. Kancharla says that an occupancy of 55% is what they aim for at the Company level, considering the facilities of ICU, Isolation wards etc have to be kept restricted and they cannot keep child patients where the women patients are kept.

It is understandable from logistics point of view.

Now my question is, if I know out of 100 beds, I am only looking to use 55-60 beds on an average then why should I keep 100 beds at all? I can use the space to accomodate 80 beds, per se, leaving me with more area and better patient service. This way I save on capex and maintenance as well.

He also says that cannibalisation and competition from smaller sized hospitals is also there. So shouldn’t this also prompt them to not have too many beds in a single facility?

Looking for guidance on these aspects, as Hospital space is not that well known to me!

Do you know whats the occupancy of Max health care hospital? Do they face similar issue?