Check this

1 Like

May I know how is Iron ore surge help the Aluminium player like Rain?

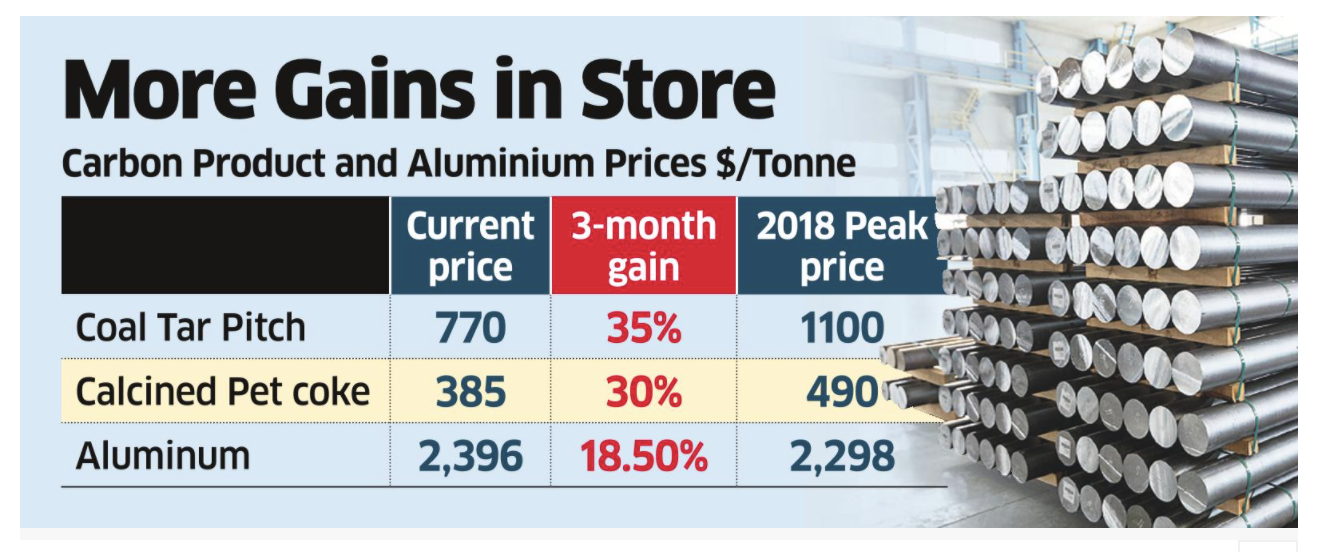

The article I posted mentions that aluminum prices are reaching all time high of the last supercycle. I was just pointing to the rally is still intact.

2 Likes

Rain has a large re-rating trigger in the fact that they are at the end of the capex cycle and now the operating leverage will kick in. And now that there is a potential supercycle in commodities in general and aluminium in particular at the time when Rain has its largest unutilized capacity, I think its a matter of time before we see a 2017 type rally.

3 Likes

Here’s the article on Rain industries, do we have anyone who has subscribed, who can summarize it for others ?

Many thanks,

Karan

1 Like

I have ET-Prime, sharing from this piece:

Q1 results are tomorrow! Let’s see if the expected operating leverage is starting to kick in

4 Likes

I am holding this gem since 2019 but in past they had one or other things which impacts their results in bad way just to name few high cost inventory,Netherlands plant shutdown, inventory write off, hurricane, etc.

Not to mention, their every capex plan is delayed by min. Few quarters if not more.

Also they did not update or did not get any response for GPC allocation quota for new Vizag vertical shaft plan. In concall they mentioned they are expecting response from AP govt in next 4 weeks from 25th Feb.

I am not able to see concall invitation for this quarter result - not sure if they have scheduled one.

Though I am hoping good to great results tomorrow.

Disc. Significant holding.

1 Like

Q1 2021 results are out. PAT @ ₹ 2.15 billion and Adjusted EPS at ₹ 6.40

Please note that Last Quarter, there was a special one time profit from sale of a small unit. So QOQ will look skewed. YOY, net profit has almost doubled. Results are excellent and I fully expect it to post even better results in the coming years.

5 Likes

Management’s comments for q1cy2021. Though not much additional details being said than investor presentation. There is no concall for previous quarter.

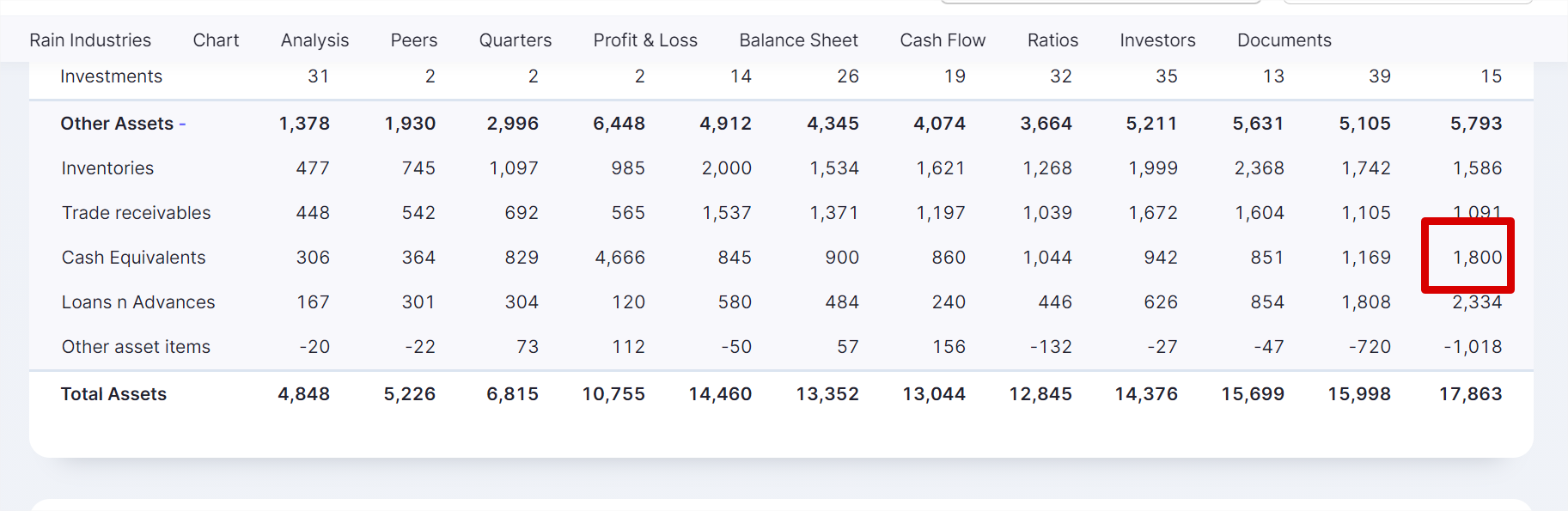

Hi, I was looking at rain industries in screener. It is showing cash equivalent of 1800 cr. Does anyone know how to confirm this number?

I also have one doubt…

Cash holding as per Dec 20 is shown as 1800 Cr. Cash holding during the increased from 1169 Cr. to 1800 Cr. At the same time, Debt during the year also increased from 7845 Cr. to 8859 Cr.

Unable to understand this logic that despite of increase in cash company didn’t reduce the debt instead borrowed further from the market…

Why to borrow money from market if your cash holding is increased during the year?

Expert views are invited…

Thanks

1 Like

I heard in one of past interview from management that they are getting loan at very low rate(i guess 4-5%) and getting return more than what they are paying as interest. So they dont want to pay the loan and want to keep borrowing for growth. I might be wrong though.

3 Likes

The debt taken by the company is in US dollars and Euros, so while preparing the presentation or reporting the financial numbers they have to convert it to rupees. This difference is mainly due to currency fluctuations.

Since Rain industries is a high working capital company so it doesn’t make much sense for them to pay debt with all the cash they have.

As par as the debt payment is concerned, company has said it repetitively that thier major long term debt repayment will start from march 2022 and they don’t want to incur penalty by paying it off early. It’s evident from the current quarter results that they have started reducing working capital debt.

9 Likes

Rain industries added to the MSCI small cap index.

1 Like

Correction:

Looks like it’s not added in MSCI small-cap index. CNBC reported it incorrectly.

1 Like

Could this increase aluminium demand in long term?

Thanks!

6 Likes

More details about it below

1 Like

As Rain industries belong to carbon products, They have any plan in to any graphene products, such as battery coating, EV etc?

They manufacturer resins by the name PETRORES for Lithium-Ion battery coatings

1 Like