Thanks, but Rain is the leader in carbon products, and stong R&D teams, as graphene is a carbon products and going to do the magic in charging batteries, storage etc, any news that rain gonna do somthing about graphene, I have read last 3 annual reports, but could not find the name

As far as my understanding with Rain business goes they are currently not into Graphene, the touch point of EV in the context of Rain industries is the manufacturing of Resins - PETRORES.

Disclaimer : Invested

1 Like

Lake Charles recorded the third heaviest rainfall in history according to the National Weather Service

Read More: Lake Charles Hit With Third Highest Amount of Rainfall in History | Lake Charles Hit With Third Highest Amount of Rainfall in History

Rain has got CPC plant in Lake Charles. No public filing yet - so good chance that no impact to plant yet.

3 Likes

Sure @Ajjugattu, but Rain has been his favourite stock for sometime now. It’s almost his biggest claim to fame in India. He had repeatedly spoken about how Rain’s moat is growing. And so I’d like to believe that his understanding of the business and access to information is higher than most people.

His selling stake is a significant event for me and I’d want to understand what led him to do this. Is it just better opportunity somewhere else (since he had sold Kolte as well), or does he see some fundamental change. Will be on the lookout for more information.

In the meanwhile, no change in my holding as the commodity rally seems in tact and Rain is well positioned to exploit it.

In this session, he talks about Rain from 30mins onwards, where he concludes that it not a fantastic business but has very good management and he bought it very cheap, so downside was capped. If he’s selling his stake it may mean a better alternative for him.

4 Likes

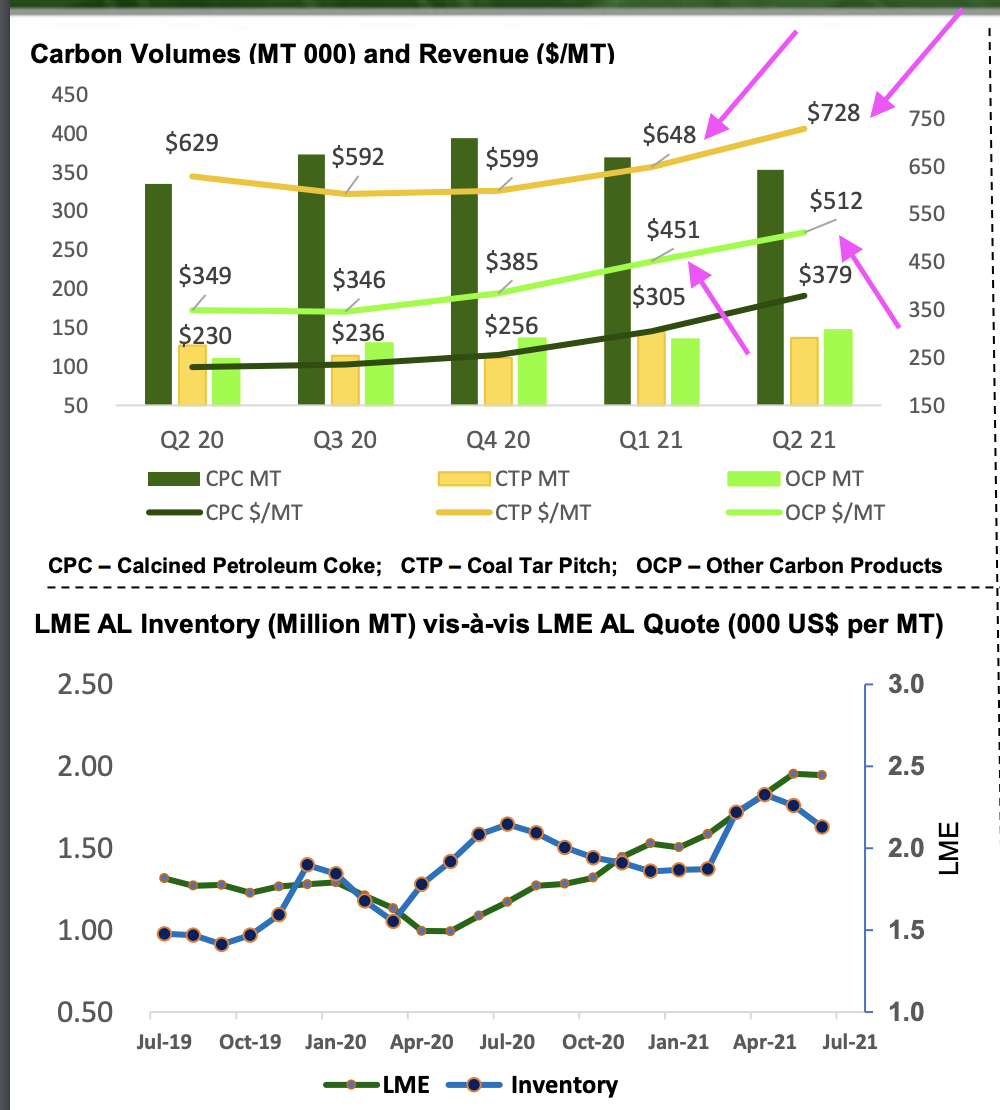

I agree with the fact with CPC and CTP prices are moving up. But we can not ignore the fact that GPC ( feedstock) is also very significantly up. In the transcript it was mentioned that GPC is scarce and the prices have shot up. Is Rain able to expand its margin spreads?

Can some one throw more light on this?

Are they able to source their GPC raw material at such rates which have improved margins?

Thank you

1 Like

Rain is having acp technology which allows it to use low grade gpc for cpc production. They are setting up this plant in India and usa. It’s all being better than the competitor. If they can gain market share with cost leadership then they will get pricing power.

4 Likes

Yes, I saw that.

So the CPC prices in China are up from $200/T in Jan 2020 to $450/T now and GPC prices are up from $150/T to $360/T.

Based on my understanding, presently Rain is sourcing their GPC externally (as APC plants not functional yet)?

So has this reduced margins? Or is GPC cheaper in India and USA.

Please correct me if I’m wrong.

Thanks

2 Likes

Hi All,

Can anyone who is tracking Rain closely provide the current CPC price.

Thanks

1 Like

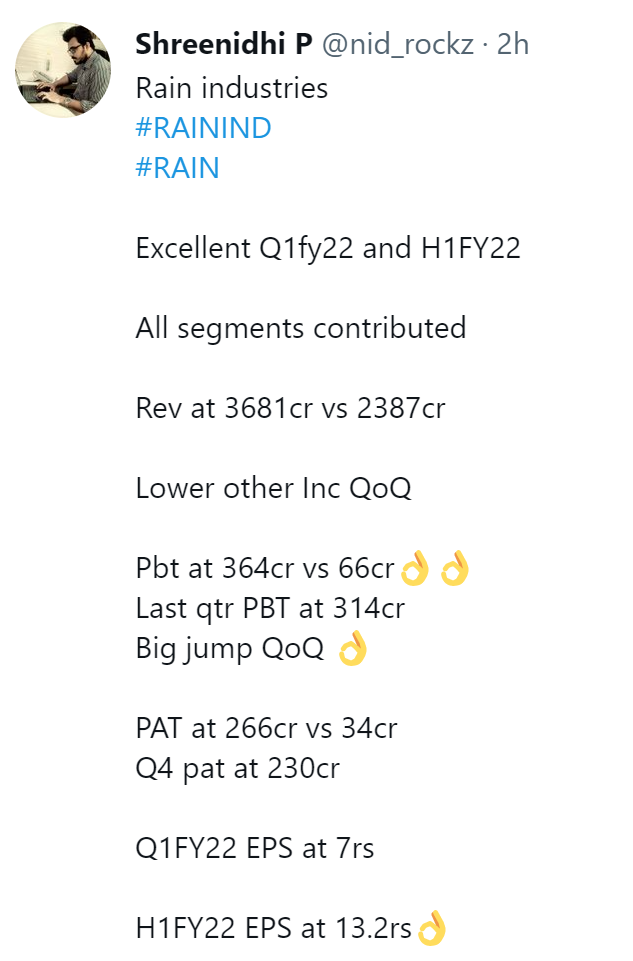

Although the results are looking like bumper results, given the cyclicality of the business we should (in my opinion) take in to account/note that last year, with covid most of the factories/clients were either closed or not operational 100% - thus demand was low, meaning it had a low base effect. So we should take the YoY results with a pinch of salt.

Look at the increase in price realization:

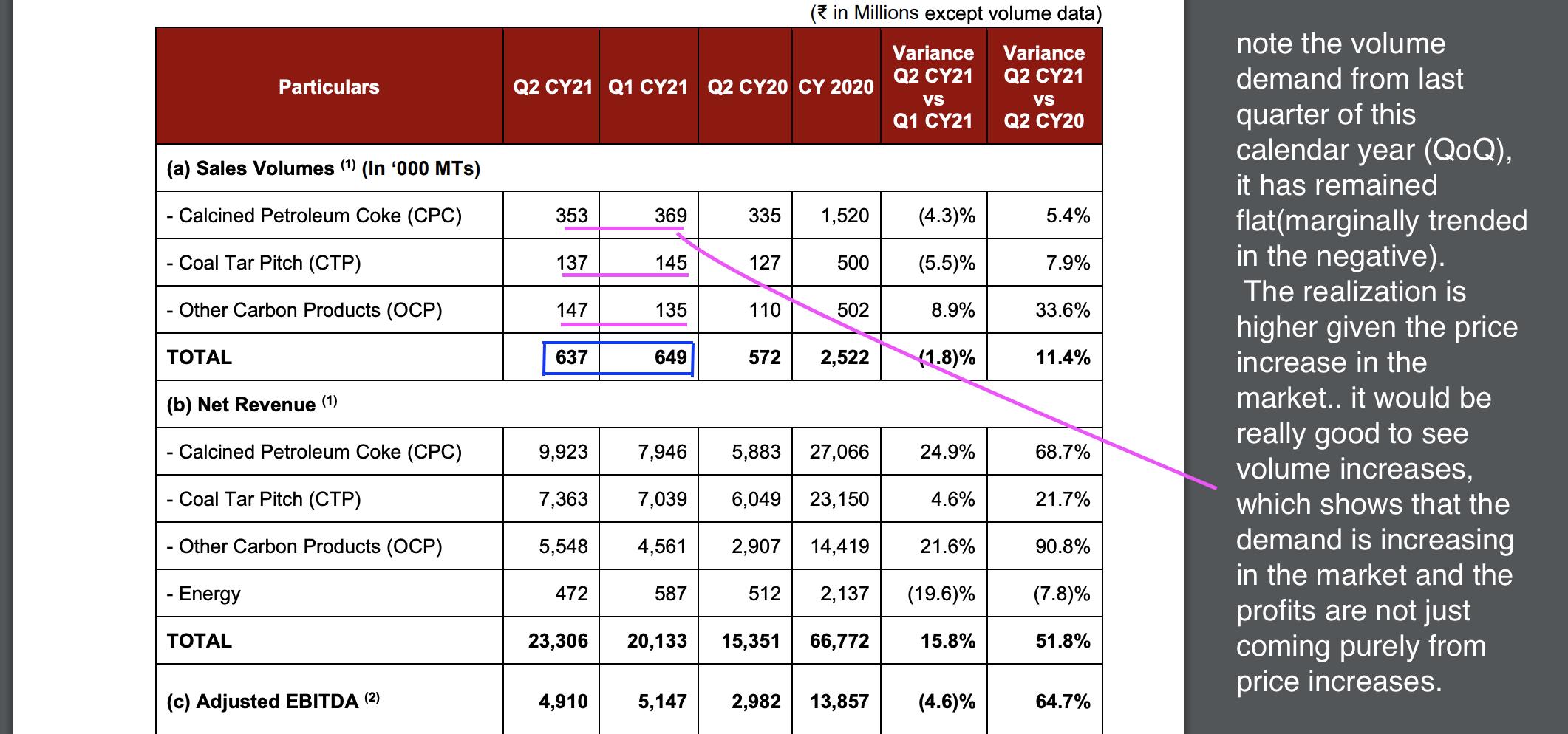

Carbon segment: QoQ the volume is relatively flat. This segment is the heavyweight from a revenue perspective for the company (roughly 65% of the revenue from this qtr)

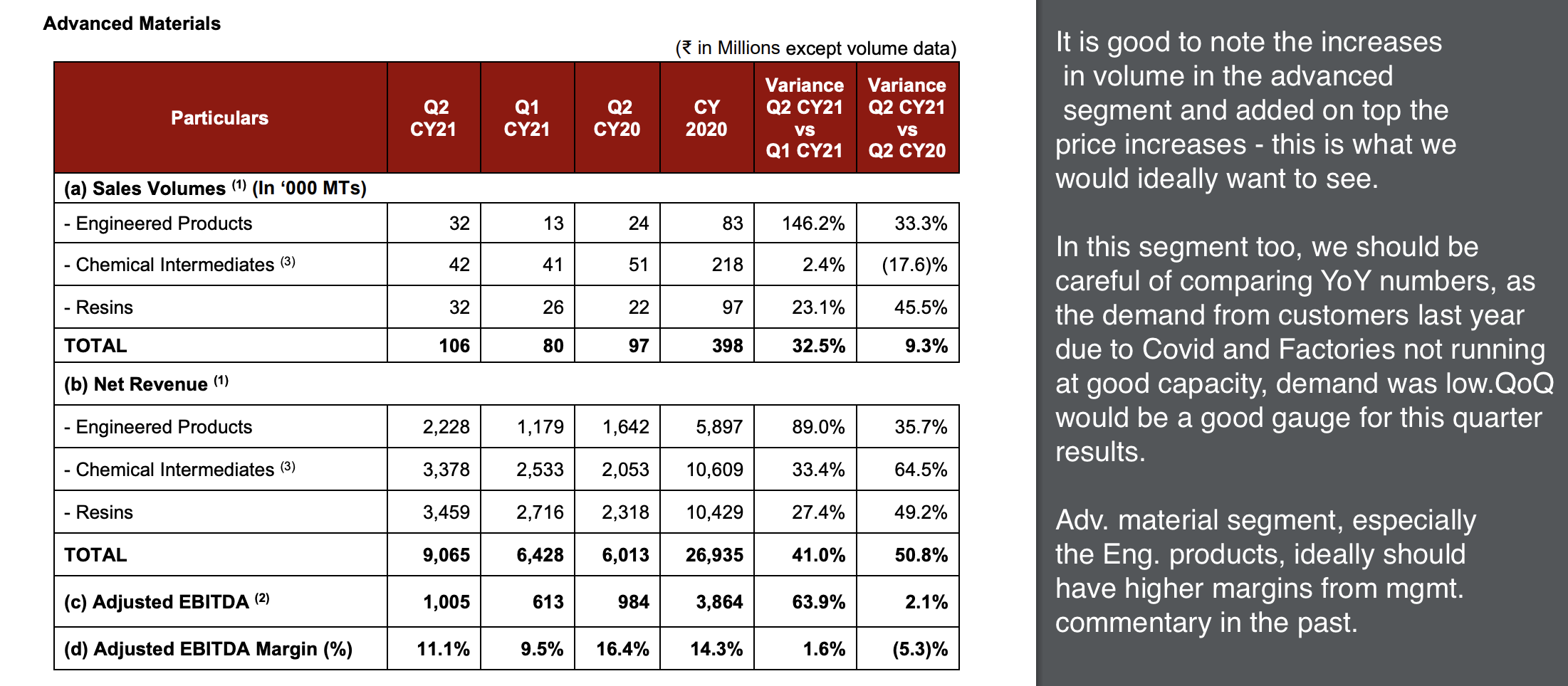

Advanced Materials Segment:QoQ the volume has increased

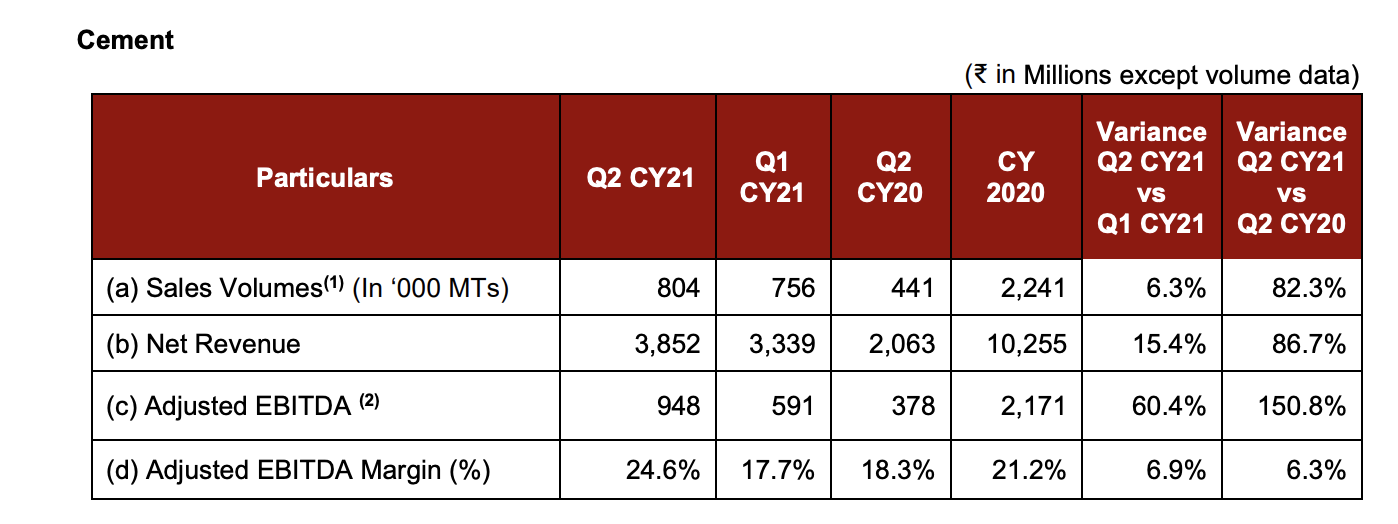

The cement segment has done well, which is a good sign:

15 Likes

Q2 CY June 2021 Earnings discussion

5 Likes

2 Likes

Results:

- Revenue from the Carbon segment increased by ~60.4% YoY. Although the volume was pretty much flat compared to last year (613 vs 617 YoY and 613 vs 637 QoQ). Realization were higher since RM and carbon products prices have gone up.

- Revenue from Adv. Mat. segment increased by 34% YoY. Volumes were marginally up (114 vs 105 YoY, 114 vs 106 QoQ). Avg. blended realization has been higher by approx 23.5%.

[One thing worth noting in the update was volume contribution in this segment from the HHCR plant.] - Revenue from Cement segment increased by 20% YoY - volumes have increased by 25% but realization is down by 4%

HHCR: 2400 MT of water white resins sold - 5% increase QoQ

To monitor: utilization of this plant and incremental contribution towards margins ( volume and value).

ACP plants -

USA plant to commence next quarter

Indian plant - still no signs of start, mgmt. commentary is recommence in early 2022 now.

I would reiterate again that we should take the YoY comparisons with a pinch of salt as 2020 most of the factories were shut down or slowly reopening at this time. QoQ the margins have gone down by 90bps for Carbon segment and 200 bps for Adv.Mat. Segment.

Looking broadly the demand has started to pick up, AL is at multi-year highs and a few more smelters about to restart.

Presentation: https://www.bseindia.com/xml-data/corpfiling/AttachHis/78097658-38dc-4560-a747-708db6d91848.pdf

10 Likes

Have they stopped doing concalls ?

Yes, this is 2nd quarter where we did not have concall. I had word with IR team and they mentioned that they have added management commentary (questions were sent by investor over mail) and discussion for which you can find recordings on company’s website and also you can find link in exchange fillings.

Though I am not sure if it is effective way as they can avoid hard questions.

Thanks,

1 Like

Pabrai loading up more RAIN.

4 Likes

Hi

Can you talk about who are the customers of Rain Industries in India?

Can someone discuss the impact on the business of rain industries if there is a sanction on Russia by USA? Thanks!