Al production has increased substantially and the prices are not showing signs of topping out.

Norske Hydro expects 20% increase in Al sales to auto companies.

Multi-material vehicle construction, onslaught of electrified powertrains and battery electric vehicle platforms drive aluminum’s increased market penetration

A new survey released by DuckerFrontier confirms aluminum, already the fastest growing automotive material, is expected to grow to content levels of 514 pounds per vehicle (PPV) by 2026, up 12% from 2020 levels.

Further, Doors represent the single highest net growth application of aluminum content per vehicle with penetration reaching 30% by 2026. Also, by 2026, aluminum hood penetration is expected to reach 81% and liftgates/tailgates reaching 44%. By 2030, total aluminum content is estimated to reach 570 PPV, a 24% increase over the next decade.

Not sure how to read this. Profits up to December 2017 levels, largely on the back of other income, most of which was from the sale of Rutgers. Operationally seems to be largely flat. Debt seems to have increased partially as well.

The global base metal industry has had a lot going for it over the past six months as a rapid rebound in economic activity and surging commodity prices have titillated investor interest. On Wednesday, US President Joseph Biden further buttressed investors’ optimism after announcing plans for a $2.25 trillion worth of infrastructure spending over the next eight years.

The plan will focus on rebuilding the US’ creaking physical infrastructure as well as creating the foundation of a cleaner technology in the country as Biden looks to further his party’s climate change causes.

The infrastructure spending in the US could compliment the strong demand emanating out of China, which has been supporting global commodity markets during the pandemic year, said analysts. Following Biden’s announcement, the Bloomberg Commodity index rose nearly 1 per cent.

At home, the Nifty Metal index surged over 5 per cent to a record high as investors’ optimism for the sector rose further on perception that the infrastructure spending in the US will boost revenues from exports for Indian companies.

In an environment where demand from China and US will be strong, not to mention the domestic market where investors are expecting the restart of the investment cycle led by the government, profitability and revenues of metal producers are likely to surge, said analysts.

“I believe that the current cycle resembles the 2002-2008 cycle where commodities did well and while the commodity user industry did not do that well,” S Naren, chief investment officer at ICICI Prudential AMC told ETNow.

The infrastructure plan in the US and the Indian government’s plans for large capital expenditure are not the only thing working in favour of metal companies. On the supply side, several base metals are suffering from chronic underinvestment in finding new sources of minerals as well as China’s renewed focus on reducing its carbon footprint.

One metal that is seeing a roaring bull market is steel where both demand-side and supply-side factors are making investors exuberant. “Tightness in supply due to supply-side issues and production curbs in China has helped regional steel prices inch up further,” said brokerage firm Motilal Oswal Financial Services.

Motilal Oswal Financial Services believes that steel producers at home will increase their prices in the coming days given the increase in steel export prices in South Korea and China – the other two large exporters in Asia.

Rain Industries is having reserve more than 5400cr, But still they are not paying debt which is around 8600cr, if they can reduce the debt at least 3000cr, the stock will move much

Management is focussed on long term, stock price is determined by strong growing business , management focus should be on growth and business quality and not stock price, stock price will follow eventually , if as a businessman , I have a business which values 100 Rupee and I borrow 100 rupee and reinvest and make 15% out of new total entity then even though my borrowing look very high initially, but with 15%-20% growth compounding the loan will start to look very small over long period of time , or debt/equity will keep shrinking over the period of time.

@unni Reserves in the balance sheet is not cash. Is a part of shareholders equity (book value) on the liabilities side. Look at cash and equivalents on the assets side to know the real cash on the books.

6/10 Triggers for Rain’s Future ROCE/ROIC (according to the Variant Perception Framework)

Deleveraging Debt Profile:"If you look at our debt, we have one billion dollars, but our net term debt as of December it’s only about $800 million plus. In the last seven-eight years we’ve been continuously investing in projects and we want to bring that down, and we should have improved cash flow both from our normal cash flow as well as contributions from these new projects should improve cash. So, based on that, our target is to reduce the debt in the next few years and I cannot comment on how much exactly we can pay but we do expect that it should come down. Our target Debt-to-EBITDA ratio should be to bewell below 2.5(~from 3.5 currently~) as soon as possible and we want tobring down our average interest rate to about 4%which we are hopeful that we can do it in the next one and half years" ~ Jagan Reddy, Vice Chairman

Product Mix Change:

Researched and now manufacturing new downstream, high-margin speciality materials of the Future like CARBORES, PETRORES and NOVARES

Incorporation of new subsidiaries like Rain Verticals, to research and develop vertical farming, logistics and lithium-ion batteries

A shift away from it’s previously cyclical, commodity-only identity

Capital Expenditure (Capex):

~ $100M of capex every year has come to an end

Built a new HHCR chemicals facility + 2 new ACP plants + 1 new vertical shaft calciner + desulphurization units

Finished it’s major capex cycle, right at the start of a commodity supercycle when most metals manufacturers (Rain’s customers) are announcing capacity expansion plans

Industry Cycle:

Commodity prices of Aluminium (globally smelters restart over Aluminium LME at $1600 ) and Calcined Petroleum Coke are

Cement prices and volumes are

Coal Tar Pitch volumes due to graphite electrode industry

Titanium Dioxide for the paint industry

Carbon black for the tyre industry

Margin Expansion:

Capacity utilization across the carbon products board has been ~60% for the past 2 years. With the ramp up in demand, utilization is expected to cross 80% and lead to huge economies of scale in production

New advanced materials hitting the market have an expected ROCE of 30%

Cost Reduction:

Lower input costs by the planned mixing of engineered ACP in the production of CPC. Partially de-risks from highly variable Green Pet Coke (GPC) feedstock rates

Interest reduction from deleveraging debt (after the sale of two non-strategic subsidiary companies, which are engaged in manufacturing and distribution of polynaphthalene sulfonates, under product-group naphthalene derivates, in Dec 2020)

Capex savings from the end of Rain’s extended capex cycle.

Thanks Anirudh, great analysis. Completed capex, increasing utilization, expanding margins and growing end user industry demand smells of high potential operating leverage. Would love to hear @Worldlywiseinvestors thoughts on this!

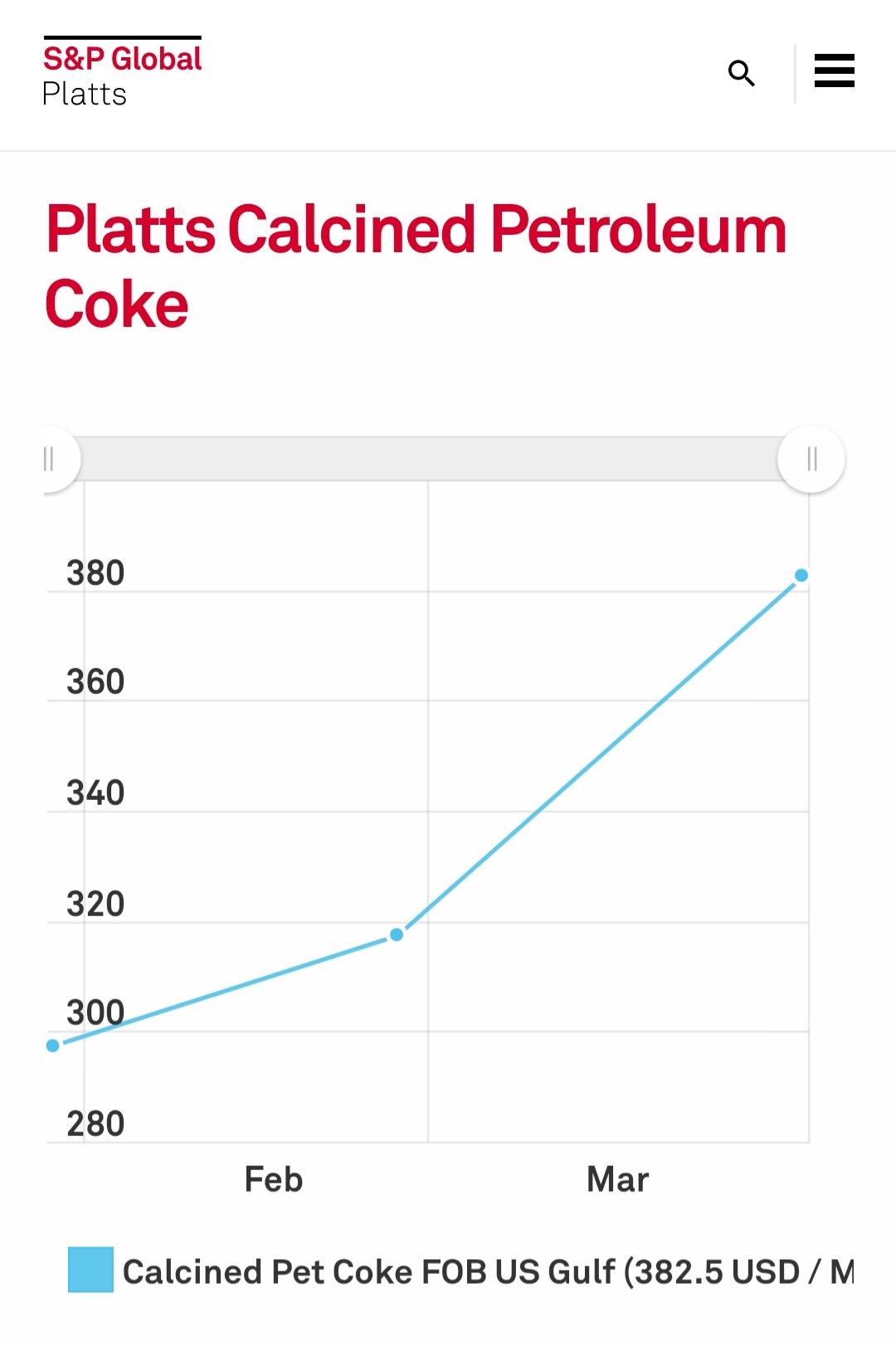

Missed adding a Calcined Pet Coke (CPC) rates graph in the earlier message! Would love other Rain investors opinions on how you’re seeing this story play out now.

One more tailwind to add - Joe Biden has announced $2.3 Trillion plan for spending on Infrastructure. Besides US is more and more keen to source material locally to given rise to local manufacturing.

Article indicates the optimism about rain’s business during this decade(based on their annual report), US opportunity and Aluminum touching its highest levels since 2018