Good write up, would you be able to provide any details on where are we with the aluminium cycle, as you know if the cycle turns up and more manufacturers produce aluminium the demand of CPC/CTP would go up potentially as this would be a key trigger for Rain.

hi @ganeshrpl, Ok, 6-7% is not a really a big percentage. As you mentioned below lines, that’s shall be their ability & competitive advantage to tackle the possible emerging competition in that area.

Gas leak at LG Polymers Industry in RR Venkatampuram village in Vishakhapatnam.

3 people including one child died, evacuation underway.

Its major gas leak tragedy, people in the proximity of 5/6 km running away for their lives.

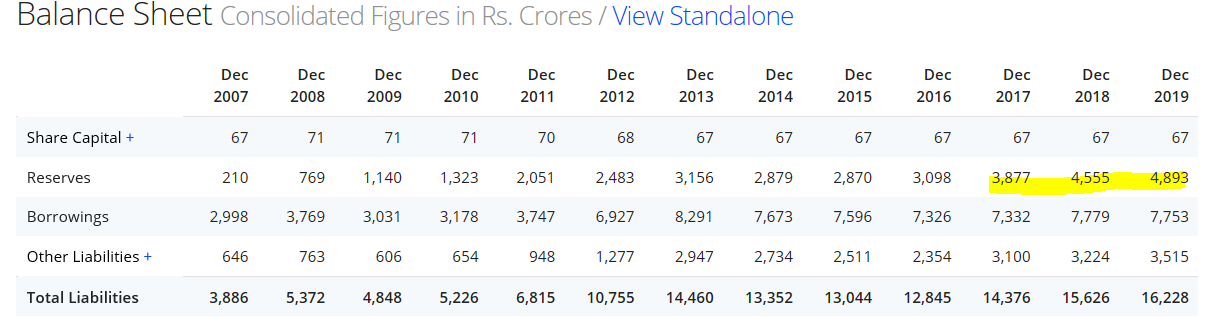

Gross Debt without Working captial is US $ 1060 Million which is 7950 Cr repayment in Year 2025.

Finanace cost each year paid is only the interest.

Lets say the average PAT each year is 500 Cr.

Worst case : 2020 is washout year, 5 year to 2025.

Consolidated PAT : 5*500 = 2500 Cr.

But Debt repayment is 7950 Cr in 2025 and Consolidated PAT is 2500 Cr. ( Cash end of CY 2019 is 164 US$ Million or 1230 INR Cr)

How will the company repay its debt ?

If my thinking /calculation is wrong please correct me.

Looking forward for your views.

I think one should look at Cash from operating activities not net profit

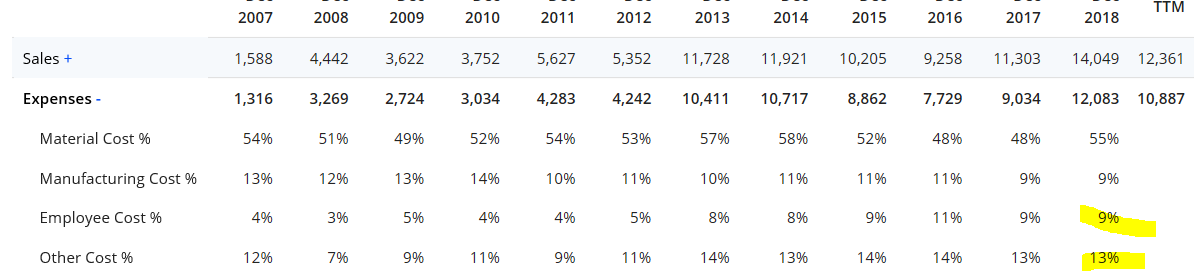

So average cashflow from operating activities for last 4 years : (2015 to 2018): =1346 CR

So 1346*5= 6730 CR

Now in last 4 years fixed assets purchased is 2602 CR , I think this will be reduced as they have done all possible expansion

I think they can safely repay debt of 7950 CR debt in 2025 (even not considering incrimental expansion cashflow )

For going concerns, debt is not repaid but only refinanced. Plus growth should come because of new capex already done and cyclicality of business will bring some bumper years. 2020 will not be a washout either.

the negative is overall profit and sales growth is in negative quadrant …

things will be more clear once concall is organized which will be on 29th of may details below

Limited impact on demand for CPC and CTP during Q1. However, slowdown of global economy may impact the demand for our products and we are prepared to minimize any such negative impacts, especially being a Convertor of by-products into value-added materials.

The management started operating its plants in India, in a phased manner, from first week of April 2020. Meanwhile, the Group’s plants in Europe and North America continued to operate, without any break during the current quarter.

Certain products were adversely affected by the unprecedented fall in crude-oil and related commodity prices resulting in a write down to realizable values at the end of Q1, expect typical lag impact of a quarter to work through the adjustment.

Write down-Inventory Adjustments due to substantial fall in commodity prices of 90 Crores ( note this is an accounting #)

Caution from Mgmt:

Demand from major customers remained strong during Q1, but the same may fall in the coming quarters.

ACP plant construction activities in U.S. and India are on hold due to the COVID-19 impact and expected to commence operations in Q1 2021 to minimise the possibility of coronavirus exposure at existing operations.

Lower Volumes in Advanced Materials and Cement Segment - basically due to the global economy being slugging, no direct impact from Covid on this yet, this might continue for the next couple of quarters (in my interpretation).

In Carbon Segment:

Prices have decreased - shipment timing might have helped increase volumes, the bigger pic is prices are playing spoil sport in this segment too.

Avg. realisationdecreased by 20% approx.

Overall Carbon segment which generates close to 65% of the revenue, is taking a hit.

Have to monitor this segment - might continue for the next couple of quarters. They are trying to control the operating expenditure

Advanced Materials: Revenue is down by 6% approx, realisations up by 1%

Cement: Revenue is down by 12.5% , realisations down by 6.6%

Thank you for posting this Shivam. I was all set on starting an sip with rain but luckily I read this post and now I’m going to stay as far away from it as I can. Seems too risky especially considering the other amazing options available in the market right now. Cheers

I dunno what it is about rain but it just draws me back. Reading the entirety of dr vijay malliks article above made a lot of sense and I decided to exit my position in rain since the fear of debt guided me. And then I went through the latest concall and read that they should be done with debt by 2025. The management is just fantastic and when they say something I believe them. They’ve done so much capex over the past decade that they’ve always walked a very thin line but they’ve almost gotten over it now. Imagine a no debt rain with all its capex ready and firing adding to its topline for cpc and ctp along with a 4MT cement business thrown in for free. And it’s valued at MCAP of 1/6th its current revenue. To be safe il switch from my previous agressive holding to a sip based holding though. Will buy a tracking position now and buy over the next few years based on quarter results and commentary. It’s a very risky play so I’m not going all in just incase all the many factors go against it but the potential is mind boggling post 2025.

The dependance on cycles is what gets me. Right now could well be the start of a cycle … however, I don’t trust myself to know when the cycle is ending. Ideally there’s a 2 to 3 year cycle where rain develops enough profits to pay of its debts. I am investing in sips hoping that’s the case. Worst case scenario the cycle starts and abruptly ends and we get a repeat of 17/18… Rain rises like crazy based on a quarter result or two and then crashes post leading debts to rise and leading to destruction of capital. I like investing long term and this scares me. IF rain does become debt free 2025(and I’d say the odds are in its favor) I’d say this will be one of the biggest success stories in the stock market. An sip based on more information every quarter will still mean I’m part of that story and also help me mitigate the risk. Their debt during Corona is just too high for me right now especially since demand will be lower due to Corona hence endangering the company. In normal times I would have been fully invested.

Makes sense. But also you don’t really have to wait till the peak of the cycle to exit. You rightly said due to Corona & chances of the cycle abruptly ending due to covid situation being new for all of us no one knows which direction it would take. But since there exsists an uncertaintity hence the cheap valuation. Yesterday, I read a quote on what is risk? “It’s a collection of questions and thing that can go wrong. Than what actually goes wrong.”

Yup. Infact what makes even more sense is buying now at low valuations rather then getting trapped at higher levels with an sip. What I liked about rain is even though it crashed from its high levels it still stopped crashing at 3 times it price before the cycle began because its base level revenue was higher than pre cycle revenue. So id say entering now is safer than I make it sound. However, due to the debt I may just wait atleast until the Corona period is over and demand rises again and reassess then.

@jitenp, I have just started studying this business in detail and would like to pick your brain on this one. I can see that you were among the first ones to invest in this business in 2014 and made a good 10x in 2-3 years. Your thesis was pure cyclical play as the co was starting an upcycle. Interestingly I can’t see any post from you since late 2017 which was peak of the share price (assuming u exited right at the top).

What are your views on the current situation? Is the co in last leg of down cycle or there is much more pain still to come?