hey @jhasuraj, i understand this might not be the time to present a write up on this, but understand this was part of our meetup and presenting a company to learn from each other.

Great questions by the way on the worst case scenarios.

Here are my 2 cents on them:

What are the different liabilities (interest payment, debt repayment, capex) which is coming in rain’s way in immediate time (in 1 or 2 year)?

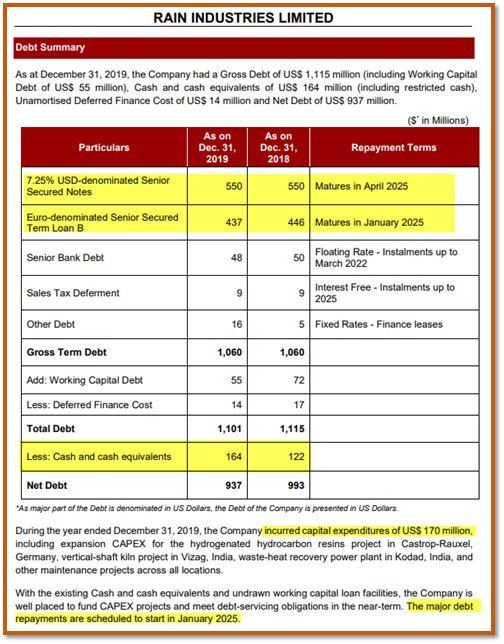

From their presentation: They have no repayments due at least until 25, which gives them 4-5 years’ cushion on principal re-payment back. Also since the central banks in USA (& assume other across the world might follow through) are trying to reduce interest rates, there is a possibility of refinancing at a lower interest rate, if needed.*

• Next year Capex for expansion + maintenance is around $120mm.

• Out of this, their regular maintenance capex is $60mm per year -

$120mm for 2 years. Worst case in two years if they see the Covid situation play out longer, they can stop Capex from an expansion perspective and contribute only to maint. of $120mm for 2 years.

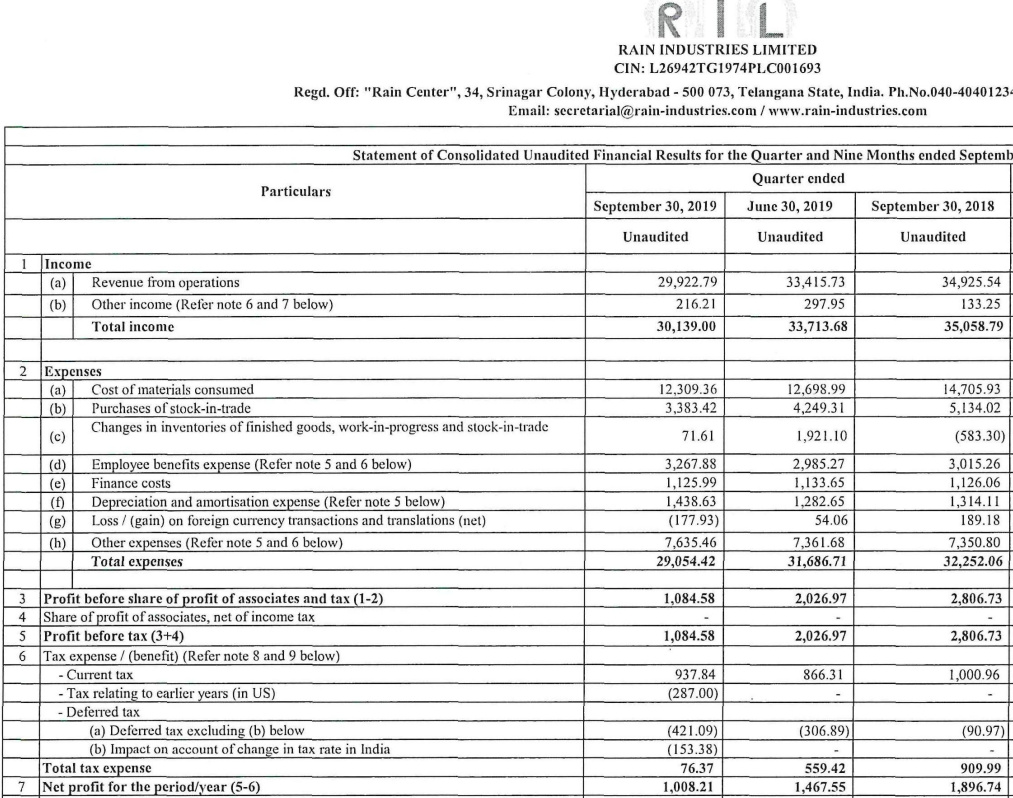

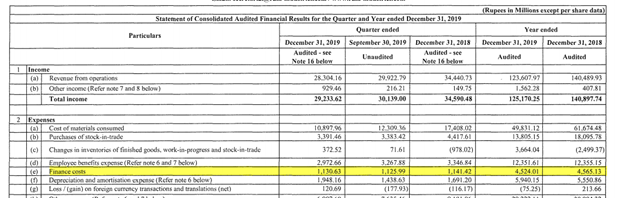

• Finance cost of Rs.452.4 & Rs.456.5 Crores in Cy 19 and 18 respectively. On avg. close Rs.450 Crores is their yearly avg finance cost. Their cash(CCE) on hand is Rs.1095.16 (cover of 2 on annual basis, in the worst case).

What do you think will be impact on sales and margin of rain, if the issue persists for some time (around 1 or 2 quarter)? In that situation, would rain have sufficient to pay its interest? – They should be able to cover with the cash in hand. Margin’s might not be compressed but the volume and revenue might go down. (read page 8 & 9 of the latest conf call transcript for additional insights)

Rain has cash equivalents worth of 1168 Cr and quarterly interest payment seems to be off 113 Cr. So they can keep paying interest for some time. but What about capex plans? Do they have any debt principal payment in next year? I think there might also be working capital cycle elongation, which can take some of the cash away. – I have covered for this on annual basis already above and they have sufficient cover. On WC elongation- yes can impact them but by how much is hard to quantify. If you look at their latest comment on this “Working capital has continued to be a source of cash for us in the year, and until prices stop falling and the new projects become operational, we expect this trend to continue.” Remember this was because of the high cost inventory before this quarter & they almost extinguished all of it.

Sources used: 1) https://www.rain-industries.com/assets/pdf/rainindustrieslimitedpressreleaseonafr31122019_20200228095840.pdf

2) https://www.rain-industries.com/assets/pdf/consolidated-afr-31.12.2019_20200228095710.pdf

3) https://www.rain-industries.com/assets/pdf/rainindustrieslimitedearningscalltranscriptonafr31122019_20200305104502.pdf