Introduction :

Cash logistics solutions include cash-in-transit, cash management services, ATM replenishment & services, money processing, vault outsourcing, transportation of valuables, intelligent safe services, and payment services, among others.

Cash Management, in particular, includes the following services: -

- Currency Management

- Currency Distribution

- Coin Distribution

- Exchange of Notes

- Combating Counterfeiting

The growing security concerns among banks and business organizations, which require secure cash movement and management services, have had a favorable impact on the global market for cash logistics services. The rising demand for cash in emerging economies, as well as the growing number of fully automated cash-in-transit equipment in developing countries, is likely to propel the cash logistics market forward.

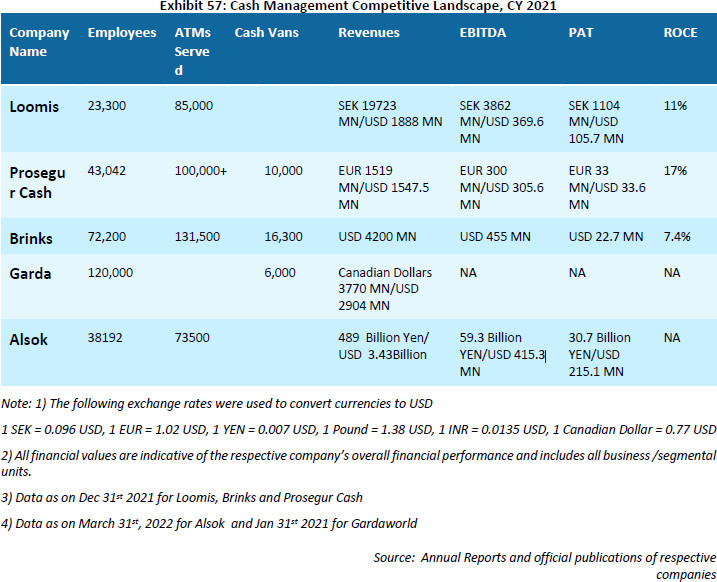

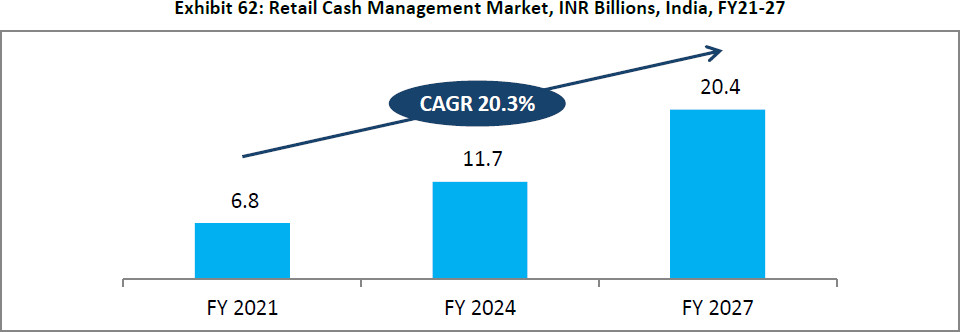

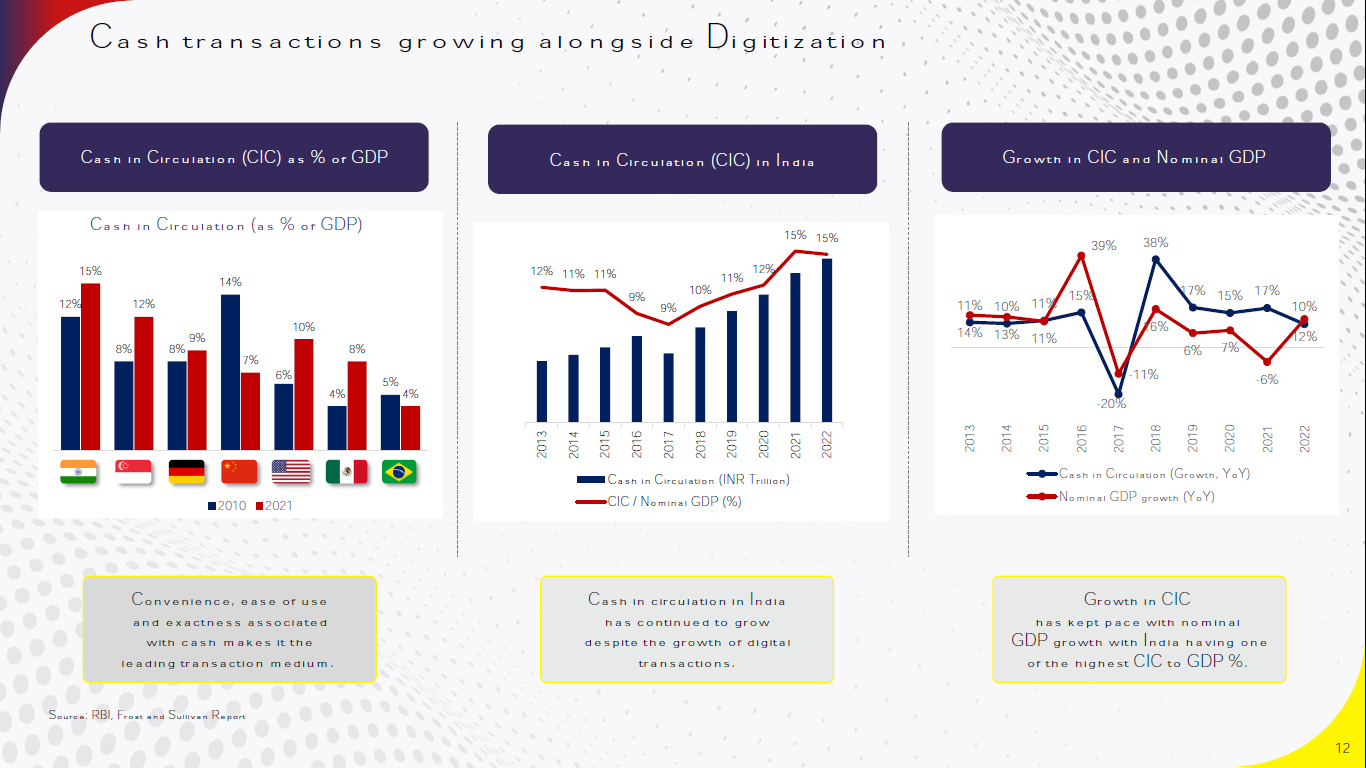

In developed markets such as US and Europe, the degree of outsourcing of cash handling is strong due to the maturity and high awareness with banks and large retailers to reduce their cash management costs and focus on their core business activities. Cash handling is in its early phases in India. Global players have been providing Retail Cash Management services for several decades now – Brinks since 1859, Loomis since 1918, Group 4 since 1960s and Prosegur since 1976. RCM is a relatively new sector in India – market leaders Radiant and CMS have been offering these services only since FY 2005 and FY 2001 respectively. The cash management services market has a tremendous potential to be exploited in areas like retail cash management, as well as other value-added sectors like ATM cash management and automation solutions. The amount of cash in circulation and the number of cash transactions that occur on a daily basis are two significant influencing factors that influence users such as banks and shops to outsource cash operations. Despite the rise of digital transactions in developed countries, cash usage continues to rise, which is more typical of the market scenario in an emerging economy like India.

Competitive Landscape :

In India, the main players are CMS Infosystems, Radiant and SIS. Writer Safeguard (WSG) and a couple of other small pvt limited companies seems potential candidates for consolidation. However, in terms of business model, Radiant is a close match with CMS Infosystems albeit leading CMS in the RCM space.The Cash management subsidiary of SIS (joint venture with Prosegur)is one other player but diversified across ATM cash management and RCM similar to Write Safeguard. Overall, in my opinion, business wise CMS seems a better player diversified through ATM cash management services however the present growth opportunities largely favour Radiant.

Business Overview:

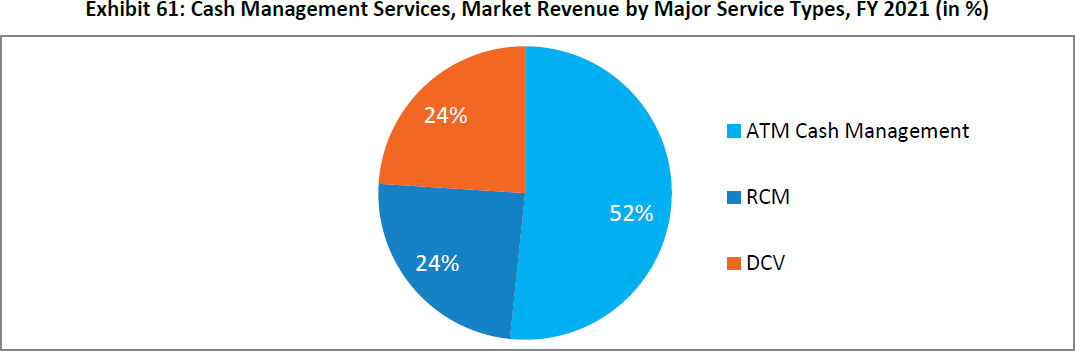

The Indian Cash management market can be split into: ATM cash management, Retail Cash Management (RCM) and Dedicated Cash-in Transit Vans (DCV). Other services include transportation of jewels, art works, valuables, bullion and cash processing and vaulting. BFSI, NBFCs, malls, fashion stores, food and beverage stores, pharmacy chains, and hospitals are all boosting the cash management market in India, especially the RCM business. These industries deal with enormous amounts of cash and need the help of private cash management companies. The Indian cash management market is consolidating, mostly as a result of smaller/unorganized players quitting the market due to stringent compliance requirements and a growing trust among scale players.

Key Business Characteristics:

- B2B - Outsourcing arm of banks and retailers

- Geographical diversification: Pan-India presence currently

- Repeatable business based on pure operational efficiency

- Asset light (buildings, vehicles and computers and accessories on lease basis)

- Potential IP (proprietary software assets)

- Likely duopoly as seen globally

- Entry barrier: Compliance with RBI incl maintaining 1 Billion INR net worth at all times

- Customers: Banks and reasonable sized retailers diversified across sectors/industries

- Long term contracts with annual automatic renewal with some flexibility to re-negotiate prices

Business Portfolio:

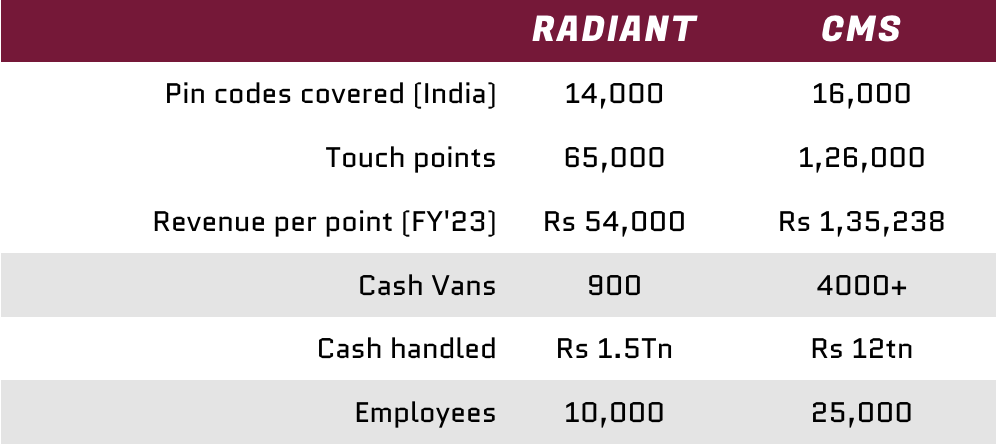

RCM market consists of CMS Infosystems and Radiant as the two key players. While CMS Infosystems has a differentiated offering across the cash management services market (including ATM cash management, RCM and DCV), Radiant has established itself as an integrated cash logistics player with leading presence in retail cash management (RCM) segment

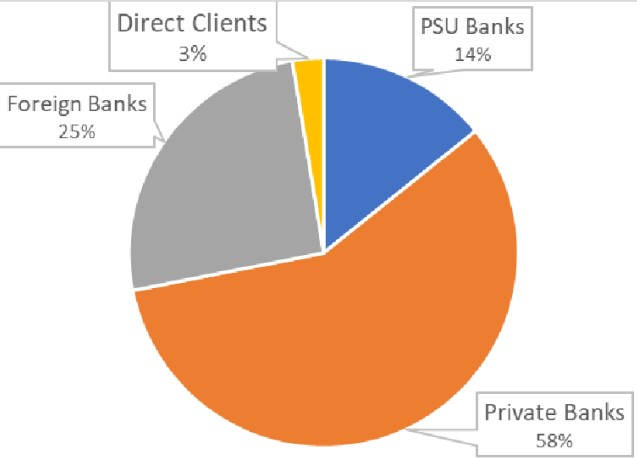

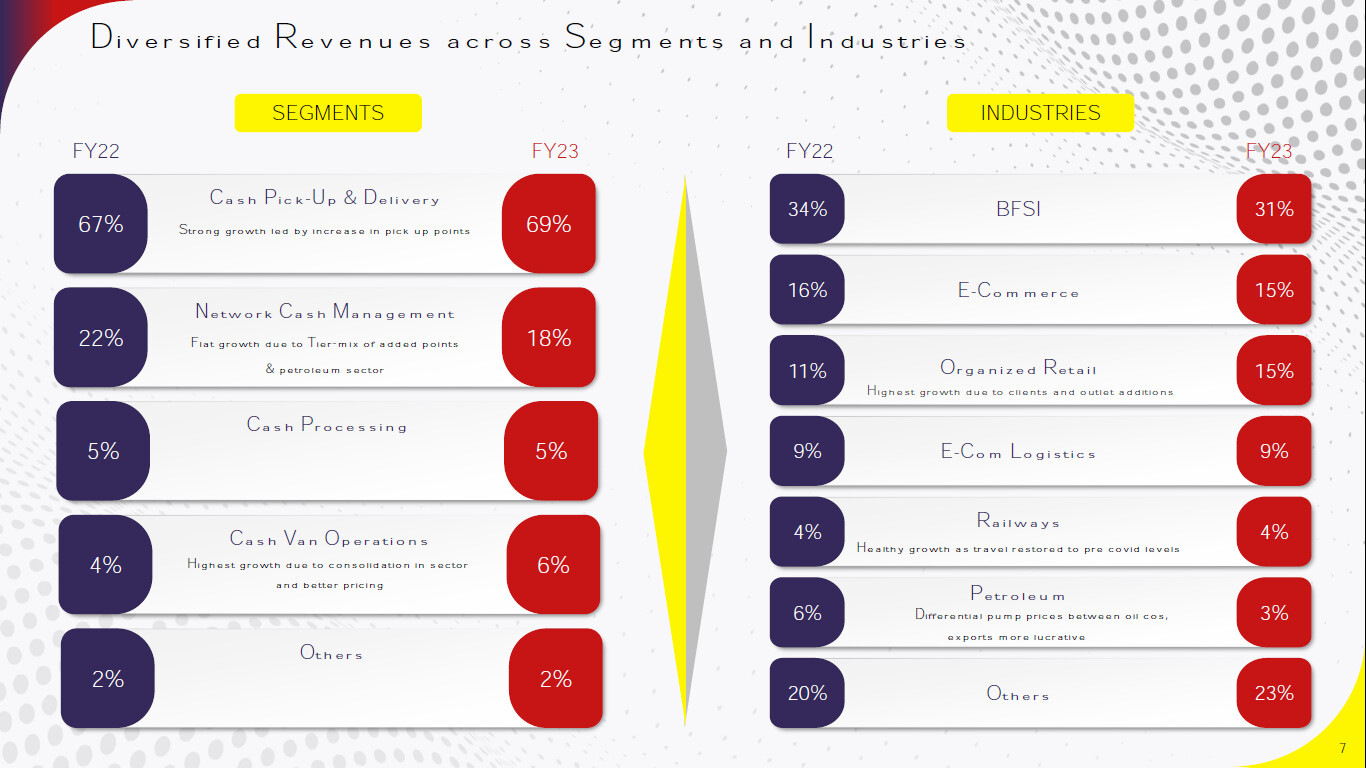

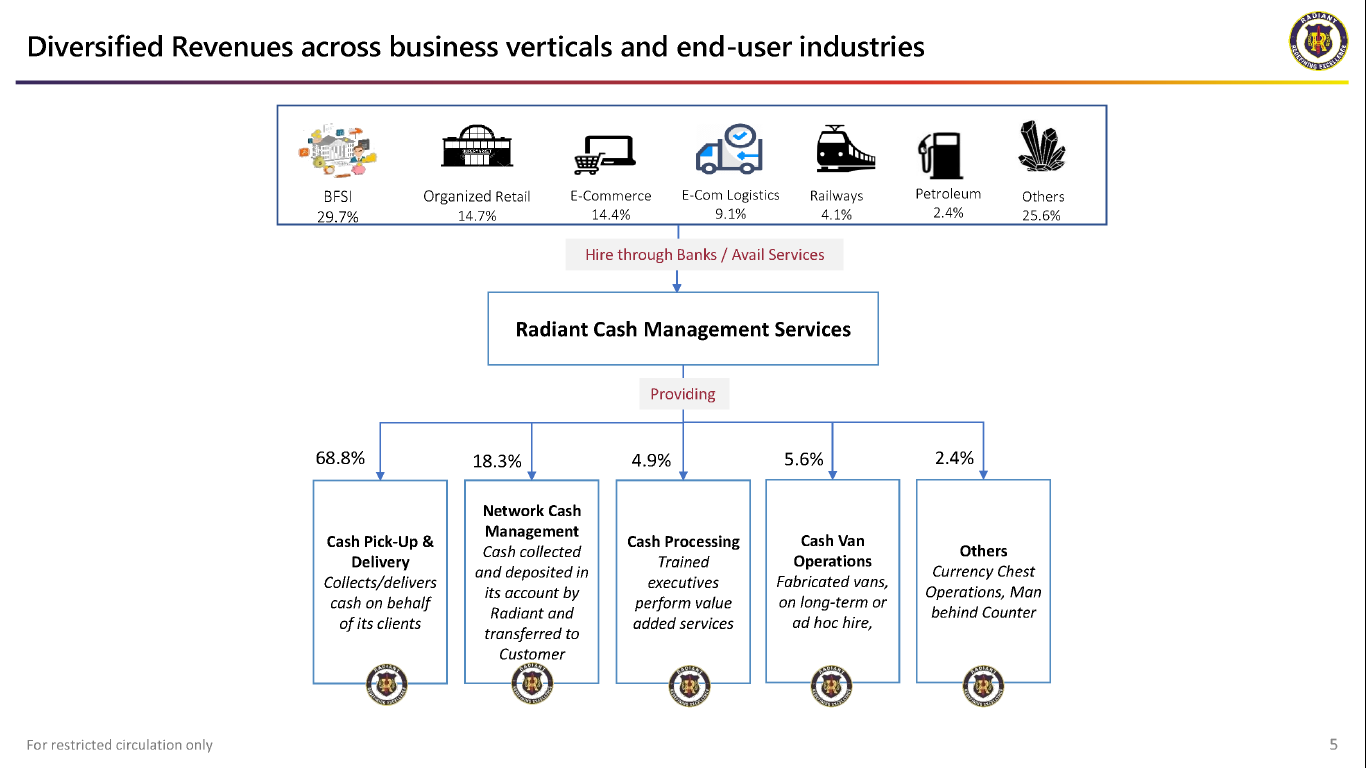

Segmental breakup of Radiant :

Key drivers:

- Growth in currency in circulation (CIC)

- Growth in key retail touch points (organized retail market)

- Growth in bank branches in semi-urban and rural areas

- Efficiencies of outsourcing

- High prevelance of Cash on delivery (COD) across cities, especially tier-2+

- Increasing security requirements

Business Risks:

- Penetration of card infrastructure in retail sector such as POS terminals which can bring down cash transactions

- Rise of digital transactions such as UPI, wallets, cards etc. which can again bring down the cash transactions

- Interest rate risk present although quite negligible

- Credit risk present although quite negligible

- Collection and liquidity risk present though very negligible

- Related party transactions (approx. 20% of sales) is a monitorable

- Loss/theft of cash is present though seems mitigated through insurance coverage and tie ups with senior police officials across the states

- High client concentration - top 10 clients contribute 90% of the revenue in FY22 that is brought down to 81% in FY23. Having said that, there should be customer stickiness unless the company goofs up in a major way.

- Increased competition if company diversifies into ATM cash management as part of its natural evolution although management does not have any such intention today

Corporate Governance:

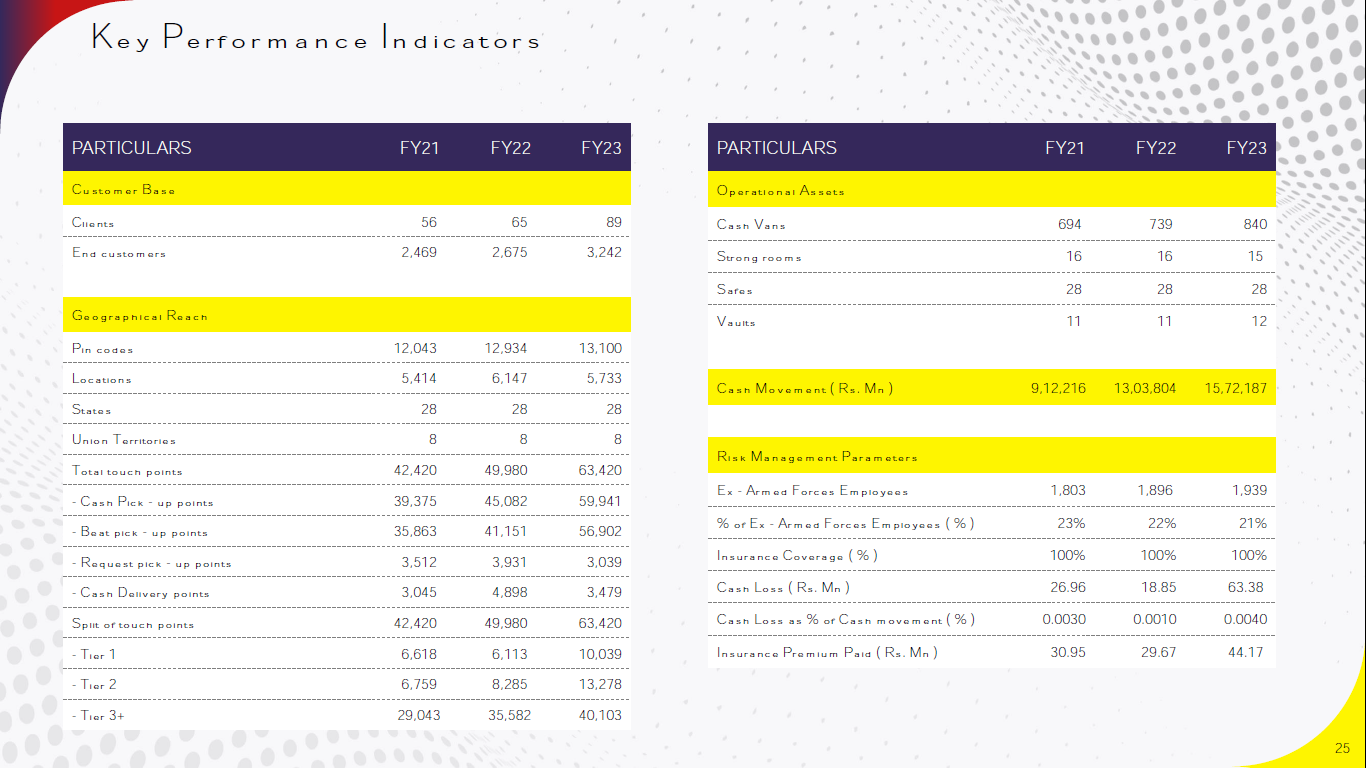

No major red flags so far except that the related party transactions with handful of group companies is a monitorable. Transactions are seen in the form of loans, advances, leasing arrangements, contract charges and equity. The company does not have any subsidiary, associate/joint venture or holding companies. Chairman and MD Col. David Devasahayam and whole time director Dr. Renuka David are related to each other. Their son, Mr. Alexander David seems to be GM (operations), which could be a potential succession plan in the future. The company boasts of the board and management comprising of many ex- defence serviceman and retired IAS persons to bring in the required rigor, discipline and integrity. 21% of the total staff as of FY23 is ex-armed forces. Promoter holding stands at 56.92%.

IPO comments :

The IPO issue was largely an offer for sale from existing shareholder (PE firm: Ascent Capital Advisors India Private Limited) to the tune of 202.6 Cr of the total 256.64 Cr with fresh issue of 54 Cr towards funding WC requirements, CAPEX for purchase of specially fabricated armoured vans solely as an operational risk mitigation measure and general corporate purposes. From the concalls, the management seems shareholder friendly. The company aspires to maintain itself as a strong dividend paying company with good focus on ROCE and ROE. The dividend payout ratio for FY23 being 51%. This also indicates that the management is in no hurry to make hasty acquisitions in adjacenies and sees enough growth potential in existing lines of business, allowing it to retain/better it’s marketshare.

Marquee clients :

Leading banks of the likes of ICICI Bank, HDFC bank, Kotak, SBI, Axis, Bajaj Finance, Deutsche bank, Standard chartered etc.

Financials and Valuation:

- Market Cap: 990 Cr

- Div yield: 1.08%

- D/E: 0.01 (largely short term working capital loans)

- 30 plus ROCE and ROE with 20 plus ROA (Asset turnover of 1.51)

- 5 year PAT CAGR: 66%

- OPM maintained at around 24-28% in the last 5 years

- Cumm CFO/PAT last 5 years: 1.09

- Free cash flow seen with adequate cash in balance sheet

- At 92.8 CMP (lower than IPO price band) available at a PE of 15.79 and a PEG of 0.25 with 4.31 PB

FIIs of the likes of Societe Generale and MOSL (Motilal Oswal) have taken a stake in the firm recently.

References:

Screener, Frost and Sullivan Assesment of Cash Logisitics Market in India, DRHP, Annual Reports, Investor Presentation and concall transcripts

P.S. This is not to be construed as buy/sell recommendation. Please do your own due deligence.

https://radiantcashservices.com/group-companies/

Industry-Report_Nov-2022.pdf (1.1 MB)

Annual-Report-2020-21-1.pdf (4.2 MB)

Annual-Report-2019-20-1.pdf (4.9 MB)

q4 fy23.pdf (2.3 MB)

q3 fy23.pdf (1.8 MB)

q4 fy23.pdf (688.0 KB)