Radiant Cash Management Services Limited – A Business analysis, 6th Feb 2024

Background

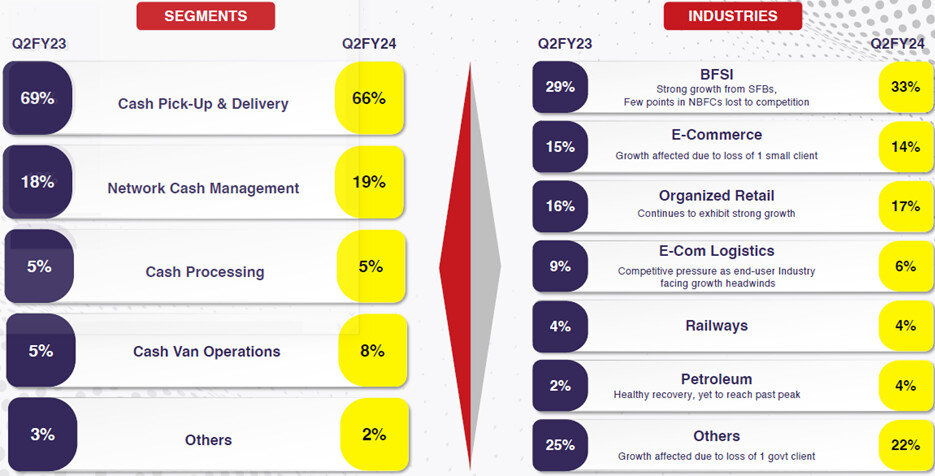

Radiant Cash Management Services, started in 2005, is in the simple business of retail cash management (RCM). It provides cash logistics and related services as described below (Figure 1):

Cash Pick-Up and Delivery: Transportation of cash to and from retail or other private entities on a daily basis or upon request and deposit it in banks. Typically, banks hire Radiant and offer these services to the end customers, e.g., retailers. About 4.1% of all revenue is from direct customers, the rest originates from banks (concall, Q1 2024, Aug 2023).

Network Cash Management (Cash Burial): If a bank does not have a branch in an area, then cash is deposited in Radiant’s account and electronically transferred to the bank.

Cash Processing: Upon end-user request, cash is counted and verified at the time of pick-up (as against sealed bag pick-up) for an additional fee.

Cash Van Operations: Provide armored vans with full crew comprising driver, armed guards, cash custodian on short- or long-term lease mostly to banks for their own bulk handling of cash (between branches and vaults)

Figure 1: Business segments of Radiant and the industries it serves, by percentage revenue (Investor presentation Q2, 2024; Nov 2023).

The major clients are BFSI, e-commerce, organized retail, e-commerce logistics, railways and petroleum companies (petrol stations).

Business drivers

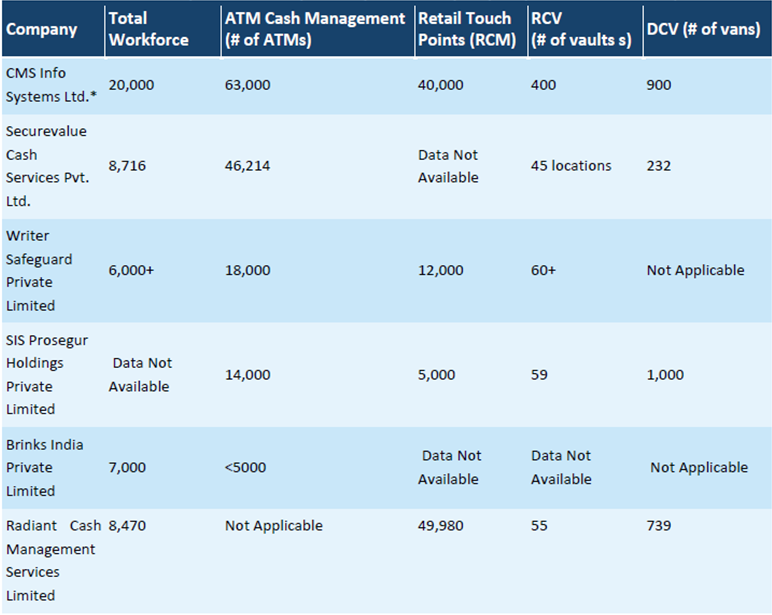

RCM is a relatively new sector in India – market leaders Radiant and CMS have been offering these services only since 2005 and 2001 respectively. Cash management industry rivalry is typically limited to two or three market participants globally, especially in developed markets. As shown in Figure 2, CMS and Radiant are the only two large players in the RCM space in India. In fact, these are the only two pan-Indian players.

Figure 2: Competitive landscape of RCM players in India (ASSESSMENT OF CASH LOGISTICS MARKET IN INDIA, Frost and Sullivan, 2022).

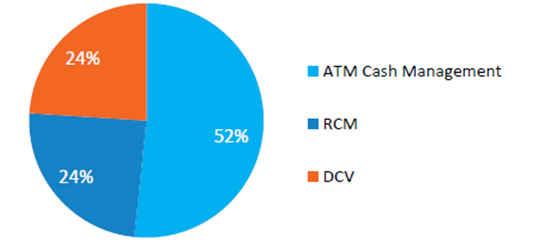

As measured y total market revenue in India, RCM and direct cash vans each constitute about 24% of revenue (Figure 3). These are the two areas where Radiant is active and has chosen not to a player in ATM cash management due to excessive competition. Further, as shown in Figure 1, for Radiant, DCV (=cash van operations) is not a major revenue source.

Figure 3: ATM cash management, retail cash management and dedicated cash vans, by revenue (ASSESSMENT OF CASH LOGISTICS MARKET IN INDIA, Frost and Sullivan, 2022).

Superficially, Radiant seems like a no-moat business. However, due to RBI regulations (link here), that requires players to have at least INR 1 billion in net worth at all times and a minimum of 300 armored vans, ensures that its hard for upstarts to break into the market. This, of course, does not stop pricing pressure and competition from existing players but that’s where a duopoly helps.

When it comes to the long-term prospects of the business, there are two opposing forces at play. The first is the possibility of reduced cash transactions owing to increasing digital payments. The second is increasing formalization of the Indian economy and thereby more customers interested in availing RCM services.

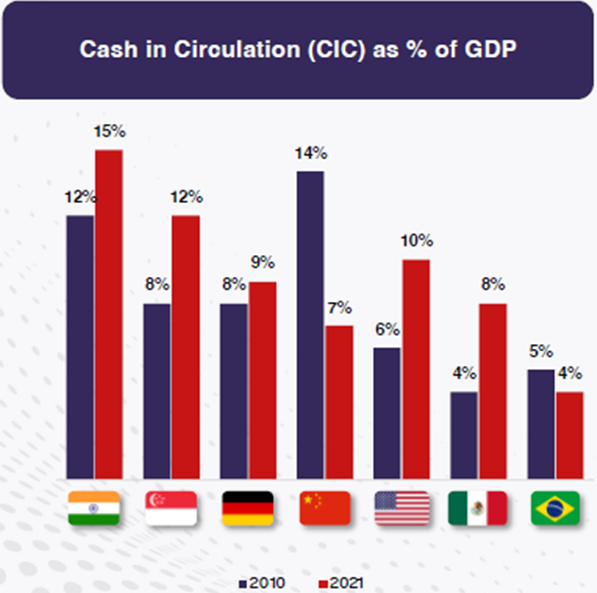

As shown in Figure 4, for most countries, including developed ones, cash in circulation as percentage of GDP does not decline. If one adjusts for the fact that the GDP itself is growing, then there is a twin-engine effect. 10 years down the line, will India buck the trend? Perhaps, but I don’t think so.

Figure 4: Cash in circulation as percentage of GDP in 2010 versus 2021 (Investor presentation Q2, 2024; Nov 2023).

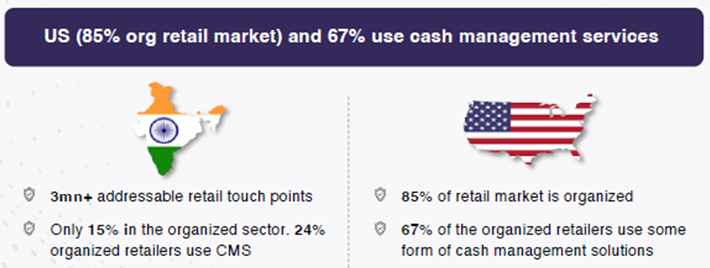

In India, RCM remains relatively nascent, owing largely to the fact that the organized sector is relatively small. As this sector grows and companies within it scale (think DMart), RCM is a natural choice. Figure 5 shows that, as opposed to the USA, where 85% of retail is organized, the corresponding percentage in India is only 15%. There are long term tailwinds for the RCM business to grow.

Figure 5: Organized retail in India versus USA, including percentage of organized retail availing RCM (Investor presentation Q2, 2024; Nov 2023).

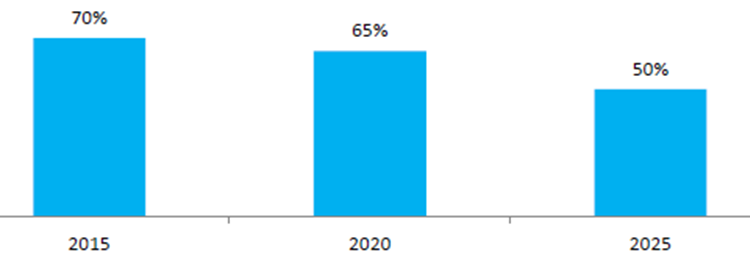

Even in e-commerce, cash-on-delivery (COD) is high. In 2022, 60% of all e-commerce was COD (Frost and Sullivan, 2022). As we travel from metros (50 percent COD) to lower tiers such as tier 2 (70 percent COD) and tier 4 regions (90 percent COD), the percentage of COD increases. While the percentage of COD overall, is reducing (Figure 6), the trend of increasing e-commerce in tier 2 and below will ensure that COD still has a long runway, at least a decade.

Figure 6: Cash on delivery in ecommerce transactions in India (ASSESSMENT OF CASH LOGISTICS MARKET IN INDIA, Frost and Sullivan, 2022).

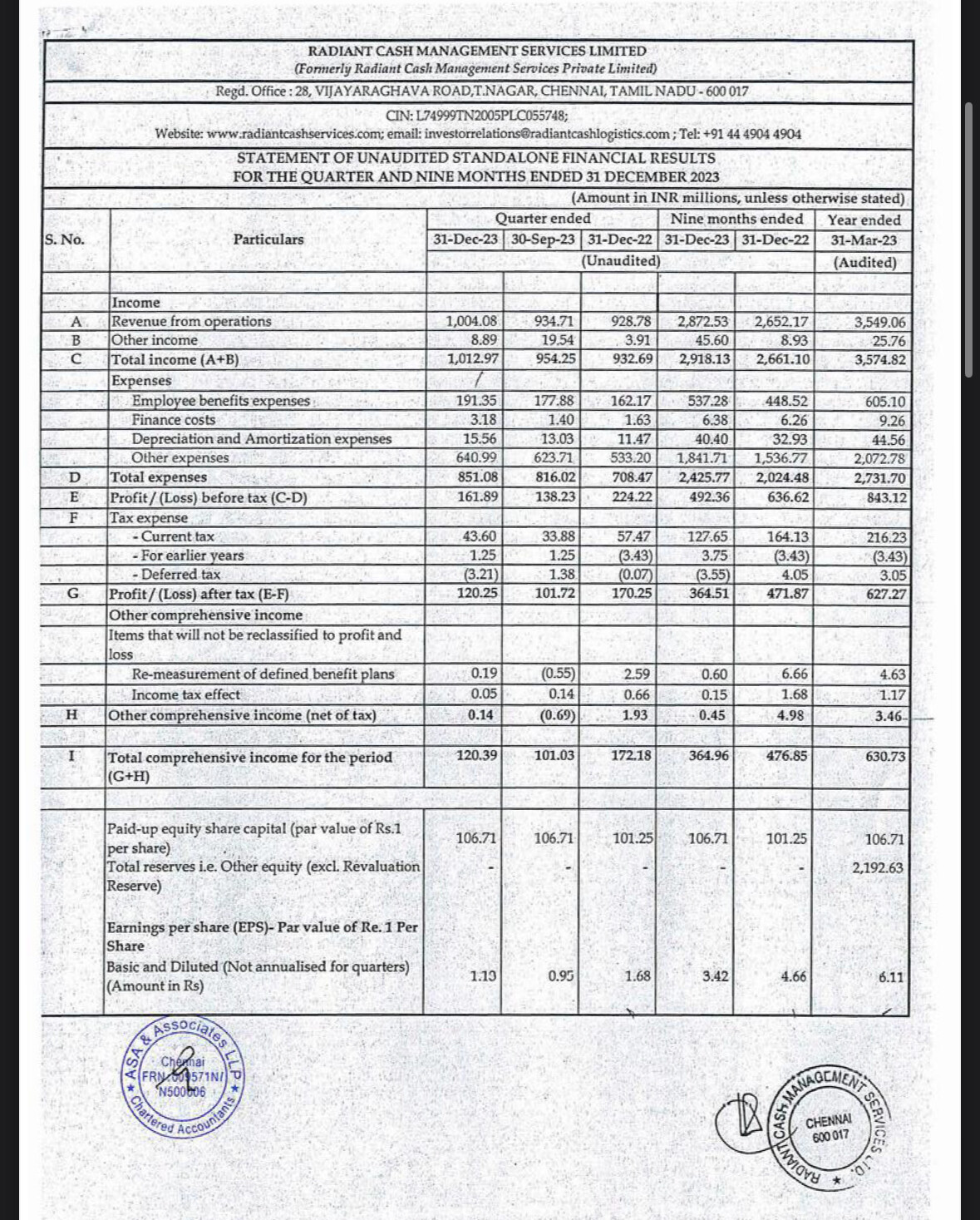

Analysis of Financial Statements

Radiant went public in Dec 2022 which is worth keeping in mind when analyzing Table 1. Cash from operations were negative in 2019-20, because a lot of the working capital (cash on the balance sheet) was used to pay down liabilities. This throws off all the 5-year averages that relate to cash from operations and FCF.

What’s worth noting though is that EPS and revenue per share are growing at a good clip, equity growth rate is high and that the company has no debt (Enterprise value < Market cap). Further, if you look at FCF in 2023, its 19.2%, a third of which is paid out as dividends. Maintenance capex is pretty low which is not unexpected for such a business – the largest depreciating asset is vans. This would leave plenty of cash for the company to consider organic growth and acquisitions.

Table 1: Key metrics from financial statements in millions INR over the past five years.

Table 2 shows a valuation attempt using EPS and a payout ratio of 50% to get close to the dividend paid in 2022-23 (INR 3). I assume modest growth rates for normal, best case and worst-case scenarios and relatively low terminal valuations with which I get a11% compounded return. I do think that the best-case scenario is most likely as the company has quite some room to keep growing even after 10 years – this would give about 17% compounded return.

Table 2: A DCF valuation for normal, best case and worst-case scenarios using EPS as input.

Investment thesis

In terms of risk, I don’t see too much downside – theft would be a risk, but they are insured against that. INR 23 out of the stock price of about INR 93 is the book value (all cash), that means you are paying INR 70 for growing future cash flows. There can be some volatility as it’s a tiny company ($120 million), but then again, it could go up 50% very quickly too. 10 years down the line, the company will still exist, will likely do a lot more business and is unlikely to get disrupted too much, even with digitalization. In summary, a boring company that does its thing and produces cash consistently. See if it fits you.

Company news

August 2023, foray into diamond, bullion and jewelry (DBJ) transportation: Radiant has made the decision to also provide services for transportation of DBJ – this seems like a good step as it employs exactly the same resources as in the RCM business, i.e., armored vans. Plus, they already service about 1000 jewelers for RCM, so plenty of synergies that may play out. According to the concall of Nov 2023, the projected revenue mix of the DBJ business in 2025 is 20%. Assuming the rest of the business grows from about INR 3700 million to about INR 4500 million by 2025, the DBJ business would be about INR 900 million. Maybe they get there, maybe not, but I don’t see much risk. If the DBJ business does not grow as quickly as expected, the vans and personnel can just be used for RCM. Radiant is adding 200 more vans to support this business. Heads I win, tails I don’t lose too much kind of situation.

Dec 2023, acquisition of Acemoney: Radiant paid INR 112 million to acquire a 57% stake in Acemoney of which 92 million went into the company. Acemoney is a fintech that provides digital banking solutions designed specifically for retail outlets, and cooperative banks societies in rural areas. Cooperative banks typically don’t have digital solutions and Acemoney can provide one for a fixed start up cost and then some amount of recurring revenue. This model has had success in Kerela, Tamil Nadu and now they want to spread to other states. When it comes to physical services such as micro-ATMs or QR code based physical assets, Radiant’s pan-Indian footprint helps as it can act as a distributor for this fintech in Tier 3 locations and below (which is where Radiant is strong) while other fintechs need to spend considerable resources to distribute such physical assets.

The CEO mentioned, they are targeting to deploy 100,000 micro-ATMs in the next 2 years (with RBI subsidy). At INR 850 revenue per micro-ATM/month, the monthly revenue is about 85 million – I suppose only 57% of that revenue belongs to Radiant which would be INR 580 million annually. Even with 5% net margins on this micro-ATM experiment, they will recover their purchase price in a few years. Again, not quite sure how this acquisition will pan out, but it’s a good bet because it’s a cheap one. Not much downside.

Catalyst

A boring, steady business which might get some extra earnings power if the new organic and inorganic experiments get executed well.