Recording of Investor Call held on 20.08.2021 with White Oak Capital Management

11 Likes

Making available one to one concal details to all investors is a very good initiative from Company and I firmly believe that all Company should do the same as part of good corporate governance.

9 Likes

@Raj_A_A

If you listen to investor call uploaded today. 46% share comes from 2 wheelers. Around 20 % from agriculture vehicles. And rest seems to be from 3 wheelers and 4 wheelers.

Impact seems to be low I guess.

2 Likes

Highlights from the call. My notes in brackets with a bit of bias, of course, due to the fact that I am invested.

On EV risk

- Already working on an EV project - Going into mass production in 2 months. 3-4% of FY23 revenue could be from EV.

- Ahead in terms of technology, compared to other Indian players, but not necessarily ahead, compared to European players.

- EV is being discussed in India whereas what is being discussed in Europe & US is hybrid vehicles.

- A thrill seeking mountaineer will not take a high end EV bike to a mountain due to a lack of charging stations in remote areas.

Growth opportunities

- Some growth will come from new customers added recently

- Tremendous growth opportunities in the business. Limiting factor is that gear manufacturing is a highly capital intensive industry. Can’t grow inorganically.

- Add a new big customer every 2-3 years. Develop a customer - Build a relationship over time - Develop technology for them - Then comes the boost in sales from the customer.

Competition / Competitive advantage

- Global competitors are based in Taiwan, Japan, China, Europe. Have a competitive edge because they are based in India.

- An American or a European buyer is looking for quality that they can get in Europe or the US. They are looking for deliveries as per Japanese just-in-time standards.

- Europeans & Americans feel IP rights are respected more in India than in China. Probably the only Indian supplier to export gears to China.

- Japanese players have very good quality & delivery but they are very slow in developing products.

- Opened a subsidiary in Austria & deployed engineers there. If a customer calls in reporting an issue, our engineer is there the next morning. (Easy availability is always an add-on)

- Core technical team has been with them for 2-3 decades. Technical capability doesn’t come overnight. It comes with sustained effort. This has happened because we nurture our people. We give them a positive work environment. We create a kind of a family culture. And this leads to technical capabilities.

(Corporate culture as a moat? Probably hard & time consuming for somebody else to replicate) - Prabh (promoter) spends 50% of his time towards human resource development.

Pricing power

- Raw material increases are sometimes passed on. Sometimes not. Depends on the contract.

On risk taking

- Don’t buy big machinery for a specific customer in order to de-risk themselves. Some part of the big machinery investment is also contributed by customers. Very careful in what to invest and where to invest.

Revenue & margin guidance

- 500 Crs revenue guidance is a safe target and they are on track.

- Confident about margins barring external factors.

31 Likes

I have read your twitter blog on RACL which was comprehensive and well covered all aspects… Their target of 500 cr by 2025 is achievable given their past achievements. But in the short term, there are two hurdles …one is commodity inflation which jacks up the COG and second big one is this chip shortage. Their Niche segment of high end bykes will definitely have semiconductors in their control modules and to that extent the end product production might be affected . Consequently , OEM suppliers will also be correspondingly affected. Which, IMHO, will affect their performance in the next few qtrs. I would request you to throw light on this aspect as you have well researched this company and would like to know your views on this. Thank you.

Disc: Invested

4 Likes

WhiteOak concall- interesting take aways( like the recording aspect, haven’t seen many practicing it)

-

Quality of Questions didn’t seem out of box - mostly standard but they intrigued management enough to give responses with a detailed flavor including rational and strategy.

-

Growth strategy - key call out was Step Approach, I.e. 3-4 year single digit growth and followed by a bump up of 1-2 years and so on. This bump up is based on their strategy to add, incubate and scale One New sizable customer every few years. Data seems to corroborate.

-

Above strategy helped them grow, but didn’t get them valuations till FY19 beyond single PE - likely because low OPM and cyclicality perception ( at least appeared so)

-

One key difference that has happened in FY20 & FY21 is on margin front - reaching to 25% from mid teen - biggest factor is export mix increasing and cost front/outsourced capital intensive jobs as explained in their Q4 call.

-

Another aspect that stands out is decoupling from industry cyclical nature - Last 3 years has been good gor them both top line( Step Approach ways), and OPM bump up and sustainability - all of these captured well by solid contributions by VP community

in thread above - much before larger investors tend to notice. -

Right before Corona - Q2 20, Q3 20 is when they reported improving OPM 19% and 22 % and since then OPM stayed above it barring lockdown quarter - huge market volume around these times right before Corona hit and stock prices touching all time high of around 130. Interesting enough that promoter Gursharan holding went up from 31 to 36.44% slightly prior to this performance coming out ( Q3 19 to Q2 20. power of insider buying info - nothing wrong here )

-

USP/ Differentiation of RACL Approach for competetion - competetion exists in China, Japan, Thailand and EU etc in all sizes - RACL takes competetion specific approach - e.g. Japan is too slow in prod dev(4+ yrs), China has quality challenges/perception, EU is not cost effective any more - India and RACL at advantages

-

While most of their current biz ( performance and premium bike/off road/large tractors etc) do not have any disruption due to EV in next 5-10 yrs, to build & prove a capability they are ready with EV parts and They are supplying EV parts to largest auto maker( VW/Toyota per whiteoak folks??) and announcement to follow in next 2-3 months ( in past they were suppliers to before time EV maker in India - Mahindra E2O.)

-

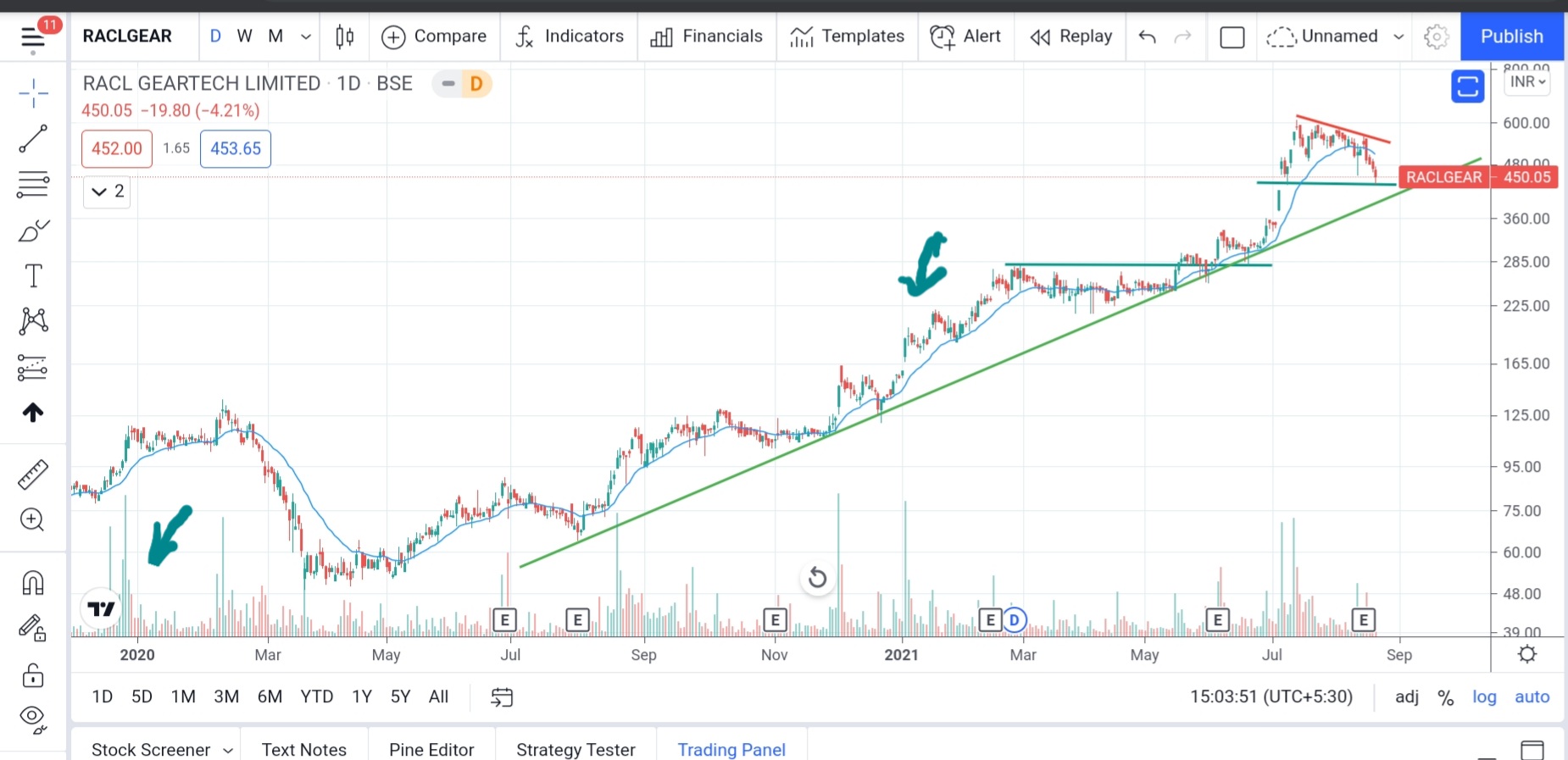

TTM 18PE, 25% margins, double revenue by FY25, valuations seems fair with recent correction healthy - stock seem to be taking support at key level of 440, need to watch out for bounce back strengths and volumes. EV success and any institutional buying will further trigger upside. Near trend line support.

Disc - Tracking position recently and intent to add more, interesting promoters and data quality & transparency for research - esp for their size of company

28 Likes

They’ve been quite candid about the fact that they don’t always win pricing wars with their clients. On the other hand they’ve also claimed that as long as their products meet customers’ need, customers are happy to pay them.

Overall, it would be hard to time this over a few quarters and the focus needs to be on whether or not they are on track to meet their targeted 25% top line CAGR between 2021 & 2025 (From 200 Crs in 2021 to 500 Crs in 2025).

If they manage to deliver consistent growth, the market could potentially give more lavish valuations to the stock just like it has given to Minda and some other auto ancillary players.

9 Likes

Wonderful summary from Baratmukhi. i had made some notes, @admins Please feel free to delete this if you find no value, these notes are like Q&A as the way concall happened

Note: This is not a verbatim

Summary

RACL Management insisted the calls get recorded, which is a wonderful gesture and also it is required as per SEBI rule, RACL want to ensure that this discussion should reach wider audience group

Analyst: Want to know the journey of RACL and their vision for 5-10 years, Market share , Margins , risk mitigation, wants to know from business perspective and less on financials

RACL Management: 60-65 exports and 35% domestic, then PSingh explains the journey of RACL and its ups and downs ( i am not detailing them here )

Some technical stuffs “Reduction gears is different for 2,3 and 4 wheeler, any EV which is 2 ,3 and 4 wheeler should have a reduction gear, even in EV the motors should runt the tire, the torque and power is different for 2.3 and 4 wheelers)

Analyst: Do we have capabilities for RG for the likes of Tesla and VWagon

RACL Management: we have adopted the technology , we didn’t chase the heros and TVS , bcos they want take a different view on sourcing/technology and it is too competitive , We created the tech Reduction Gear technology 10-15 years back for REVA

Between EV and non EV the diff is precision class, we are looking at premium customers, we have created trust and partnership and the client will stick to us.

Analyst: are we working with client in EV space or is it just POC?

RACL Management: we are working with client whose details will be out in next 3- months and the whole world will know , cant specify which country the client belongs to, they are big player and has presence in Europe, USA, China, Japan and in India too (most likely could be Toyota or VW)

Analyst: Share of biz in terms of application

RACL Management: 40-45 % 2 wheelers niche, high end bikes of 600+ cc, We dont do just gears but also suspension, Break and handle parts. 20% goes to agri mainly exports, not limited to trac but could be Land Mowers. New segment Recreational vehicles like snow scooters, snowmobile which is 13% of revenue and rest export customers , remaining in high commercial vehicle for companies like GE and Shnider

Analyst: Can you give a break of parts wise(volume)

RACL Management: cant give breakup to the digit as it is a competitive advantage, We do 600 different parts every month ,volumes 5-6 million and giving product breakup is also difficult as we track it at customer level

Analyst: In EV space In tems of total addressable opp for our segment , how large is the opportunity and what is potential disruption

RACL Management: Regards disruption 47% 2 wheelers its a premium segment , customer are not price sensitive, Agri business will not adopt EV yet charging tractor is not feasible , 3 wheelers reduced from 20% to 3% in last 3 years, We are entering 4 wheelers which are exports customers

opportunity for growth is tremendous as more outsourcing is the way forward, gear manfg is highly capital intensive, Hybrid is what europe is looking forward. demand for parts is high for hybrid.

limiting factors is that the inorganic growth is limited

Analyst: who are the global competitors

RACL Management: Cant guess, they could be from Taiwan, Japan ,China and Europe at all levels , they could be big OEMs are could be mid sized, India has competitive edge due to low cost and labor competitiveness , when it comes to JIT sourcing , IP rights are respected in India , but not the case in China, Japan is slow , there are many players in India, I cant avoid competition , we are looking at creating partnership hence we have opened subsidiary in Austria and have an Engg team there , for quick turnaround.

Analyst: What is our technical capabilities , USP?

RACL Management: Tech Capabilities comes from People, and our employees are working with us from 2-3 decades , Next Gen Employees are entering our company and we are nurturing the new breads

Analyst: Visibility for 500 cr revenue by 2025

RACL Management: Everyone grows 6-8 % on an average, We are adding new customer every 2-3 years, will take 1-2 years for the partnership to become meaningful , when we add new customers we are adding new investments, and it will take 1-2 years for the investment to reap benefits. we don’t invest in special equipment’s and will work with General machines, sometime customers purchase special machines for us.

We have a defined roadmap for achieving 500 Crs, we need to grow by 15-20% growth every year, which is not difficult given our history

Analyst: Have the margins peaked , is there a scope for improvements

RACL Management: Cant give a guidance ,but we are doing best

Analyst: is 15% achievable

RACL Management: lets wait for qrtely results, Q1 was normal business no prototyping in Q1

Analyst: Cash conversion cycle has gone up, Working capital cycles has gone up, from 70-80 days to 110 days

RACL Management: Exports have grown and hence the Cash cycle but we have built that in price.

Analyst: Impact of RM and Currency price increase

RACL Management: we have indexation mechanism on RM and currency and sometimes one offsets the other, client wants us to be profitable but quality should not be compromised

Analyst: Has China +1 one helped us

RACL Management: Cant give political statement, as we are exporting to china too

24 Likes

Earlier BMW had raised concerns about the possible impact on the vehicle production during the second half of this FY due to chip shortages.

However, “More chips are required for higher model vehicles. For instance, semiconductors are key components used in car infotainment systems, touchscreens, power windows, music systems and even remote key modules.”

Some of the options that have a higher demand than supply are the Harmon/Kardon Premium Sound System, Wireless Charging, Parking Assistance Package and Digital Keys. There are, of course, other supply shortages also, like 2-axle air suspensions on the X5 and X6 and ventilated seats, just to name a few. BMW, like other automakers as well, have adapted to the chip shortage by dropping some features from their models. In some cases, they are replaced by similar options which could increase the base price.

But not all models are affected. For now, some variants of the M Performance Automobiles division are spared by this shortage. So it’s always best to check with your local dealer for the most up-to-date information on existing or future orders.

It seems that the chip shortages will largely impact the high end four wheeler models, and less likely impact the superbikes manufacturing as the parts which needs more chips and facing supply woes are typically not there in bikes. Same can be considered for tractors as well.

Not sure how long this semiconductor crisis will continue, but this should be treated as a short term bilp (if at all) in the overall big picure of the exciting future growth that the company envisages.

Discl: Invested from lower levels and this is not any buy/sell recommendation.

11 Likes

Can anyone help with the link of the audio. unable to locate on the website

Concall notice for 3rd Sept (Jun end results). You will need to pre register by 31st Aug to get an invite.

11 Likes

Q1FY22 concall highlights :

Challenges in terms of margins due to global players?

Global players will not work on lower margins.

Competition is always opportunity and never a threat. It keeps u on your toes.

We are competing against best in class.

Debt to equity?

They are very healthy. We are less than industry norms.

Our finance cost has been reducing. We are borrowing judiciously. We have got good interest rates.

Ours is capital intensive business. As a company, future growth can it be funded through internal accruals?

The capital expenditure always has been with borrowing. Leverage is not a bad word. If we are borrowing, means we have confidence in repaying back usually.

We 1st get customers, then do capital investment (except for brief gestation period).

Asset turn ideal should be 2 for us minimum.

Fungibility of capex for ICE and EV customers?

Gears of ICE and EV look similar, but precision is more in case of EV.

All our new investments are happening on EV ready OEMS.

We are not present in low end bikes and cars. Our utility for capex will sustain for 10-15 years, our customers are less susceptible to EV.

EV customer Scooter capacity added?

Our capex can be used for ICE

Our free cash flow has been on weaker side because we are doing capex. WC is on higher side.

For manufacturing, why keep free cash, invest in capex. Keeping money in banks not healthy for shareholders.

At some stage, need to invest keeps reducing. Today Asset turn is 1.4x, in future, it will move up. % of capex at some stage will go down.

Since we are making mechanical components. Our inputs are not chips. For our OEMs, they are big brands and they have good forecast systems and hence we are not impacted much.

Mass customers will give us opportunity, then why not we would manufacture provided if it gives us long term business continuance.

We are always hungry for new customers. When I work for BMW, KTM, for us there is not attraction for brand, we need good stable business even if it is Tesla.

What is our arrangement with clients in case of Recall ? And in past what what has been the error rate if we can quantify?

No recall ever. If any recall, we are hedged with appropriate insurance policy. Some customer allow 100 in 1 million. We did 25 for 8 years.

Samples from new facility, are in advanced stage and validation is in process.

We will always stick to core competence and move only in allied parts which require critical machining. Since we have capital intensive, we have to grow in systematic way.

We are 30 year old organization, we have to take care of obsolesce of our equipment, hence we have to do maintenance capex also.

EV gears, high value but produce less. As long as tradeoff is better, what is the harm.

Capacity in terms of SKUs : We do around 5-7 million parts a year (all products, SKUs).

500 crores target. Nothing drastically change on customer profile.

% of vehicle cost our proportion is very less.

How easy is it to penetrate supply in new brands?

Getting business is tough, since there are gestation periods, sometimes geographical border clients have, can Indians do?. Clients want a strong player for entire project life (at-least 10-15 years), size of team, strength of team. We get lot of business word of mouth and since we have big brands and they refer us.

European customers are also focussed on environment, EE care, beyond our quality. They want to work with responsible company.

Customers are demanding too much and hence we have to fully ready. Once u are ready, customer will come to you. You give whatever he wants.

Advance for machine procurement in Annual report.

Lead times of machine are 6-8 months, we will get machines in this year. Capex this year will also be 50 crores (backed on new customer wins and existing customer demand)

Others please add, if I have missed any point.

Thanks.

21 Likes

Competition

Getting a new client is tough. There’s a gestation period involved.

Country specific hesitation. Question in a potential customer’s mind - Can an Indian co make quality gears?

Word of mouth from other key customers has worked well (This bodes well for RACL’s future)

European customers are particular about environment & employee relations.

Scalability

Will grow in a planned & systematic way

Sometimes rush to grow takes a co. backward

At some point we may say 500-1000 Crs top line in 3 years (This was more of a hypothetical comment, but you never know)

Debt

First get customers > Then borrow & do capex

Finance cost is always reducing as a %

Borrowing judiciously - Getting better rates from banks

Debt to Equity is healthy

Interest cost down from 10-10.5% to 6.9%

Asset turns

Asset turns have potential to go from 1.4x to 2x

2x is a benchmark

Potential to increase asset turns/better operating leverage with scale

EV

Can ICE capacities can be used for EV as well?

All new equipment is EV compatible

Others

Nil/minimal impact due to chip shortage

Open to acquisitions in the future (couldn’t catch this well)

High precision - 25 PPM (Parts Per Million failure) track record vs 100 PPM specific customer requirement

2019 plant was shut down for some time - Still paid employees/vendors

Make 5-7 million parts a year (gears, shafts)

Next year’s growth in line with 2025 target of 500 Crs top line

Capex

50 Crs this year for new customers added

20 Likes

Here are my notes.

• 20-25% of CAPEX are funded through internal accruals and rest are funded by bank borrowings

• Ideal asset turns ~ 2, currently its 1.4x. Excluding land, useful equipment contribute ~140 cr.

• The gear capacities are fungible for ICE and EV customers, EVs require higher precision

• Instead of generating free cash, management believes to use cash to fund growth. With growth, reinvestment needs (in percentage terms) will come down

• Capex in 3 buckets: creating capacity for new customers, creating capacity for existing customers and modernization of equipment

• Capacity for gears, shafts and other equipment: Provide 5-7 mn parts in a year

• About 5-7% of vehicle cost is from gears

• 50 cr. CAPEX in FY21, plan another 50 cr. in FY22. Industry norm is to pay 20-25% as advances for procurement of machines

Disclosure: Invested (position size here)

24 Likes

Further to @harsh.beria93’s notes -

-

Growth: do not want to destabilize the boat by growing very fast as co is still small. Once a certain threshold is achieved and thus the ability to absorb losses goes up, one can accelerate further; grew from 100 crs. in F10 to 200 crs. in 10-12y, now intend to scale from 200 to 500 crs. in 4y, and maybe will do 500 to 1k crs. in 3y

-

Debt to Equity is very healthy and comfortable until 1.5x as the business is capital intensive; RACL gets customers first and then spends. Hence, the capacity is not lying idle & so is comfortable with the leverage levels. Also, interest expense as % of sales is trending lower

18 Likes

RACL Geartech AR 2020-21

1 Like

Recent concall audio recording available on RACL website under corporate announcements

http://www.raclgeartech.com/corporate_announcement.html

Now transcript

4 Likes

29 Likes

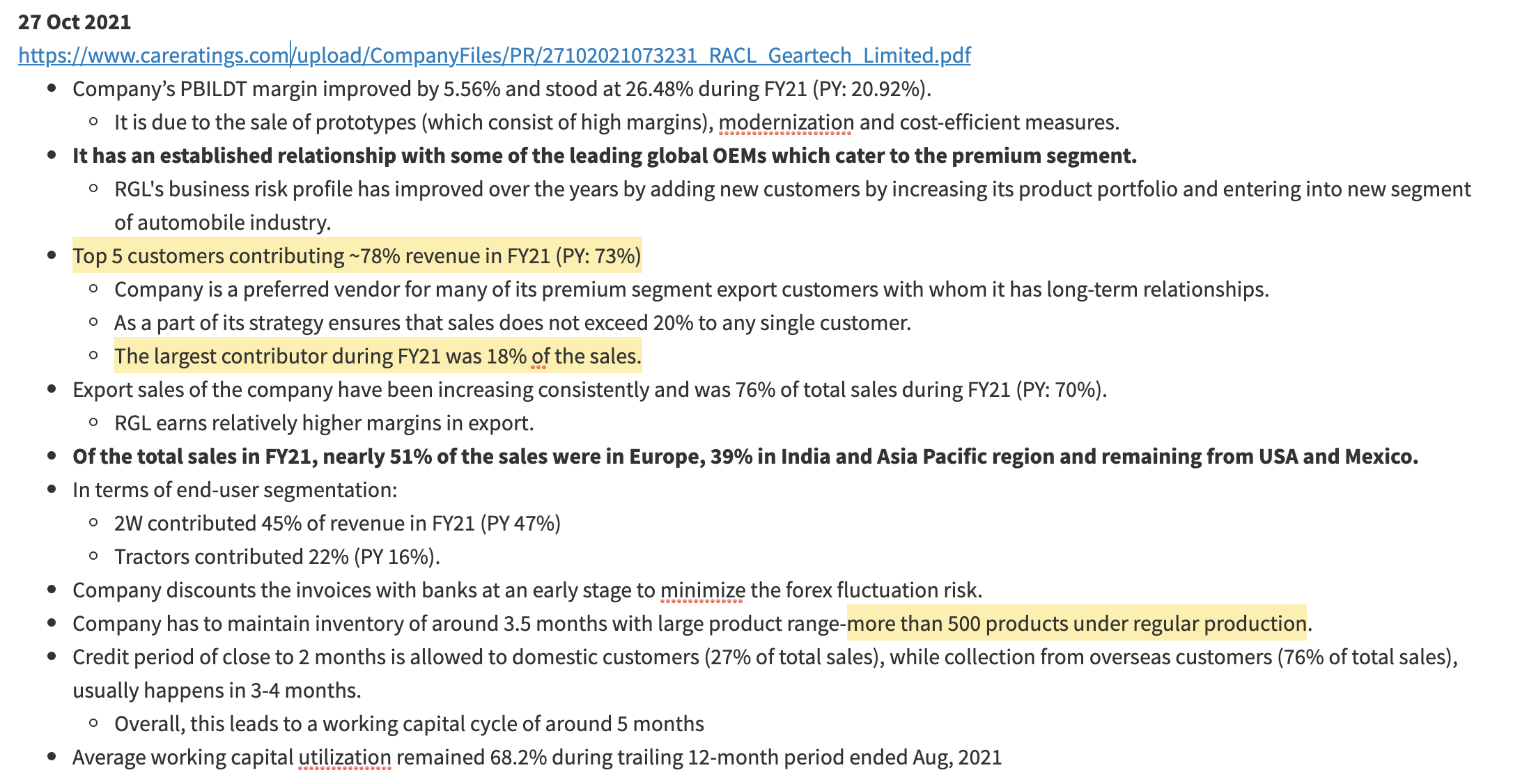

Hi All,

Sharing my notes from RACL’s latest credit rating report.

It has good data points around break-up of sales and customers.

Hope this helps!

Regards,

Yogansh Jeswani

Disclosure: Invested

29 Likes