Lots of insider trading violations happening at the company. Based on my research the only point that irks me about the company is promoter behavior on taking money out of the company. Wife of promoter is the highest paid non executive director without really having the necessary experience to be a director in the company. Very high promoter pay compared to other executives (their resigning CS was only paid 7 lakhs in yearly pay compared to promoter being paid more than 1cr) and now insider trading violations that were dismissed with ‘warning’ and barely any fines.

Just to clarify, ‘taking money out of the company’ has a different meaning akin to siphoning. Here, the promoter is trading in his own stock and not siphoning. But I did understand your perspective. Even I was surprised to see promoter indulging in unnecessary activities vs. running the company. Why are they disclosing? Is it voluntary or because of some SEBI diktat?

I had emailed the company about joining the conference call. The reply I got is as follows:

"Dear Investor,

Thank you for showing interest in the RACL’s Earnings Conference Call.

The final list of participants and link to the call shall be shared on 24th February, 2021. In the meanwhile, if you have any queries for the management, feel free to share the same"

Since company is doing it’s 1st concall, I thought it might be a good idea to collaboratively build up a good list of questions. Even if a small subset of us are able to join (from the reply it felt like only a few people would be allowed to join) this would enable whoever joins to ask tough/critical questions to management.

Here is a list of questions that I had in mind (in order of priority). Request everyone to please review and feel free to add anything I might have missed.

With a large part of automotive industry (including’s RACL’s target product segments of 2W and tractors) moving towards EV, what sort of effect would this have on RACL’s volumes, realizations and change in product mix? What are the key differences between the parts that RACL provides for ICE related automotive parts versus those that are provided for Electric Motor based vehicles?

Does RACL already provide automotive parts towards any EV cars? Are any such deals underway? Has the management considered entering such supply contracts? if so, what % of the topline comes from automotive parts that end up in EVs?

The company supplies automotive parts to global leading OEMs like BMW, Kuboto, KTM, Schneider etc. Can the company please comment on the nature of these supply contracts, whether they are multi-year, whether raw material price volatility can be passed on, and so forth.

Can the company comment on the status of the 50cr capex that they were undertaking in FY21? When is the expected completion date, and when would we be able to reach peak utilization on that capex? On a related note, what is the capacity utilization for our existing installed capacity?

For someone with enough capital (imagine say a Motherson Sumi), how difficult would it be to replicate RACL’s business? As far as we understand, the long gestation period client relationships and trust built through years of high quality product delivery are the competitive edge of the company. Are there any other competitive advantages for the company?

What are the growth aspirations of the company? Any medium term (3-5 year) revenue guidance?

Emailed them as well, here are the questions I have asked them.

What is the company’s plan to cater to the EV market (two wheelers and tractors) that will probably see the fastest EV disruption (next 2-3 years). There are new major players in the 2 wheeler market emerging like Ola (which has announced the biggest 2 electric two wheeler factor in the world to be set up in Tamil Nadu) and new companies like Ather Energy. Does the company plan to cater to these new emerging players since it will be easier to negotiate a supply contract with them as these companies are in early stages of their journey?

We added TVS as a customer for 2 wheelers, do we plan to add more domestic players?

What R&D is the company doing now for it to be ready for the EV disruption in the coming years?

These are very valid questions. I think it is very important to see impact of EV on the company and where do company see itself in next 3-5 years or may be beyond it. Good to know about company aspirations in medium and long term.

Disc -invested

I personally was quite pleased even to hear that a 180 odd cr topline company is even considering doing a conference call. I think we might have to give some leeway to these microcap companies. Often times, their non-core functions might not be as polished as their larger counterparts, but IMO the management intent counts for a lot.

Received the conf call details, plz note that only the already registered investors will be able to join:

Dear Investor,

Please find below the link to the RACL Geartech Limited Q3 2021 Earnings Conference Call to be held on 26th February, 2021 at 03:00 P.M. to discuss the Company’s Financial Performance:

Domestic market: Added Escorts Kubota (agri tractor), TVS (in their apache bike + 300cc BMW bike) and Kawasaki (which earlier had joint venture with Bajaj; now manufacturing alone) in Indian business segment.

Export market additions: CFMOTO (2-wheeler, KTM has tied up with CFMOTO to enter into China market, RACL had relation with KTM and are providing fully furnished gearbox to them), Moto Guzzi (2-wheeler high end Italian motorbike company, owned by Piaggio, they have had a long relationship with Piaggio), ZF (new client; biggest auto parts manufacturing company globally; entered Chassis component of passenger car (for both electric and conventional cars) which is a new segment; first Indian company to supply fully finished parts to passenger cars to ZF), Man trucks (Europe’s second largest CV manufacturer); New capacity: 50% will go to ZF and rest will go to Man trucks

One of major electric vehicle bike will be launched by European player in India

2025 turnover objective: 500 cr.

Key reasons for higher operating margin: Export margins are much higher. In-house manufacturing of certain instruments (eg: forging) have helped to improve margins. Also out-source some other jobs. Aims to maintain this kind of margins

Some prototyping orders this quarter have led to higher gross margins which is not sustainable

Expansion: Plant is already ready; end of 2021 will start production. Volumes will start coming in 2022

Core competence: Gears. Diversifying into chassis component (will remain in e-vehicles)

Precision of gears will increase manifold in e-vehicles. Investments have been into doing precision gears which makes less noise which is required in EVs

In India, gear making technology is not available. Equipment are generally imported

Current capacity utilization is 70-75%

10-15% of revenues can potentially come from the EV opportunity

This whole discussion is making a mountain out of a molehill,just like there was a lot of hair splitting on the “monthly updates”.The presentation is already on the exchanges

The transcript should be available soon enough too.

I just want to put things into perspective .Buying and Selling shares of own company over long period of time (either by promoters or employees ) is common .Sebi doesnt allow to do a reverse trade in less than 6 months .This rule many employees and non active /silent partners /promoters may not know .Once Sebi issues notice( very common practice )about this non compliance employees /promoters becomes aware and then starts monitoring this religiously thru company secretary and hence would never do this .Hence if you see the insider trading was of past and not present period .If now (from next qtr ) if you see this repeating ,then you should be worried .

BTW…board meeting is on 7th June to announce results. Any insights from long timers, in this board? I sense some nervousness in the price action, last few days and today’s crack (fell, almost 7%, as I type this…there is general sale in mid & small cap today, but not in that scale. I had seen this scrip, hold its head, during days of correction but not in the last few weeks…I am sensing something…or am I reading too much?)

Disc - invested

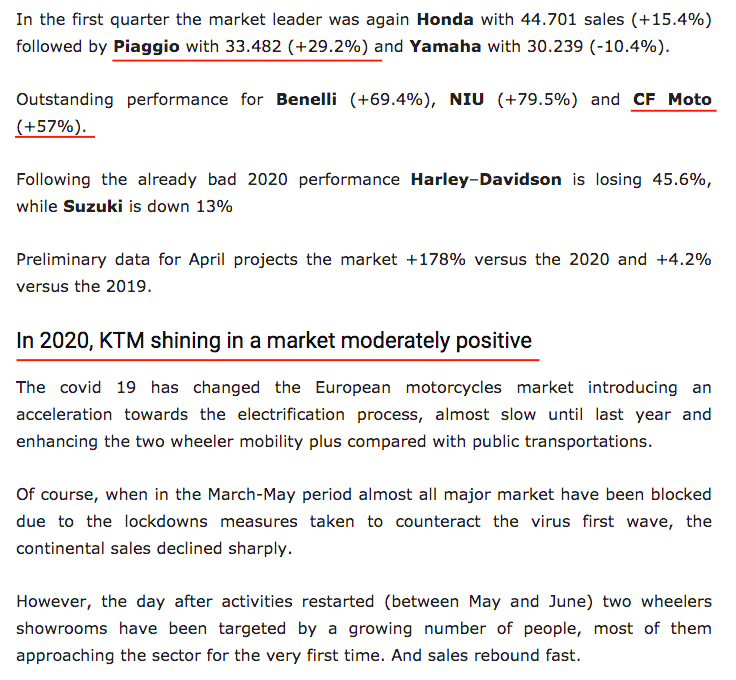

I was tracking the Q1 2021 sales and results for the RACL customers and found that almost all of them are clocking very very exciting numbers.

Piaggio and Moto Guzzi

In the first quarter to 31 March 2021, the Piaggio Group sold 135,000 vehicles worldwide

(+15.3% from 117,100 in the year-earlier period), and reported consolidated net sales of 384.7

million euro. The growth in volumes arose in all geographical regions.

BMW Motorrad was able to deliver 42,592 motorcycles and scooters to customers in the first three months of this year (+22.5%) – its best-ever sales result for a first quarter. This sales growth underpins BMW Motorrad’s successful growth strategy. Both its strong product offering, with a variety of different models, and the market launch of various new products, provide key elements for the continued success of BMW Motorrad.

TVS Motor’s facility produces 17% of BMW bikes globally.

Jumping off of the highly successful 310 platform (BMW G 310 duo and Apache RR 310), TVS and BMW are working on a new entry-level adventure bike which will be branded under the TVS name. It’s expected that the new bike could be heavily derived from the BMW G 310 GS, albeit slightly tweaked in order to be more affordable and accessible especially in the Indian market.

Escorts Kubota

Did not get the sales figures for this JV, but escorts reported strong growth of 64% YoY in Tractor volumes in Q4 21.

Summary

As the recent data suggests, lot of growth and positive activities are seen in the premium motorbike segments globally and the leaders from the lot are very long term customers of RACL. They are providing additional business too to RACL along with their own growth.

Disc: Invested from lower level, this is not any recommendation.

Qtr3 conference highlight(realized that summary is not posted here )

Competitive edge : Gears. Diversifying into chassis component (adjacency to Gears )

Precision of gears is key in e-vehicles. Investments have been into doing precision gears which makes less noise which is required in EVs

In India, gear making technology is not available. Equipment are generally imported

2025 turnover objective: 500 cr looking very much achievable .

Client addition in last 2 years :

Domestic market: Most recent addition is Escorts Kubota (agri tractor), TVS and Kawasaki (which earlier had joint venture with Bajaj; now manufacturing alone)

Export market additions:

CFMOTO (2-wheeler, KTM has tied up with CFMOTO to enter into China market)

Moto Guzzi (owned by Piaggio)

ZF (Fortune 500 company - biggest auto parts manufacturing company globally with turnover of USD 44 bn ) entered Chassis component of passenger car (for both electric and conventional cars) which is a new segment; first Indian company to supply fully finished parts to passenger cars to ZF

Interesting to note that their new business is also coming from tie ups of their present customers with new companies (speaks of stickiness of customers)

Capex expansion: Plant is already ready ,already trail batches has been sent ,commercial production by end of this calendar year –fully benefit to come by Mar 22 .

* 40% of capex dedicated to ZF

Capex backed by tentative order for next 5 years for all clients including ZF

Discl: One of the Top 10 individual shareholder and hence my view may be biased …

Well covered the conf call highlights, would like to add few more points:

MAN Trucks (old client till the time they exited India) - RACL have huge order from them and the capacity expansion shall be utilized for them too. Trucks are not going to get converted into Electric anytime soon, as management indicated.

Margin improvement and sustainability:

40% work for forging press work is done now in-house (earlier 100% were outsourced), improving raw material consumption and cost efficiency. Management are thinking of adding some more internal capacities.

Heat treatment have high cost and having higher overhead, they are mostly oursourced.

Improvement in internal productivity due to dedicated and motivated workforce, reducing rejection rate (important in export).

Whether higher steel price will dent the margin:

For all domestic customers, any hike in raw material price is passed to the customer through raw material indexation mechanism. For others, steel price is hedged through raw material indexation and foreign exchange indexation. So they are safegaurded in this regard.

Why receivable days are on higher side: 90 - 100 days?

Being located at north part of india, it takes 15 days for material to reach the port. 60 days from the bill of lading is the minimum payement time for export business, and co set off the receivables only after it comes back to bank. So effectively it takes that long time. RACL’s export share has increased gradually from 18.78% in FY 2011-12 to 52 % in FY 2015-16 to 70% in FY20.

RACL has installed Fassler Switzerland make 5-axis CNC controlled Gear Power Honing machines to fabricate high precision Gears with the capacity to meet the requirements for DIN Quality 6 & JIS Grade 3 quality.

One more important point I feel is that till date the growth were driven mostly by the old customers, as their business were growing or they were adding more parts from RACL. The revenue will start flowing now from the new customers, and this will drive the next phase of growth.

Disc: Invested from lower level, this is not any recommendation.